Banking on the Edge

What’s old is new again. The risks of international banking have returned to prominence in the wake of the Russian invasion of Ukraine. Global banks are playing a central role in the economic sanctions regime imposed upon Russia in response to its acts of military aggression. Foreign banks have retrenched from serving the Russian economy. International markets for debt, equity, and commodities are experiencing significant disruptions. The solvency measures and quarterly earnings of global banks have been impacted. These risks are new versions of an old story. International banking has been a fraught endeavor dating back more than a century. Despite their significance, the international operations of U.S. banks are often overlooked by legal scholarship.

This Article fills in some of this picture by examining the evolution of U.S. banks’ global presence through the lens of an underappreciated, but significant, law: the Edge Act of 1919. The Edge Act began as a framework for privatizing the post-World War I rebuilding effort. Its drafters argued that promoting the competitiveness of U.S. banks abroad would expand U.S. commerce, manufacturing, and exports. Instead, through a series of legislative amendments and misadventures with overseas expansion, the Edge Act became a vehicle for global banking conglomerates to operate lightly regulated overseas “nonbank-banks.” International banking policy came to prioritize the U.S. financial sector as its primary beneficiary, with deregulation as the predominant vehicle for achieving this goal.

The Edge Act is a case study for evaluating the longstanding desire to ensure that U.S. banks remain globally dominant. The results of eroding geographic and activity limitations include exposure to evolving risks—including sovereign debt crises, commodity price shocks, currency market risks, money laundering, derivatives dealing, and the growing use of financial sanctions—as well as increasing financialization, and an historic global financial crisis. As the experience of the Edge Act demonstrates, claims about the value of financial deregulation and its connection to international competitiveness should be treated with skepticism.

The appropriate role of global financial institutions is likely to be an issue of continued relevance as the emergence of nascent digital asset markets and digital banking models challenge the spatial and conceptual borders of financial markets. Without a thorough reexamination of the purposes and functions of international banking as we know it, beginning with the Edge Act, global banks may continue to exploit legal structural complexity in the name of international competition. As the case of the Edge Act demonstrates, such opportunistic use of regulatory arbitrage exposes the public to significant financial risk.

I. Introduction

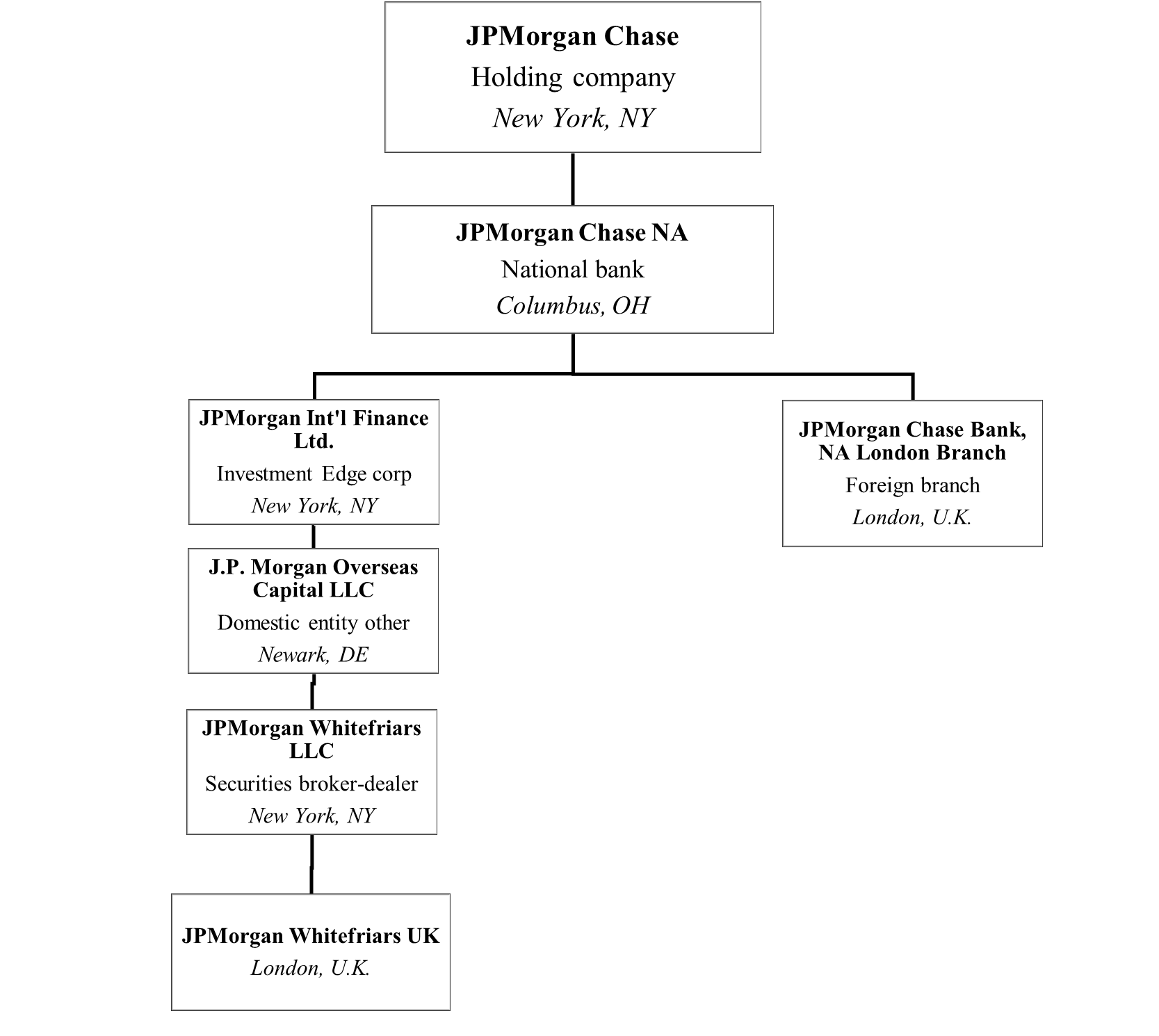

In April 2012, the name “Whitefriars” went from obscurity to relative notoriety in financial circles. A number of business media outlets had reported that a single JPMorgan trader, who had come to be known among industry participants as the “London Whale,” had been taking large positions in certain bespoke and illiquid credit derivatives markets.1 A month later, JPMorgan Chase would disclose that it had lost more than $2 billion on these trades; its losses eventually grew to more than $6 billion.2 Postmortem analyses of the London Whale trades uncovered inadequate management oversight of the activities in the company’s Chief Investment Office (CIO),3 resulting in an enforcement action and $300 million penalty from the Federal Reserve (Fed).4

A technocratic narrative emerged from the London Whale episode, focusing on inadequate risk measurements and complex products gone awry, particularly whether the relevant trades should have been classified as permissible risk-mitigating hedging transactions or prohibited proprietary positions.5 Less appreciated was the fact that dispersion of financial activities across a sprawling complex of legal entities had resulted in both a lack of clarity about the appropriate allocation of supervisory responsibility over international financial conglomerates, as well as difficulties in sharing examination information between regulators.6 The role of Whitefriars, a subsidiary established under a law known as the Edge Act, was largely absent from the policy debate that resulted from the London Whale.7

Rather than interpreting the episode as a cautionary tale that signaled a need to reform an antiquated U.S. banking law, observers largely glossed over the role in it of a specific type of international subsidiary of international banking conglomerates. As a result, an opportunity to reexamine the risks and benefits of an archaic—but nonetheless significant—banking law was missed. This Article attempts such a re-examination and argues that we will remain vulnerable to more London Whale-type events if the status quo persists.

The evolution of the Edge Act, from its origin as a law meant to encourage U.S. trade and exports to its central role in a scandal involving complex structured securities, is both important and underappreciated. Notwithstanding the fact that, according to one leading banking law textbook, the Edge Act “continues to be surprisingly relevant today,”8 there is a dearth of contemporary scholarship documenting the role of Edge Act Corporations (EACs) and their implications for modern banking law and policy.9 The Edge Act should not be overlooked any longer, as it serves as a valuable case study to enrich the picture of the role of U.S. banks in the global economy.10

While not a full account of U.S. banking activities abroad, the esoteric Edge Act offers a lens through which to observe the evolution of financial law and policymaking and the political economy of finance. EACs are overseas “nonbank-banks,” legal anomalies permitted to engage in a wide range of financial intermediation while enjoying exclusions or exemptions from the requirements and protections traditionally applied to banks. This arrangement exposes the domestic financial system to risk and complexity in the name of international expansion. Yet, the Edge Act is a lacuna in U.S. banking law that receives little scrutiny relative to the other forms of nonbank-bank.11

