A Disclosure Gap in the Market for Order Flow

Wholesalers in U.S. equity markets are once again a focus of the SEC and scholarly debate. In this Comment, building on the empirical work of Schwarz, et. al. (2022), I present a model of the broker-wholesaler relationship based on the duty of best execution under FINRA Rule 5310 and the antifraud provisions of the federal securities laws as well as public disclosures by brokers and wholesalers. I suggest that the arrangement between a broker and a wholesaler on any given day is determined by the technology of the wholesaler, the likelihood of adverse selection, and the overall strategy of the broker. As a broker negotiates arrangements with different wholesalers, it inevitably makes tradeoffs between average price improvement, likelihood of price improvement, likelihood of price disimprovement, speed, and other measures of execution quality. Unfortunately, under current SEC regulations, brokers are not required to articulate order-routing strategies in meaningful detail. Unlike in other parts of financial markets where there are strong incentives for self-induced disclosure, there is an inefficient disclosure gap in the market for order flow, because no broker knows whether the benefits of wholesaler-specific disclosure will accrue to them or their competitors. Ultimately, I conclude that the disclosure gap limits competition and prevents customers from effectively monitoring brokers, and I propose a regulatory solution. I also discuss the SEC’s recently proposed Order Competition Rule and amendments to Rule 605.

I. Introduction

Off-exchange market makers (i.e., “wholesalers”) in public equity markets have long been controversial among regulators,1 commentators,2 and the general public. By some measures, wholesalers save retail investors billions of dollars every year.3 Nonetheless, wholesalers operate in relative secrecy, and with the surge in retail trading activity over the past couple of years,4 there has been increasing pressure on the Securities and Exchange Commission (SEC) to regulate off-exchange trading more aggressively. For months, Chairman Gensler has proposed various equity market structure reforms to decrease fragmentation of U.S. equity markets and to increase competition for retail order flow.5 In fact, in a June 2022 speech, Chairman Gensler expressed concern that economic rents may accrue to wholesalers as they pay for marketable orders placed by retail investors.6 Other SEC commissioners expressed their own concerns.7 Ultimately, on December 14, 2022, the SEC proposed some of the most significant changes to equity market structure and broker-dealer regulation since the early 2000s.8 Moreover, increasing interest among regulators has been accompanied by increasing scholarly interest. Most notably, in a recent empirical study, Christopher Schwarz et al. found that wholesalers provide different levels of execution quality to different retail brokers.9

In this Comment, I argue that there is a disclosure gap in the market for order flow that limits competition and prevents retail investors from effectively monitoring brokers. Unlike exchanges and alternative trading systems, wholesalers are in constant communication with brokers. Their relationship is iterative, as brokers increase or decrease the amount of order flow sent to each wholesaler, and wholesalers adjust execution quality for each broker. Ultimately, the arrangement between a broker and a wholesaler on any given day is determined by the technology of the wholesaler, the likelihood of adverse selection, and the overall strategy of the broker. Unfortunately, under current SEC regulations, investors are entirely unaware of the broker-wholesaler arrangements negotiated on their behalf.10 While brokers have an incentive to voluntarily disclose overall execution quality,11 the expected marginal cost of disclosing their arrangements with individual wholesalers generally exceeds any expected marginal benefit for at least three reasons. First, retail investors have heterogeneous preferences that are difficult to predict. Second, with high fixed costs, extreme economies of scale and other barriers to entry, wholesalers may earn supracompetitive returns, and brokers likely worry that their competitors would have greater success in negotiations with wholesalers if they knew that wholesalers had the ability to provide better execution quality.12 Third, large wholesalers are sufficiently insulated from competition to withhold information on the execution quality they provide to other brokers.13 Consequently, even if customers had predictable, stable preferences, brokers would not know whether they would benefit from the disclosure of wholesaler-specific execution quality. In sum, no broker knows whether the benefits of wholesaler-specific disclosure will accrue to them or their competitors. Even so, retail investors would benefit substantially from wholesaler-specific disclosure because brokers would be forced to articulate their order-routing strategies in meaningful detail and communicate tradeoffs between metrics like speed, likelihood of price improvement, likelihood of price disimprovement and average price improvement. Most likely, retail investors would make a more efficient choice of broker.