The Edge Act provides a case study for evaluating the claim that deregulation-driven “competitiveness” provides a boon to the nonfinancial economy through the financing of trade.12 Such was the justification offered in favor of the effective repeal of New Deal legal separations between banking and securities,13 and against more stringent regulation of the financial services sector in the wake of the Global Financial Crisis of 2008 (GFC).14 In the earliest days of his presidency, Donald J. Trump issued an Executive Order declaring “core principles” for his administration’s approach to financial regulation, one of which included “enabl[ing] American companies to be competitive with foreign firms in domestic and foreign markets.”15 In an otherwise anomalous presidency, this was an orthodox approach to financial regulation.16

The notion of “international competition” is premised upon a variety of assumptions: that large nonfinancial corporations will only be able to engage in international trade if there are giant international financial institutions; that having a larger financial system provides a net benefit to national economies; and, frequently, that U.S. banks are on the precipice of ceding their world dominance. The argument exists in a perpetual and delicate balance: the U.S. has the greatest markets and institutions in the world, but its success is always on the verge of being squandered as a result of regulatory overreach. More often than not, deregulation is the proffered means of preserving the competitive advantage of U.S. banking.17

Within this context, the following examination reveals that the justifications for the sui generis legal status of EACs are premised upon misplaced notions of international competition and trade. The Edge Act began as a means to promote the competitiveness of U.S. banks abroad in the service of U.S. manufacturing and commerce. As the financial sector has become increasingly volatile and self-referential, however, the Edge Act has come to prioritize banking as an end in itself. As a result, the tool of private financial sector deregulation and credit has proven to be an ineffective means of bolstering exports and the industries involved in producing them, such as manufacturing and agriculture. The original purpose of this century-old law has become an anachronism. The experience of the Edge Act should cause legislators and policymakers to treat such claims about the value of financial sector deregulation and international competitiveness with greater skepticism.

This Article proceeds to examine the Edge Act and its implications for international finance in the following sections. Section II recounts the legislative history of the Edge Act and U.S. banks’ early forays into overseas financing, which proceeded in fits and starts. Section II also describes the subsequent growing pains experienced during the post-World War II banking expansion, including a renewed push for bank deregulation and the risks associated with the newfound adventurism of U.S. banks. Section III revisits the era of so-called “financial modernization,” including its roots in U.S. competitiveness, the GFC and its aftermath, and current examples of systemically important financial companies’ uses of the Edge Act. Section IV explores areas in which the lessons gleaned from examining the Edge Act can be applied to current and future policymaking. This includes the traditional separations of banking entities from nonbanking financial and commercial businesses, attempts to impose activity constraints upon banking entities, the mechanics of cross-border resolution of international banking conglomerates, and the oversight of digital assets and payment systems. Before concluding, this Article considers potential reforms to the Edge Act and its implementing regulations.

These insights are likely to be of continued relevance with the emergence of digital banking and digital assets that have challenged the spatial and conceptual borders of the financial markets. The trend toward digitization has led to a resurgence of the nonbank-bank model and a revival of arguments promoting international competitiveness.18 In this context, the role of EACs within the corporate structure of modern financial conglomerates presents a cautionary tale of how private market “innovations,” in the form of piecemeal deregulation unaccompanied by proportional regulatory adjustments, leave the financial system exposed to unforeseen and underappreciated vulnerabilities.

These lessons are relevant once again in the wake of the Russian invasion of Ukraine. The international response has relied upon economic and financial sanctions transmitted through U.S. banks with global footprints.19 Banks’ direct exposures to the Russian economy have resulted in a reduction in their market capitalizations as well as their capital ratios.20 Global banks have also been indirectly exposed—including through their investment banking, wealth management, derivatives, and commodity financing businesses—in ways that are “difficult to identify and assess” with the potential to be “meaningful and surprise investors once revealed.”21 Global U.S. banks are vulnerable to cyber and other operational risks that could result from an attack on their information technology infrastructure in response to broader geopolitical events.22 Finally, political economists have begun to examine the interactions between international banks’ geopolitical importance and their domestic political power.23 While all of the concerns highlighted in this Article may not come to fruition, its contributions should help scholars and policymakers to better appreciate the risks to domestic economies posed by globalized banking.

II. Where We Were: The Era of Privatization

U.S. financial institutions were enlisted to help execute World War I. The Federal Reserve (Fed), the nation’s central bank, “recognized its duty to cooperate unreservedly with the Government to provide funds needed for the war and freely conceded that the great national emergency made it necessary to suspend the application of well-recognized principles of economics and finance which usually govern banking operations in times of peace.”24 Unusual measures, including an aggressive expansion of credit, were required because “[w]ar is the most uneconomic of all processes.”25 The Fed was not alone. Private banks helped the U.S. Treasury raise debt and supported European allies in managing their war production and monetary systems.26

By the end of the war, many European countries were in a precarious financial situation due to factors that included the decimation of national infrastructure during the war, the debt overhang from war financing, and the toll of German reparations payments.27 The U.S. had loaned a great deal of money to its European allies, and made debt repayment a priority at Versailles.28 All of these factors contributed to the passage of new legislation to boost U.S. exports and trade by leveraging the private banking system.

A. The Edge Act’s Origins

Until the passage of the Federal Reserve Act (FRA) in 1913, national banks could not establish overseas branches or accept drafts.29 Before the war, trade credit was only needed to smooth seasonal imbalances. In the postwar period, European nations’ rebuilding effort required them to import materials, and the typically short-term—60- or 90-day—credits used to finance trade during seasonal imbalances were not fit for purpose.30 The FRA addressed this by allowing national banks to establish branches abroad.31 A 1916 FRA amendment created “Agreement Corporations” (ACs), state-chartered banks authorized to operate abroad pursuant to a written agreement with the Fed.32

By 1919, the year of the Versailles Treaty, Congress was concerned that the U.S. had “been loaning enormous sums, or credits, to these countries for the purchase chiefly of foodstuffs, and Congress had authorized the War Finance Corporation to advance a round billion dollars for financing export trade.”33 It decided that “Government advances should stop and that the business should be financed by private capital.”34 Rather than focusing on the underlying foreign policy issues that created this precarious situation, such as the treaty’s onerous and austere economic implications, policymakers identified two of its symptoms: (1) the exchange rate disparities between the creditor U.S. and debtor European countries; and (2) U.S. banks’ constraints against providing trade credit.35 The latter factor inspired the Edge Act.

1. Credit as a Postwar Panacea

The Edge Act’s proponents argued that the U.S. had extended too much public support to its World War I allies, and that European countries should “put their houses in order” and stop asking for debt forgiveness.36 The solution to the European economic malaise was for the U.S. to become a full-fledged “creditor nation,” with private banks, rather than the Treasury, playing a central role in facilitating U.S. exports.37

Senator Walter Evans Edge of New Jersey argued that U.S. banks could play an important role in postwar trade and economic development, through the creation of corporate subsidiaries that could act as intermediaries between U.S. sellers and foreign buyers:

The American exporter or manufacturer may sell his goods to an impoverished foreign purchaser—a foreign government or a private concern. One of the proposed corporations then may accept collateral from the purchaser, acceptable to the Federal Reserve Board, and against this issue debentures to sell to investors, and the money so received will be paid to the American seller. Through the powers granted to these proposed corporations they may accept even mortgages on the plants or other real property of the purchasers . . . Thus a foreign concern in need of raw material may obtain it by giving a mortgage on its plant, and eventually by turning this raw material into finished product will be able to redeem its collateral and to put aside a little profit besides.38

According to one Fed official, there was “no one way in which the present European credit situation may be more effectively dealt with than by the incorporation of institutions of the kinds provided for” in the Edge Act.39 And “anything that betters that situation assists not merely in the gigantic task of reconstruction in Europe, but also in providing a market for our own exports and in developing our foreign commerce in a most effective and satisfactory way.”40

Legislators spoke about the Edge Act in similar terms:

A very large part of our prosperity as a nation now depends upon foreign trade, upon holding and extending foreign markets for our surplus products. If our export trade should collapse because of the utter inability of our chief customers to pay in cash or by the usual terms of drafts and bills of exchange the consequences would be disastrous to many of our industries. If on the other hand the passage of this bill . . . results in a certain measure of ownership of foreign transportation or industrial agencies we shall be but reinvesting in Europe, the capital which the people of the older countries formerly invested in our railroads and industries at a time when we of the United States needed capital. In a word, we shall have become in our turn a creditor Nation, having purchased securities that will bring us a continued income with a part of our surplus of commodities.41

Named after its sponsor, the Edge Act had three purposes: (1) encouraging U.S. banks to finance exports; (2) promoting international and domestic competition—namely, helping regional U.S. banks compete with foreign banks and challenge an international banking monopoly;42 and (3) enhancing Federal oversight of U.S. banks’ international operations.43 It framed financial deregulation as the solution to an array of economic and geopolitical problems.44 Like most financial deregulation, it was presented as a win-win proposition: freeing U.S. banks from their constraints abroad would shift the burden of solving Europe’s economic problems from the public to the private sector.45 Credit would fill the gap for the lackluster macroeconomic situation. The profits would accrue to the U.S. manufacturing and finance industries. This arrangement would benefit “real economy” businesses like manufacturers, farmers, and ranchers.46 The fate of the U.S. financial system, and the wellbeing of the nation as a whole, was at stake.47

2. Creating Overseas Nonbank-Banks

The Edge Act added section 25A to the FRA, authorizing the creation of EACs as corporate subsidiaries of national banks with a special charter from the Fed to “engag[e] in international or foreign banking or other international or foreign financial operations” without complying with state-by-state banking laws.48 EACs could, pursuant to regulations promulgated by the Fed, engage in nine different financing activities, including some limited deposit taking.49 EACs could establish branches or agencies abroad, subject to Fed approval and any relevant terms and conditions.50 An EAC’s ability to operate inside the U.S. was limited to activities that the Fed determined were “incidental to its international or foreign business.”51

While early drafts had limited EACs to banking, the Fed argued that allowing EACs to engage in other “financial activities” was essential to achieving the goal of boosting exports.52 The Edge Act created two types of entities: (1) banking EACs that engage in limited deposit taking, lending, and related activities; and (2) investment EACs in which a U.S. bank directly owns shares in foreign companies.53 Because EACs were “not to be banks of deposit,” Congress determined that they did not require traditional banking protections.54

Departing from the longstanding principle of separating banking from commerce,55 EACs were permitted to invest in nonfinancial companies, so long as the companies’ U.S. business was only “incidental to its international or foreign business.”56 This authority was intended to allow banks to invest in joint ventures with nonfinancial companies, bringing their financing expertise to the realm of trade.57 At the same time, EACs were prohibited from otherwise “engag[ing] in commerce” or directly trading commodities, and EACs and their officers and directors were prohibited from controlling or fixing the price of commodities or conspiring to use the EAC’s financial resources to do so.58 In tension with EACs’ ability to own nonfinancial businesses, Congress was concerned that, consistent with broader concerns about mixing banking and commerce, allowing EACs to own and trade in commodities would create monopolies that engage in anticompetitive practices like driving up prices or tying the purchase of raw materials to credit products.59

EACs were subjected to several other limitations. To ensure their solvency, they needed a minimum of $2 million in total capital at the time of incorporation, and national banks could not invest more than 10 percent of their capital in EAC stock.60 Directors of EACs were required to be U.S. citizens, and the majority of investors in an EAC were required to be U.S. citizens or corporations.61 At the same time, EACs’ officers, directors, and employees were exempt from the management interlocks prohibitions of the Clayton Antitrust Act of 1914, permitting them to serve at both an investing bank and its investee EAC.62 EACs were also restricted from buying stock in EACs or ACs that were in “substantial competition.”63

The Edge Act highlights the complexity, and resulting tensions, of financial policymaking throughout the 20th century.64 Policymakers argued that nonfinancial industries were best served by policies limiting banks’ activities and constraining their economic power.65 At the same time, they believed customers and the economy would benefit from policies that promote financial “competitiveness” by allowing banks to engage in a wide range of financial activity.66 Reconciling these conflicting policies has been a recurring challenge in international and domestic banking law.

B. The Uneven Early Years of International Banking

The Fed issued the first rules governing U.S. banks’ international activities, Regulation K, in 1920. Regulation K included procedures for EACs and ACs to establish foreign branches, engage in international banking, and invest in foreign organizations.67

There was some initial, but modest, growth in U.S. banks’ international activities in the postwar European reconstruction period, with three EACs formed in the 1920s. The Federal International Banking Company was a consortium of a thousand commercial banks, with a home office in New Orleans. It was established to finance trade in tobacco, lumber, and, most importantly, cotton.68 The First Federal Foreign Banking Association was organized by eleven commercial banks to finance foreign trade, and the First Federal Foreign Banking Corporation operated subsidiaries in Argentina, Brazil, and Switzerland, and offices in several other countries.69

In 1929, a consortium of aspiring bankers challenged the Fed’s denial of their application to form their EAC, the Foreign Financing Corporation.70 The Fed had determined that the applicants lacked the “qualifications reasonably necessary to assure the financial soundness, reliable and competent management, or the proper or successful operations of a corporation organized under [the Edge Act] to engage in the highly technical activities of international or foreign banking or other international or foreign financial operations and that it would be detrimental to the public interest to approve” their application.71 In Apfel v. Mellon, the court concluded that “Congress was providing a means for conferring special and important privileges upon such corporations as should be organized under the Edge Act” and that “abuse by any corporation of the powers thus granted to it might involve grave consequences to our public service.” 72 It was therefore “reasonable to believe that Congress intended that a careful investigation should be made by the [Fed] concerning the character and competency of the incorporators of such an enterprise, as one of the means of determining whether to grant or withhold their approval of the application for incorporation.”73 Not only did EACs have latitude to operate internationally, but the Fed enjoyed discretion in determining the scope and fitness of EACs’ operations.74

By 1932, twenty EACs and ACs had been chartered.75 After the enactment of the Edge Act, large U.S. banks underwrote and marketed syndicated loans to the German government, as well as bonds issued by European governments and corporations, and by Latin American countries.76 Nonetheless, financial deregulation could not fix the economic and political problems created by the debt overhang from World War I. As a result, economic growth remained weak while the political status quo grew increasingly unstable.77 Federal International Banking Company and First Federal Foreign Banking Association were liquidated in 1925, and the third, First Federal Foreign Banking Corporation, was liquidated in 1933.78

1. The Great Depression and the Glass-Steagall Act

U.S. export financing tapered off and came to a virtual standstill during the stock market crash and the ensuing Great Depression. In the wake of that banking panic, Congress passed the Banking Act of 1933, commonly known as the Glass-Steagall Act, separating commercial banking from investment banking.79 The Banking Act added a new section 23A to the FRA limiting transactions between banks and their nonbank affiliates.80 The Banking Act also gave the Fed authority to limit the interest rate that banks could pay to attract time and savings deposits, and prohibited paying interest on demand deposits.81

Glass-Steagall was meant to prevent banks from using public-backed funds for speculative activities and limit the associated risks.82 Its sponsors argued that the “banking system was diverted from its original purposes into investment activities” and narrowing banks’ focus would “call back to the service of agriculture and commerce and industry the bank credit and the bank service designed by the framers of the [FRA].”83 Among their examples, they cited large banks’ marketing of risky foreign bonds through their securities businesses.84

Yet, neither Glass-Steagall’s structural separations nor section 23A’s affiliate transaction restrictions applied to EACs.85 U.S. banks’ international activities were exempted from rules meant to limit banks’ activities, again ostensibly in the name of “competitiveness.”

2. The Postwar Era

Interest in overseas banking remained stagnant for the next two decades.86 By 1940, only one EAC remained, owned by Chase National Bank.87 Just two EACs were chartered between 1932 and 1956.88 One was Bank of America, which engaged in general foreign banking and, until 1963, operated several foreign branches.89 The other, American Overseas Finance Corporation, engaged in medium-term financing of purchases of U.S. equipment and services by foreigners, and in foreign lending and investment to finance the establishment and expansion of business abroad.90

In contrast to the post-World War I privatization approach codified by the Edge Act, the post-World War II era saw increased public trade financing. Private financing could neither meet the direct need for purchases by European nations rebuilding their economies, nor sustain the U.S. manufacturing sector’s wartime expansion.91 In 1945, Congress codified the government-chartered U.S. Export-Import Bank (EXIM) as an export credit agency for the “purpose of aiding in the financing and facilitating of exports and imports,” with the statute noting that Congress intended the bank to “supplement and encourage and not compete with private capital.”92

The Bretton Woods agreement, reached in 1945 and implemented in 1958, instituted a system of currency convertibility among significant economies with the International Monetary Fund (IMF) as a central multilateral financial institution and the U.S. dollar as the reserve and trading currency.93 Other notable developments during this time included the creation of the Common Market in Europe, a flow of investment from the U.S. abroad, and an interest by wealthy countries in investing in developing economies.94

Throughout this period, U.S. banks used EACs as an international vehicle for arbitraging domestic business restrictions. One example of this was the emergence of the “Eurodollar” market as a significant financing source. The Eurodollar market is the “market for dollar-denominated financial accounts and instruments situated outside of the United States.”95 Eurodollars enabled U.S. banks to more easily serve foreign clients, attracting deposits and certificates of deposit though their international operations, without either (1) running afoul of the capital controls that the U.S. government had instituted in 1965 to address balance of payment issues, or (2) being limited by the Regulation Q prohibition against paying interest on deposits.96

In another example, Congress enacted reforms that sought to tighten limits on domestic banking activities and ownership, but preserved the special status enjoyed by EACs’ activities abroad. The Bank Holding Company Act of 1956 (BHCA) required Bank Holding Companies (BHCs) to limit their activities and investments to banking, managing or owning banks, or a set of activities that are closely related to banking, as determined by the Fed. The BHCA also required BHCs to limit the trend of banking expansion in circumvention of branching restrictions.97 Yet entities organized by U.S. BHCs to operate abroad, including EACs, were excluded from the terms of the BHCA.98