In Part II, I describe U.S. equity market structure and Regulation National Market System (NMS). I also discuss some of the controversies surrounding wholesalers, and I briefly introduce the recently proposed SEC regulations. In Part III, I explore in depth the broker-wholesaler relationship, and I suggest that brokers make non-obvious tradeoffs in their negotiations with wholesalers. In Part IV, I describe the disclosure gap. To do so, I demonstrate that neither mandatory disclosure, under Rule 606 and Rule 605, nor voluntary disclosure provides individual investors with enough information to monitor brokers. In Part V, I explain the economics of broker disclosure, and I ultimately conclude that there is a market failure. Finally, in Part VI, I suggest a regulatory solution (i.e., mandatory disclosure of the tradeoffs made by brokers in their negotiations with wholesalers), and in Part VII, I discuss some of the implications of my research for the newly proposed SEC regulations.

II. Background

A. An Introduction to U.S. Equity Market Structure

Most individual investors place two types of orders with their broker: limit orders and market orders.14 Limit orders are orders to buy (or sell) stock at a price no greater (or lower) than a certain specified limit price. Limit orders resting on exchanges can be displayed to the rest of the market under the “market data rules” of Regulation National Market System (“Regulation NMS”).15 Marketable limit orders are limit orders that can be executed immediately at the national best bid or offer (i.e., the “NBBO”). Market orders are orders to buy or sell stock at the best available price.

After a customer places a limit order or a market order, a broker will route the order to one of three venues: an exchange, an alternative trading system (ATS) or an off-exchange market maker (i.e., a “wholesaler”).16 ATSs are trading systems that match buyers and sellers through a “matching engine” and are operated by broker-dealers. They are popular among institutional investors because there is generally no pre-trade transparency. While limit orders resting on so-called “lit” exchanges like NYSA ARCA and Cboe EDGX are displayed to the entire market as part of the NBBO, orders resting on an ATS are usually invisible to the market until they execute (though note that an exchange may have “dark” order types with no pre-trade transparency and an ATS may be required to report certain bids and offers to FINRA or a national securities exchange to be disseminated to the market).17

While exchanges and ATSs merely match buyers and sellers, wholesalers take inventory risk.18 To make money, wholesalers buy and sell shares throughout the trading day and collect a spread. Orders placed by retail investors are particularly valuable to wholesalers because the risk of adverse selection is low.19 That is, it is less likely that prices will move against a wholesaler after the wholesaler executes a trade. To attract retail orders, wholesalers will buy at higher prices and sell at lower prices (relative to the NBBO), resulting in billions of dollars of price improvement every year.20 Historically, brokers would internalize trades, but with decimalization and high frequency trading, the internalization business requires substantial upfront investment in sophisticated technology.21 Thus, there are high fixed costs and extreme economies of scale, leading brokers to outsource to a small number of wholesalers that have invested heavily in technology.22

B. Regulation “National Market System”

Regulation NMS is a set of rules passed by the SEC in 2005 pursuant to its authority under Section 11A of the Exchange Act that are “designed to modernize the regulatory structure of the U.S. equity markets.”23 There are five components of the regulation as originally passed. The order protection rule (Rule 611) restricts “trade-throughs” in NMS stocks (i.e., “the execution of trades on one venue at prices that are inferior to publicly displayed quotations on another venue”).24 The market access rule (Rule 610) prohibits a trading center from enforcing “unfairly discriminatory terms that prevent or inhibit any person from obtaining efficient access” to the quotations in an NMS stock displayed at that trading center through a member, subscriber, or customer of the trading center.25 Under the sub-penny rule (Rule 612), no market participant may “display, rank, or accept” an order in an NMS stock that is priced in an increment smaller than $0.01 if the order is priced equal to or greater than $1.00 per share.26 The market data rules provide for the dissemination of post-trade data and displayed quotes.27 Finally, under Rule 605, market centers must publish “standardized, monthly reports of statistical information concerning their order executions,” and under Rule 606, brokers must publish a report on their routing of non-directed orders in NMS stocks that are submitted on a held basis.28 Note that not all of the rules that form Regulation NMS were initially promulgated in 2005.29 Many predate the 2005 rulemaking and were merely reorganized by the SEC as part of Regulation NMS.30

The rules build on each other to accomplish the goals of Regulation NMS. The market data rules provide for the transmission of data on displayed quotes. Rule 611 (the order protection rule) ensures that brokers will access the best displayed quotes, and Rule 610 (the market access rule) makes those quotes accessible. Meanwhile, Rule 606 tells investors where their broker generally routes orders, and Rule 605 tells investors (and brokers) which market centers have the best execution quality (on average).