Third, banks used EACs to engage in securities activities that were otherwise prohibited by Glass-Steagall. A 1957 revision to Regulation K sought to codify the original intent of the Edge Act by creating two distinct legal entities, the banking Edge and the finance Edge.99 In doing so, the rule was meant to implement the spirit of Glass-Steagall by separating deposit banking from investment banking.100 Many of the large New York banks established both types of EAC,101 and many of the largest banks still retain both a banking EAC and a financial EAC. In addition, while the 1957 Regulation K revision differentiated banking and nonbanking entities, it also liberalized the activities that these entities could engage in, making both types of EACs more attractive as financing vehicles.102

In 1963, the Fed further revised Regulation K, walking back its distinction between banking EACs and finance EACs.103 The rule also codified a statement of “national purpose,” that EACs are meant to have “powers sufficiently broad to enable them to compete effectively with similar foreign-owned institutions and to afford to the United States exporter and importer in particular—and to United States commerce, industry, and agriculture in general—at all times a means of financing international trade.”104 Again, the Edge Act sought to ensure the competitiveness of U.S. banks in the service of financing international trade and thereby bolster manufacturing, agriculture, and the economy in general. In doing so, EACs had flexibility to conduct a range of activities and use a variety of structures, but were only to engage in activities that were “in the interest of the United States,” and practices that were “consistent with high standards of banking or financial prudence” and “clearly related to international or foreign business.”105

EACs developed three primary structures to make foreign investments: (1) wholly owned subsidiaries; (2) controlled subsidiaries with substantial minority investment from a local financial institution; or (3) minority interests in foreign subsidiaries.106 Large U.S. and European financial institutions could also invest in joint ventures with foreign banks.107 This latter arrangement complicated the picture of international “competition” by permitting collaboration, as opposed to outright opposition, between ostensible competitor institutions.

U.S. banks continued expanding their activities abroad from 1955 to 1966, with the value of dollar loans and acceptance credits issued to foreign customers growing from $1.75 billion to $9.6 billion, and the number of EACs and ACs growing from seven—three EACs and four ACs—to forty-five, thirty-six of which were EACs, owned by thirty-three banks and BHCs.108 In terms of geographical dispersion, as of 1964, EACs were making about 40% of their equity investments by dollar value in Europe, with 20% in Latin American countries, 20% in Canada, 10% in Africa, and 5% in Asia.109

During this period, banks “began to use London as a center for unregulated deposit taking and lending in dollars.”110 In particular, “eurodollar accounts in Europe offered the basic framework for a largely unregulated global financial market.”111 U.S. banks offered “Eurodollar loan” products, which critics argued were functionally securities products conducted abroad, through EACs, in “subterfuge” of U.S. securities laws.112 Many of the EACs formed in the 1960s were set up “primarily to engage in the Eurodollar market,” clearing funds procured by the parent bank through its branches abroad.113 U.S. banks using EACs to arbitrage domestic banking restrictions would become a pattern in ensuing decades.

C. The Expansion of International Banking

Subsequent realignment of the international economic order altered the course of U.S. banks’ overseas expansion. Bretton Woods formally collapsed in 1973, coinciding with a rise in “petrodollars” and a corresponding demand for unencumbered capital movement.114 In 1974, the Fed relaxed its capital control rules, freeing U.S. banks’ international lending and deposit activities.115

Table 1 illustrates the growth of EACs as a vehicle for international finance over the course of almost two decades. From 1956 to 1974, the number of EACs grew more than thirty-five-fold, from three to 107.

Table 1: Growth of Overseas Banking

U.S. EACs, 1956–1974

|

Year |

Number of U.S. EACs |

|---|---|

|

1956 |

3 |

|

1957 |

4 |

|

1958 |

5 |

|

1959 |

6 |

|

1960 |

10 |

|

1961 |

11 |

|

1962 |

22 |

|

1963 |

30 |

|

1964 |

36 |

|

1965 |

37 |

|

1966 |

40 |

|

1967 |

46 |

|

1968 |

56 |

|

1969 |

63 |

|

1970 |

69 |

|

1971 |

80 |

|

1972 |

87 |

|

1973 |

98 |

|

1974 |

107 |

Source: Fed. Rsrv Bank of N.Y., Fed. Rsrv. Bank of Chi., Joint Econ. Comm., U.S. Cong.

This expansion opened new opportunities for U.S. banks, but also shifted the focus away from domestic activities like municipal financing.116 At the same time, U.S. banks were exposing themselves to new risks, highlighted by the failure of the German bank Herstatt. Counterparties that had paid German Deutschmarks to Herstatt failed to receive their corresponding dollar payments in return, demonstrating the dangers of foreign exchange settlement.117

As shown by Table 2, U.S. banks’ operations abroad were concentrated in major trading partners and international financial hubs, namely the U.K., Canada, Australia, Hong Kong, Brazil, and offshore jurisdictions. In addition to financing manufacturing, EACs were used as vehicles to invest in mining and other extractive industries, both abroad and in the U.S.118

Table 2: Global Reach of U.S. Banks

Foreign subsidiaries of U.S. banks, BHCs & EACs, 1975

|

Location |

Number |

Percent |

Total Assets ($bn) |

Percent |

|---|---|---|---|---|

|

Europe |

324 |

50.2 |

15.1 |

60.6 |

|

Canada |

93 |

14.4 |

3.0 |

11.9 |

|

Latin America |

61 |

9.5 |

1.0 |

4.0 |

|

Australia |

60 |

9.3 |

1.7 |

6.8 |

|

Offshore jurisdictions |

45 |

7.0 |

2.5 |

10.0 |

|

Asia/Pacific |

44 |

6.8 |

1.1 |

4.6 |

|

Israel |

18 |

2.8 |

0.6 |

2.6 |

|

Total |

645 |

100 |

24.9 |

100 |

Source: Norman S. Fieleke, The Growth of U.S. Banking Abroad: An Analytical Survey (Prepared for “Key Issues in International Banking,” Fed. Reserve Bank of Bos., Oct. 1977)

U.S. policymakers continued expanding EACs’ privileges in service of promoting international competition. In 1975, the Fed revised Regulation K’s application to state member banks. Under the Fed’s interpretation, the FRA prohibited state member banks from establishing operating subsidiaries abroad, unless they availed themselves of the FRA’s provisions expressly permitting foreign investments, which included the Edge Act.119 EACs thus remained one of the limited avenues by which U.S. banks could operate abroad. In 1977, the Fed permitted U.S. banks’ EAC subsidiaries to raise debt in foreign markets and transfer the proceeds to their parent BHCs for domestic use.120

1. The International Banking Act and Super Edges

Assets held by EACs and ACs nearly doubled from 1972 to 1976, growing from about $6 billion to $11.6 billion, and by 1977 there were 116 registered EACs.121 Congress was encouraged that EACs had “no doubt assisted in the financing of U.S. exports,” but echoed the familiar refrain that an “antiquated statutory and regulatory framework” has “hampered their “usefulness” and “has put them at competitive disadvantages.”122 The International Banking Act of 1978 (IBA) was meant to “mitigate any competitive disadvantage resulting from the line of business restrictions found within U.S. law” by allowing U.S. banks to engage in activities overseas that were impermissible at home, at the same time subjecting Foreign Banking Operations (FBOs) to greater oversight of their U.S. operations.123

The IBA targeted three types of banking law provisions: (1) those that “discriminate” against FBOs, (2) those that “disadvantage or unnecessarily restrict or limit” EACs in their competition with FBOs at home and abroad, and (3) those that impede the Edge Act’s longstanding policy that U.S. banks should facilitate exports and trade.124 The IBA incorporated a new policy statement into the Edge Act that established the following goals:

[T]o provide for the establishment of international banking and financial corporations operating under Federal supervision with powers sufficiently broad to enable them to compete effectively with similar foreign-owned institutions in the United States and abroad; to afford to the United States exporter and importer in particular, and to United States commerce, industry, and agriculture in general, at all times a means of financing international trade, especially United States exports; to foster the participation by regional and smaller banks throughout the United States in the provision of international banking and financing services to all segments of United States agriculture, commerce, and industry, and, in particular small business and farming concerns; to stimulate competition in the provision of international banking and financing services throughout the United States; and, in conjunction with each of the preceding purposes, to facilitate and stimulate the export of United States goods, wares, merchandise, commodities, and services to achieve a sound United States international trade position.125

These policies were meant to guide any future revisions that the Fed made to Regulation K, which the IBA required it to review every five years.126 The IBA’s drafters wanted to clarify that the Edge Act’s “emphasis is on financing exports; and that is where it should be in order to establish and maintain a sound U.S. trade position.”127

The IBA eliminated the limitations on EAC’s assumption of debt in excess of ten times its capital as well as the requirement that each EAC maintain reserves equal to 10% of its U.S. deposits.128 It also removed the prohibition against foreign citizens serving as officers and directors of EACs, and permitted FBOs to become majority owners of EACs.129 The law sought to create parity between FBOs and U.S. banks with respect to establishing branches and engaging in interstate banking.130

While the four points in the IBA policy statement were generally consistent with the Edge Act’s original purposes, policymakers largely focused on the first policy—competitiveness—after the IBA’s passage. By the 1980s, most large banks, including all fourteen banks with more than $10 billion in assets, owned EACs, and forty-eight banks with $3 billion or more in assets accounted for 95 of the 131 EACs in existence.131 Banks used EACs to finance trade abroad through a variety of unique products and markets, including foreign exchange, letters of credit, bankers acceptances, and Eurocurrency.132 They used their EACs to invest in foreign financial companies, including nonbanks and banking organizations, as well as in passive equity-type “merchant banking” investments in nonfinancial businesses abroad.133 The competitiveness of U.S. banks was becoming an end in itself, rather than a means to promoting U.S. trade, exports, and manufacturing.

Again, EACs were used to arbitrage domestic banking restrictions. After the IBA’s enactment, the Fed amended Regulation K to allow EACs of U.S. banks to branch domestically, subject to Fed approval.134 Banks could establish as many EAC branches as the Fed permitted, and by consolidating disparate EACs into one EAC with multiple branches, the 10 percent individual lending limit of the consolidated EAC’s capital was available to each branch location.135

Establishing an EAC allowed banks to operate in more regional markets, namely New York, but also San Francisco and Miami, evading interstate branching restrictions, an option generally only available to large banks given the $2 million minimum capital requirement.136 In the mid-1950s, there were two banks with EACs in New York: Bank of America, New York, and Bank of Boston International. By 1966 there were nine, established by banks in Boston, Minneapolis, Pittsburgh, Chicago, Los Angeles, and San Francisco.137

Beginning in the early 1970s, banks focused on Miami as a hub of EAC activity, given Miami’s trade relationship with Latin America, particularly the growth of direct exports to Latin America, the number of companies that had established their Latin America operations in Miami, and the desire to attract deposits from Latin American clients.138 In 1977, there was greater regional dispersal, with 38 of the 116 EACs in existence in New York, twelve in Los Angeles, eleven in Chicago, ten in Miami, and nine in Houston.139

In the eighteen months following the 1979 Regulation K revisions, eleven banks received approval to establish in total twenty-eight EAC branch offices.140 A review of Federal Register publications in the decade following the IBA’s passage, as depicted in Table 3, demonstrates the benefits that law provided to the banking industry.141

Table 3: Building “Super Edges”

Edge Act activity after the IBA, 1978–1990

| Year | Applications142 | Domestic Banks | Foreign Banks | ||

|---|---|---|---|---|---|

| EACs | Branches | EACs | Branches | ||

| 1978-1980 | 35 | 16 | 52 | 5 | 0 |

| 1981-1990 | 83 | 31 | 59 | 21 | 10 |

| TOTAL | 118 | 47 | 111 | 26 | 10 |

Source: Federal Register

These figures illustrate the growth of domestic Edge Act activity in the wake of the IBA, as assets held in EACs tripled from 1978 to 1981.143 U.S. BHCs used EACs to expand their U.S. operations, broadening their branch networks in circumvention of the prohibition against interstate branching.144 The resulting entities, with a parent EAC and a network of branches operating in critical U.S. markets, were known as “super-Edges.”145

In 1981, the Fed provided additional flexibility for EACs’ domestic operations by allowing EACs to invest in foreign companies that operate within the U.S., so long as that company is “predominately engaged” in business outside the U.S., engages in activities “closely related” to banking, and the EAC acquires no more than 25% of the company’s equity.146

The Competitive Equality Banking Act of 1987 (CEBA) responded to the growth of nonbank-banks, entities that engaged in bank-like activities without the regulatory and supervisory regimes applicable to banks, including enabling their parent companies, often commercial businesses, to avoid BHC registration requirements.147 EACs were among the nonbank-banks that were excluded from CEBA’s expanded definition of “bank,” which was meant to capture previously un-addressed deposit activities and lending.148 At the same time, CEBA extended the restrictions on bank lending to insiders and prohibitions against tying to EACs.149 Thus, while CEBA’s intent was strengthening the separation of banking and commerce, much of EACs’ special, nonbank-bank status remained even after the law’s passage.

As U.S. BHCs expanded their branch networks, the number of EACs and ACs declined, from one hundred and twenty-six in 1980 to one hundred in 1990.150 In 1994, Congress enacted the Riegle-Neal Interstate Banking Efficiency Act, permitting national banks to engage in interstate branching.151 Industry stakeholders and policymakers argued that U.S. banks’ inability to branch across states was preventing them from competing internationally; conversely, interstate branching would help preserve their market share in exporting industries.152 Authorizing interstate banking diminished EACs’ utility in circumventing branching restrictions.153

2. Public-Private Partnership: Edge Corporations and Export Credit Agencies

While EACs’ role as conduits for U.S. trade financing has been framed as an exclusively private endeavor, they have frequently benefitted from various kinds of government support. The 1960s saw the beginning of bank partnerships with foreign governments, with EACs making investments in government-sponsored development banks in India, Pakistan, and Nigeria.154 EACs also invested in sovereign development entities and their projects through loans, bond purchases, and other forms of financing, in addition to multilateral development bodies like World Bank subsidiary International Finance Corporation (IFC) or the U.S. Agency for International Development (USAID).155 EACs have been eligible for insurance through USAID for investments in less-developed economies, protecting them from risks such as inconvertibility, expropriation, and disturbances caused by wars or civil unrest.156

EACs also partnered with U.S. export credit agencies to fund international projects.157 In 1982, Congress passed the Bank Export Services Act (BESA), which aimed to “increase United States exports of products and services by encouraging more efficient provision of export trade services to United States producers and suppliers,” including by permitting BHCs or their subsidiary EACs to invest in export trading companies (ETCs).158 An ETC is a U.S. company that is “exclusively engaged in activities related to international trade, and which is organized and operated principally” for the purpose of exporting U.S. goods or providing export trade services to facilitate the exporting of U.S. goods.159 Allowing BHCs to own ETCs deepened the public-private partnership at the heart of the Edge Act.160 BESA directed the EXIM Bank to establish programs to guarantee ETC-financed loans when private financing was not otherwise available,161 serving as a guarantor of last resort for banks’ export financing activities.

Again, deregulation was meant to solve such vexing problems as the trade deficit, the value of the dollar relative to foreign currencies, and the risks of inflation.162 Industry promised that the legislation would produce new manufacturing jobs, while some members of Congress expressed doubts about further undermining the separation of banking and commerce.163 Ensuring the “meaningful and effective participation” of private financial companies in “the financing and development of export trading companies,” was supposed to make export financing more competitive, realize economies of scope, and coax regional banks and small- and medium-sized enterprises into international trade.164

Deregulation again came up short as a tool of trade and export policy. Following the passage of BESA, there was “relatively slow development of bank-affiliated export trading companies,” with only forty-five BHCs applying to establish ETCs.165 Acknowledging that this lackluster activity “may have been significantly influenced by the adverse economic climate that made exporting difficult for all sectors of the U.S. economy, as well as the unfamiliarity of U.S. bank holding companies and manufacturers with ETCs as vehicles for export trade,” Congress nonetheless pinned some of the blame on “unduly restrictive” Fed regulations.166 The Export Trading Company Act Amendments of 1988 further deregulated BHC-owned ETCs, including by increasing the amount of leverage they could employ.167 These tweaks had seemingly little effect, as the total number of ETCs increased by just three, to forty-eight by 1996.168

These new legal entities and public programs were an important milestone in international banking. While originally driven by the dual aims of financial competitiveness and export promotion, the banking laws were now largely focused on the competitiveness of U.S. banks. Exports, trade promotion, and the financing thereof, was becoming the public sector’s responsibility.169 Thus, EACs not only benefitted from deregulation in the name of facilitating trade and industry, but they also shifted some of the risks of operating internationally onto the U.S. government.170

3. Risky Markets: Sovereign Debt and Money Laundering

Banks predominately used their super-Edges to target domestic markets with a nexus to international trade. Banks’ branch applications were often reorganizations, establishing an EAC in a bank’s home city with branches in regional trade hubs.171 As mentioned above, Miami was a focal point for EAC activity in the late 1970s and early 1980s due to its proximity to Latin America and state laws encouraging international banking.172

During this period, large U.S. banks’ exposure to loans in developing countries, particularly in North and South America, increased substantially,173 leading to concerns about the stability of the U.S. banking system. In 1977, Fed Chair Arthur Burns “warned repeatedly that bank lending to less developed nations was proceeding at a pace ‘too fast’ to be sustained.”174 After two oil price shocks during 1973–74 and 1979–80, Mexico and Argentina defaulted on some bond payments in 1982, escalating the level of the banking system’s exposures “from the category of ‘problem’ to ‘crisis.’”175

The policy response mixed regulation and relaxation. In 1987 and 1988, the Fed allowed EACs to invest through debt-for-equity conversions. U.S. banks could restructure troubled foreign loans through debt-for-equity swaps and joint ventures with sovereign entities, allowing foreign governments to convert dollar loan repayments into local currency that would be reinvested in companies or sovereign entities in the same jurisdiction.176 EACs were allowed to invest up to 100% and 40% in the equity of sovereign and privately owned nonfinancial foreign ventures, respectively,177 subject to holding and divestiture periods and exposure limits.178

Congress also determined that, along with broader macroeconomic trends, lax bank supervision contributed to the indebtedness of certain countries and the related default risk exposure of some banks.179 The International Lending Supervision Act of 1983 (ILSA) directed regulators to strengthen banks’ capital adequacy by increasing capital requirements, particularly for international lending.180 ILSA required supervisors to evaluate foreign country exposures and transfer risks, and banks to report regularly on these risks.181 ILSA required regulators to establish reserve requirements for foreign country risk, and set special requirements for highly indebted countries.182 Finally, ILSA required additional documentation and examination of banks’ risks from large foreign loans related to mining, metal and mineral processing, or fabrication.183 At the same time, ILSA directed the Treasury Secretary and the banking regulatory agencies to encourage their foreign counterparts to “work toward maintaining and, where appropriate, strengthening the capital bases of banking institutions involved in international lending,”184 a provision that would help to spur the Basel I International Capital Accord.185

Increased exposure to money laundering schemes was a second consequence of international expansion during the 1970s and 80s. The Bank of Credit and Commerce International (BCCI) was a notable example of this vulnerability. BCCI was a Luxembourg-based foreign holding company founded in 1972, with banks chartered in London and the Cayman Islands and head offices in Karachi and London, the largest shareholder of which was the sovereign wealth fund of Abu Dhabi.186 Beginning in 1987, U.S. regulators detected irregularities in BCCI’s U.S. operations, first with respect to suspicious money laundering activities occurring in BCCI’s Miami agency that resulted in criminal indictments and the Fed issuing a cease-and-desist order.187 From 1991 through 1992, BCCI’s international holding company and one of its U.S. subsidiaries were liquidated.188

In response to the supervisory failures uncovered by this episode, regulators established an international supervisory college for examining and supervising international banking institutions in 1988.189 In its immediate aftermath, Congress enacted the Foreign Bank Supervision Enhancement Act of 1991 (FBSEA), which augmented the Fed’s role in consolidated supervision of international banking conglomerates, as well as in oversight of FBOs’ U.S. operations.190

Riggs Bank was another example of money-laundering risk. Riggs filed its application to create a Miami-based EAC with the Fed in 1980, which then opened in 1981.191 The risks of money laundering activities in the Miami market were well known at the time.192 During 1994–2002 and 1995–2004, Riggs facilitated illicit banking services for Argentinian dictator Augusto Pinochet and members of the regime in Equatorial Guinea, respectively. Riggs’ Edge Act subsidiary Riggs International Banking Corporation (RIBC) was a participant in this activity.193 Riggs agreed to a consent order with the Fed to address RIBC’s deficient Bank Secrecy Act and Anti-Money Laundering (AML) compliance.194 Riggs closed RIBC on December 31, 2004195 and pled guilty to a felony count of failing to file suspicious-activity reports (SARs) accompanied by a $16 million penalty.196 Compliance issues across the broader Riggs enterprise metastasized to such a level that Riggs eventually needed to be rescued by the bank PNC.197 A Senate investigation into money laundering practices at U.S. banks, including Riggs, resulted in provisions of the USA Patriot Act of 2001 that required updates to the AML provisions of Regulation K.198

While Riggs and BCCI are among the highest-profile examples of the money laundering risks from Edge banking, they are not the only ones. Shortly after the Riggs case, BSA/AML violations by American Express’s EAC, American Express Bank International of Miami, Florida (AEBI) resulted in a Deferred Prosecution Agreement with the Department of Justice (DOJ) that included forfeiture of $55 million, a $25 million fine by the Treasury Department’s Financial Crimes Enforcement Network (FinCEN), and a cease-and-desist order and $20 million penalty from the Fed.199 AEBI was used by Colombian drug cartels to facilitate the “Black Market Peso Exchange” scheme to launder $55 million in drug proceeds from 1999–2004.200 AEBI was also the subject of a Fed enforcement action and a DOJ settlement in 1993 and 1994, respectively, for BSA/AML violations related to the Mexican Gulf drug cartel.201

III. Where We Are: The Era of Modernization

The prevailing economic policy framework of the late 1980s and 1990s “subjugate[ed] both the governing agenda of American democracy and the direction of global economic development to the currents of international capital markets.”202 This period was marked by globalization in the form of liberalized international trade policy. The world’s major economies established the World Trade Organization (WTO) to manage trade relationships with an eye toward reducing barriers; trade relations between China and other major trading nations were normalized; and the U.S entered the North American Free Trade Agreement (NAFTA).203 Globalization was accompanied by financial “modernization” in the form of deregulation. In 1986, the U.K. enacted its “Big Bang” policy agenda of financial deregulation, temporarily giving London an advantage as the major global banking center.204

By 1996, seventy-three EACs and ACs, with total parent-only assets of $40 billion, were operating forty-two domestic branches.205 Overseas subsidiaries of U.S. banks grew in assets from $7 billion in 1970 to $81 billion by 1980, to $191 billion by 1990, and $718 billion by the end of 1998.206 As Table 4 shows, London was the most popular jurisdiction by the number of subsidiaries (110), just ahead of the Cayman Islands (106), as well as measured by total assets ($358.3 billion). Seventy percent of these assets—more than $500 billion—were being held in EACs.207

Table 4: Pre-Gramm-Leach-Bliley Landscape

Foreign subsidiaries of U.S. banks, 1998

|

Location |

Number |

Percent |

Total Assets ($bn) |

Percent |

|---|---|---|---|---|

|

Europe |

327 |

28.9 |

477.6 |

66.5 |

|

Offshore jurisdictions |

211 |

18.6 |

66.6 |

9.3 |

|

Latin America |

238 |

21.0 |

40.5 |

5.6 |

|

Asia/Pacific |

151 |

13.3 |

46.6 |

6.5 |

|

Middle East |

8 |

0.7 |

13.4 |

1.9 |

|

Africa |

12 |

1.1 |

1.0 |

0.1 |

|

Australia |

31 |

2.7 |

25.9 |

3.6 |

|

Canada |

36 |

3.2 |

20.9 |

2.9 |

|

U.S. territories & others |

60 |

5.3 |

9.8 |

1.4 |

|

U.S. |

59 |

5.2 |

15.6 |

2.2 |

|

Total |

1,133 |

100 |

717.9 |

100 |

Source: James V. Houpt, International Activities of U.S. Banks and in U.S. Banking Markets, 85 Fed. Res. Bull. 599 (1999).

While these international subsidiaries initially focused on traditional banking and lending, by the late 1990s they had shifted toward trading and securities.208 More than 60% of the $285 billion in U.S. commercial bank trading assets were booked abroad—in London and, to a lesser extent, Tokyo and Singapore.209

During this period, crises in the foreign exchange markets, driven by the volatility of the peso and ruble, caused the collapse of the hedge fund Long Term Capital Management (LTCM).210 LTCM was saved by public-private rescues, which was a necessity given its interconnectedness with Wall Street banks.211 The LTCM episode reinforced that the risks of international banking exposed during the Herstatt failure and the sovereign debt crisis of the 1970s remained present, this time mixed with the complexity of modern financial instruments known as derivatives.

Despite LTCM’s cautionary tale, U.S. banking policy in this period swung toward deregulation. Policymakers expanded the activities in which U.S. banks could engage, culminating in the repeal of the Glass-Steagall limits between banking and securities. As a result, EACs now engage in a range of banking and nonbanking activities, including nonfinancial activities that arguably violate the separation of banking and commerce. These expansions present new and significant challenges for regulating and supervising such sprawling financial enterprises.

A. International Banking and Financial Services Modernization

By the late 1990s, U.S. banks had shifted their international activities from facilitating trade and exports to trading securities and derivatives.212 The Financial Services Modernization Act of 1999, known as the Gramm-Leach-Bliley Act (GLBA), completed this transformation by permitting BHCs to conduct a broad range of financial activities, including securities underwriting and dealing, and insurance.213 BHCs were also allowed to engage in commercial activities that the Fed determined to be closely related to banking by making passive private equity-type merchant banking investments and directly owning commodities.214 GLBA generally envisions these activities being conducted through two vehicles, either a nonbanking subsidiary of a BHC or a financial subsidiary of a bank.

Like many of the laws discussed above, GLBA aspired to “make U.S. financial firms more competitive both domestically and internationally.”215 Notwithstanding U.S. banks’ ability to provide a wide range of services and activities abroad through their EACs, GLBA’s advocates argued that American preeminence in global financial markets would “come into question” if the limitations on banks’ activities remained in place.216 After GLBA, BHCs could engage domestically in any activity that they “engage in outside of the United States” that is “usual in connection with the transaction of banking or other financial operations abroad.”217

1. International Banking: A Growing Oligopoly

Many of EACs’ structural advantages were diminished with the repeals of the McFadden Act’s interstate branching restrictions and the Glass-Steagall Act’s activity limits.218 Table 5 shows that the number of EACs declined from ninety-four combined U.S. and Foreign Banking Organization (FBO) EACs in 2000 to forty-three EACs at the end of 2019. Since then, the number of new applications has been moribund, declining from fifty-two during the decade following the passage of the IBA, to nine during the 1990s, five during the 2000s, and four during 2011–2020.

Table 5: Post-Gramm-Leach-Bliley Realignment

Edge Act activity by decade, 1980-2020

|

Years |

Applications |

EACs |

||||

|---|---|---|---|---|---|---|

|

Total |

U.S. EACs |

FBO EACs |

Total |

U.S. EACs |

FBO EACs |

|

|

1981-1990 |

52 |

31 |

21 |

118 |

100 |

18 |

|

1991-2000 |

9 |

7 |

2 |

94 |

76 |

18 |

|

2001-2010 |

5 |

4 |

1 |

59 |

51 |

8 |

|

2011-2020 |

4 |

4 |

0 |

43 |

35 |

8 |

Source: Federal Register, Federal Reserve

This trend could suggest that the Edge Act has waned in popularity after GLBA authorized BHCs to engage in a wide range of financial, and even some nonfinancial, activities in the U.S. and abroad. More likely, the decline in the number of EACs reflects consolidation that occurred post-GLBA, particularly among the largest U.S. BHCs in which EAC ownership is concentrated.219 Due in part to the mergers that followed deregulation, the banking industry is more concentrated now than it was in 1990.220 Consistent with the broader trend toward concentration, the banking industry’s focus shifted from forming new EACs to reorganizing within the BHC structure.221

As shown by Table 6, the average U.S. Globally Systemically Important Bank (GSIB) now accounts for hundreds of billions of dollars in cross-border claims and is comprised of hundreds—if not thousands—of unique legal entities that operate across dozens of jurisdictions.222

Table 6: U.S. GSIB International Footprints

Systemic importance indicators, Q2 2021

|

GSIB |

Cross-border claims ($ billions) |

Legal entities |

Jurisdictions |

|---|---|---|---|

|

JPMorgan Chase |

$1,100 |

937 |

56 |

|

Bank of America |

$577 |

1,391 |

52 |

|

Citigroup |

$1,161 |

976 |

96 |

|

Wells Fargo |

$184 |

366 |

33 |

|

Goldman Sachs* |

$644 |

3,617 |

51 |

|

Morgan Stanley* |

$417 |

3,534 |

45 |

|

BNY Mellon |

$156 |

708 |

41 |

|

State Street |

$126 |

184 |

38 |

|

Total (Avg.) |

$546 |

1,464 |

52 |

Source: Federal Reserve form FR Y-15, FFIEC’s National Information Center

* = no EAC subsidiaries

While GSIBs’ domestic commercial banking subsidiaries hold an average of 62% of their total consolidated assets, nonbanking entities comprise approximately 99.85% of their legal structures.223

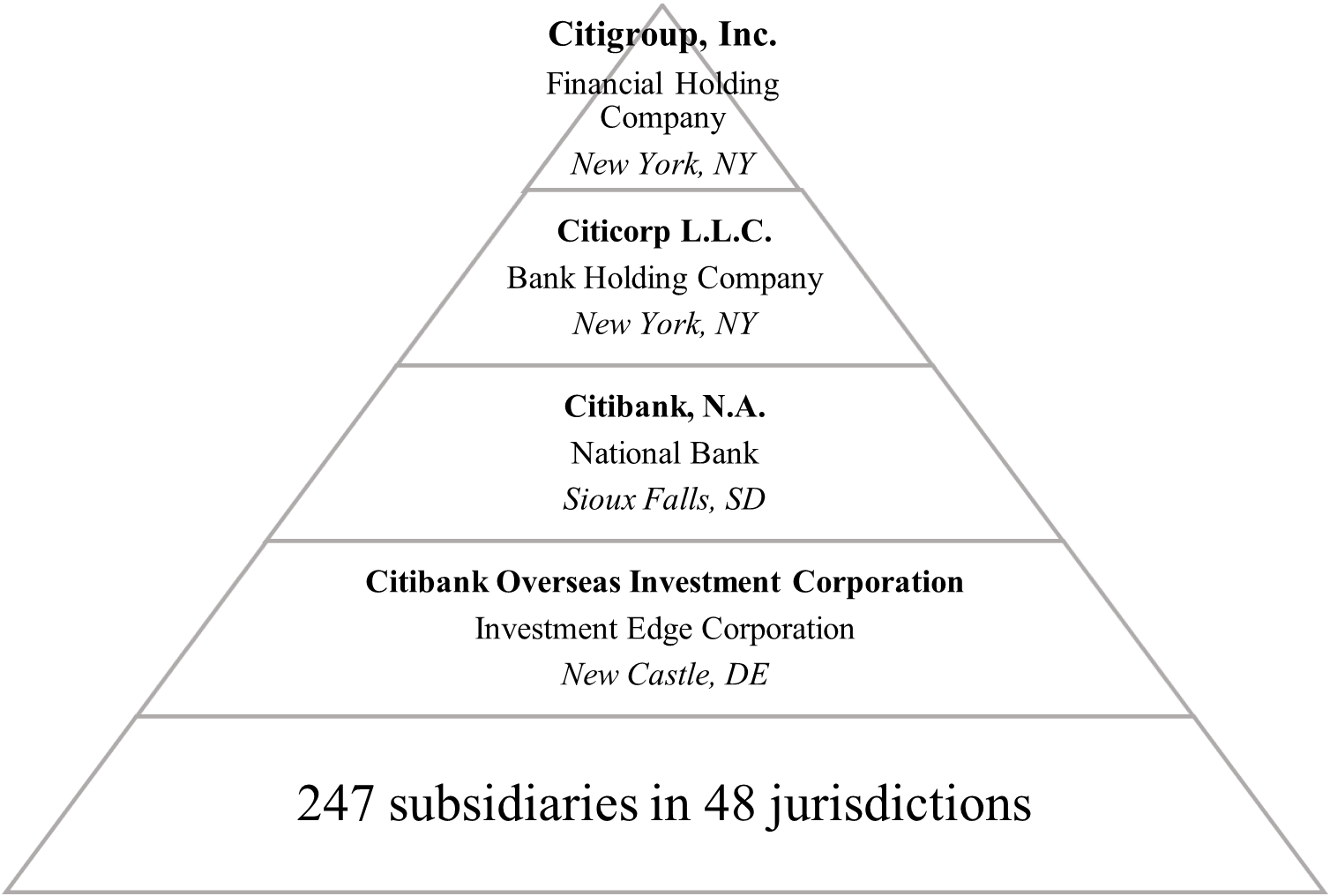

Ironically, a law that was meant to break up a monopoly on international banking has instead resulted in an international banking oligopoly. As seen in Table 7, most GSIBs have maintained EAC subsidiaries to serve as hubs for their global operations. In particular, “[s]ome of the largest U.S. GSIBs still hold their foreign bank and broker-dealer investments through an [EAC] underneath their main bank, reflecting the traces of history when that was the only structure possible.”224

Table 7: Vestiges of the Edge Act

EAC subsidiaries of U.S. GSIBs, Q2 2021

|

GSIB |

Edge Corporation |

State |

|---|---|---|

|

JPMorgan Chase |

JP Morgan International Finance Limited |

Delaware |

|

Bank of America |

BankAmerica International Financial Corporation |

California |

|

Citigroup |

Citibank Overseas Investment Corporation |

Delaware |

|

Wells Fargo |

Wells Fargo International Banking Corporation |

North Carolina |

|

Goldman Sachs |

-- |

N/A |

|

Morgan Stanley |

-- |

N/A |

|

BNY Mellon |

Mellon Overseas Investment Corporation |

Delaware |

|

State Street |

State Street International Holdings |

Massachusetts |

Source: FFIEC Nat’l Information Ctr.

Far from being obsolete, EACs evolved alongside the concentration and financialization that began in the 1980s and culminated with the passage of GLBA.225

2. Edge Corporations as Overseas Nonbank-Banks

EACs enjoy special legal status as overseas nonbank-banks. Nonbank-banks are “institutions that offer services similar to those of banks but which . . . conduct[] their business so as to place themselves arguably outside the narrow definition of ‘bank’[.]”226 Their sui generis treatment provides two advantages relative to traditional banks: (1) the ability to engage in more expansive nonbanking and nonfinancial activities; and (2) exemption from traditional structural restrictions, including the separation of banking and commerce.227

First, the Edge Act permits U.S. banks to engage in a wider range of activities abroad than those authorized domestically by GLBA, ostensibly in the name of competition.228 The Fed updated Regulation K after the passage of GLBA, liberalizing EACs’ permitted activities, providing greater latitude to operate without Fed approval, and relaxing solvency requirements and quantitative limits on investments.229 Regulation K enumerates at least nineteen unique activities that EACs may engage in abroad.230 In addition, EACs are authorized by reference to engage in the nonbanking activities that the Fed has determined are “so closely related to banking” as to be a “proper incident thereto” under Regulation Y.231 Regulation K also establishes the scope and conditions of the five categories of EACs’ permissible investments.232 Not limited to solely operating abroad, EACs may engage in at least seven different kinds of domestic banking and financing activities.233 Finally, the Fed may also authorize an EAC to engage in activities that it determines are “incidental to [its] international or foreign business” or “usual in connection with the transaction of the business of banking or other financial operations abroad.”234 In all, EACs are authorized to conduct more than fifty different types of banking and nonbanking activities, as well as nonfinancial activities that commingle banking and commercial business.

The alternative to the Edge Act structure—the foreign branch—is more common and more closely tied to the operations of the parent bank.235 With notice, banks, EACs, and nonbank affiliates within the BHC structure may establish foreign branches.236 Branches can offer more limited services and engage in more limited activities than EACs. In addition to the general banking powers available to a parent bank, branches are permitted to engage in eight defined activities, as well as any other activities that the Fed determines are “usual in connection with the transaction of the business of banking” in the branch’s host country.237 U.S. banks are expected to “supervise and administer their foreign branches and subsidiaries in such a manner as to ensure that their operations conform to high standards of banking and financial prudence,” including maintaining adequate recordkeeping and risk management practices.238 Thus, while the process of opening and operating foreign branches is less legally onerous than for EACs, foreign branches are also more limited in their potential.

In addition to their broad activities, because EACs are not considered banks, they are exempt from a variety of banking laws that preserve the independence and stability of depository institutions.239 Table 8 describes provisions from which EACs are exempt, including prohibitions against interlocking management, limits on product cross-marketing, and credit concentration limits.240 These provisions are important parts of a legal edifice erected to maintain the integrity, and prevent the misuse or abuse, of banks’ special financing powers.

Table 8: EACs as Overseas Nonbank-Banks

EACs’ banking law exemptions

|

Subject |

Provision |

Restriction |

|---|---|---|

|

Interlocking management & directors |

12 U.S.C. § 3204(2) |

Prohibits officers and directors from serving at multiple banks simultaneously |

|

Cross- marketing |

12 U.S.C. § 1843(k), (n) |

Prohibits banks from marketing products or services on behalf of companies, including commercial businesses, owned or controlled by merchant banking affiliates |

|

Deposit insurance |

12 U.S.C. §§ 1814-1818 |

Establishes minimum financial and managerial requirements for a depository institution to be eligible for deposit insurance |

|

Affiliate transactions |

12 U.S.C. §§ 371c & 371c-1 |

Establishes quantitative limits on transactions between banks and affiliates, and requires such transaction be on market terms |

|

Credit exposures |

12 U.S.C. § 84241 |

Limits unsecured and secured credit exposure to any one party to 15% and 25%, respectively, of a bank’s capital |

|

Dividend restrictions |

12 U.S.C. §§ 56, 60242 |

Prohibits banks from paying dividends in excess of annual net income without regulatory approval, or when a bank does not experience an annual profit |

While EACs are not considered “banks” for purposes of these restrictions, they benefit from exclusions from securities registration and commodities trading regulations applicable to bank products, including loan participations and swap products.243 Thus, EACs exist within a BHC structure and possess banking powers without being subject to the full range of obligations imposed upon banks and BHCs.

3. Containing Edge Corporations: Prudential Regulation and Supervision

In addressing the risks of international banking, Regulation K asserts that EACs should “at all times act in accordance with high standards of banking or financial prudence, having due regard for diversification of risks, suitable liquidity, and adequacy of capital.”244 An EAC must be “capitalized in an amount that is adequate in relation to the scope and character of its activities.”245

Banking EACs have a minimum 10% capital-to-risk-weighted-assets ratio, and 5% ratio of tier 1 capital-to-risk-weighted-assets.246 EACs are also subject to lending limits prohibiting them from financing trade acceptances in excess of 200% of their tier 1 capital or financing trade acceptances to a single borrower in excess of 10% of that capital.247 Banking EACs generally may not lend more than 15% of their tier 1 capital to any single borrower.248 However, credit extended by EACs is not combined with other bank transactions with the same borrowers for purposes of the National Bank Act’s lending limits, because doing so “would put . . . banks at a competitive disadvantage in the foreign markets.”249

EACs’ investment activities are subject to escalating scrutiny—in the form of general consent, limited general consent, prior notice, or specific consent requirements—depending upon their nature, size, and concentration.250 In order to make investments, an EAC must meet total and tier 1 capital ratios of 8% and 4%, respectively.251 EACs that are “well capitalized and well managed,” with tier 1 and total risk-based capital ratios of 6% and 10%, respectively, are provided wider latitude.252

With regard to supervision, EACs occupy a “unique position, since they are regulated and supervised solely by the Federal Reserve, irrespective of the agency supervising the parent institution.”253 Regulation K requires U.S. banking organizations to “supervise and administer” foreign subsidiaries to “ensure that their operations conform to high standards of banking and financial prudence.”254 EACs must maintain reports regarding their activities and condition, including regarding joint ventures entered into by the EAC, and make such reports available to both management and examiners.255 In general, the Fed is required to examine an EAC annually.256 These examinations are conducted at the head offices of the U.S. banking organization.257 The Fed’s supervisory approach for each EAC should be tailored to the entity’s activities, risk profile, and other attributes, according to a set of specific factors.258 Examinations of an EAC’s overseas operations must be conducted in coordination with the host country supervisor.259 Historically, the supervisory process has helped reveal some of the noncompliant, and potentially unsafe and unsound, EAC activities.260

GLBA required the Fed to defer “to the fullest extent possible” on reports and examinations conducted by a bank’s primary supervisory agency.261 Thus, if an EAC is a bank subsidiary, the primary regulator of the bank is the OCC, and the Fed largely defers to the OCC with respect to regulating that bank.262 GLBA’s proponents argued that functional regulation would “encourage and facilitate cooperation among the functional regulators,” while reducing “overlap between the various regulators” and clearly allocating “responsibility and accountability for supervising the different parts of new financial holding companies.”263 To ensure effective enterprise-wide supervision, the Fed was to have a “meaningful, albeit streamlined, level of umbrella oversight of the entire organization.”264

In practice, it is difficult for a single agency to acquire a complete picture of a banking conglomerate’s global operations.265 Under the balkanized U.S. regulatory structure, multiple agencies exercise either primary or backup supervisory authority, while home country and host country agencies share supervisory powers. With functional regulation and supervision of GSIBs being a virtual impossibility, the public supervision component of the public-private partnership has effectively been outsourced to private risk managers and “market discipline.”266

B. International Banking in the Global Financial Crisis

Experiences such as the Asian currency crisis of the 1980s demonstrated that “a crisis in the domestic banking industry quickly can turn into an international economic crisis.”267 Like all financial crises, the GFC had many causes and implications, but it was undoubtedly a “global” crisis in its origins, in the cross-border contagion that exacerbated its impacts, and in the subsequent financial reform effort.

1. Living Globally, Dying Locally

Many of the risks of the GFC were produced by a deregulatory push motivated by the desire to promote U.S. banks as “national champions.”268 By 2007, London was a world financial capital, accounting for 35% and 43% of global banks’ foreign exchange and derivatives activities, respectively.269 This was due in no small part to the comparative laxity of the U.K. in the regulation of wholesale funding markets.270

In addition, the cross-border nature of modern financial markets and institutions created vulnerabilities that influenced governments’ responses. The complexity and interconnections of the bankruptcy of the investment bank Lehman Brothers, including its overseas operations and derivatives business, risked igniting financial contagion.271 U.S. regulators sought to save Lehman Brothers by organizing a purchase by the U.K. bank Barclays, which U.K. regulators ultimately blocked, ostensibly to prevent the panic from spreading from the U.S. to Europe.272 These events were a reminder that, as one former Fed policymaker observed, “while internationally active banks live globally, they may well die locally.”273

The Fed’s Primary Dealer Credit Facility program made loans to support the repo trades of U.K.-based subsidiaries of U.S. investment banks Goldman Sachs, Morgan Stanley, and Merrill Lynch, and the U.S. universal bank Citigroup.274 U.S. banks also retrenched in their dollar-denominated lending to foreign banks, prompting the Fed to open currency swap lines with its foreign central bank counterparts.275 In a refutation of the argument that global diversification provided financial stability benefits, banks’ international operations and accompanying exposures emerged as a source of risk and instability.276

2. International Financial Reform: Dodd-Frank and Basel 3