C. Wholesaler Controversies

Much of the controversy surrounding wholesalers is attributable to payment for order flow (“PFOF”) and segmentation.31 “PFOF” refers to payments made by wholesalers in exchange for retail order flow. Recall that retail order flow is attractive to wholesalers because adverse selection is less likely.32 PFOF is controversial because there is, at least theoretically, a conflict of interest for brokers. Every dollar of PFOF (i.e., every dollar paid to a broker) could be a dollar of price improvement (i.e., a dollar paid to a customer).33 Since at least the early 1990s, the SEC has said that, even though there is an “inherent” conflict of interest when brokers receive PFOF, PFOF is permissible under the securities laws and is not necessarily a violation of the duty of best execution or general agency principles.34

To address the conflict of interest, commentators have made a variety of proposals. Kelleher, et al. (2022), for example, recommends either a PFOF ban or a definition of “best execution” that is “more strictly focused on the best price available at the time of the trade, rather than using the misleadingly incomplete NBBO or the confusing and subjective multi-factor test that is currently used to assess compliance with the “‘best execution’ requirement.”35 In Part III, I suggest that there are necessary tradeoffs for any broker that routes customer orders and that a multi-factor test—though difficult to apply for both the SEC and brokers—is likely a necessary evil.

Another controversial issue is segmentation. “Segmentation” refers to “any practice by which a certain category of orders is identified and treated differently for execution than other categories of orders.”36 Wholesalers separate retail order flow from institutional order flow to lower the risk of adverse selection. For years, there has been a debate among regulators and in the scholarship as to the costs and benefits of segmentation.37

D. Proposed Regulations: Disclosure of Order Execution Information, Order Competition Rule and Regulation Best Execution

On December 14, 2022, the SEC proposed four regulations that would fundamentally change the relationship among retail investors, their brokers, and wholesalers. The regulations are complex, and my focus is on current equity market structure, rather than the SEC’s proposed reforms. Nonetheless, if adopted, the regulations will fundamentally restructure U.S. equity markets, so it is important to at least introduce them. The centerpiece of the proposed regulations is order-by-order auctions. Under the Order Competition Rule (Rule 615), with limited exceptions, a “restricted competition trading center” (like a wholesaler) may not execute a “segmented order” until after “a broker-dealer has exposed such order to competition at a specified limit price in a qualified auction operated by an open competition trading center.”38 The purpose of the regulation is to expose retail orders to greater competition, thereby increasing price improvement for the average order. There are two other regulations that are relevant to this paper: (i) proposed amendments to Rule 605 (which would require brokers to disclose detailed data on execution quality) and (ii) Regulation Best Execution (which would establish a best execution standard to supplement FINRA Rule 5310).

III. The Broker-Wholesaler Relationship

I will return to the SEC’s 2022/2023 regulations at the end of the article. In this section and Section IV, I argue that, under current SEC regulations, there is a significant disclosure gap in the market for order flow and customers could make a more efficient choice of broker if the disclosure gap were eliminated. Specifically, I suggest that brokers make non-obvious tradeoffs in their negotiations with wholesalers, and customers have little insight into those tradeoffs. To fully understand the disclosure gap, we will need some background on both the duty of best execution and the relationship between brokers and wholesalers.

A. The Complexities of Best Execution

The duty of best execution is ultimately traceable to the law of agency, but today, the duty of best execution is enforced more commonly under FINRA rules (specifically, Rule 5310) and the antifraud provisions of the federal securities laws.39 Under FINRA Rule 5310, “[i]n any transaction for or with a customer or a customer of another broker-dealer, a member [of FINRA] and persons associated with a member shall use reasonable diligence to ascertain the best market for the subject security and buy or sell in such market so that the resultant price to the customer is as favorable as possible under prevailing market conditions.”40 Moreover, a broker must conduct “regular and rigorous review of execution quality” at a minimum once every quarter. According to FINRA Rule 5310.09(b):

When conducting their reviews of execution quality, member firms should consider: (1) price improvement opportunities (i.e., the difference between the execution price and the best quotes prevailing at the time the order is received by the market); (2) differences in price disimprovement (i.e., situations in which a customer receives a worse price at execution than the best quotes prevailing at the time the order is received by the market); (3) the likelihood of execution of limit orders; (4) the speed of execution; (5) the size of execution; (6) transaction costs; (7) customer needs and expectations; and (8) the existence of internalization or payment for order flow arrangements.41

The SEC has provided similar guidance:

A broker-dealer must consider several factors affecting the quality of execution, including, for example, the opportunity for price improvement, the likelihood of execution (which is particularly important for customer limit orders), the speed of execution, and the trading characteristics of the security, together with other non-price factors such as reliability and service.42

Thus, brokers who mechanically route orders to the wholesaler or ATS that has provided, on average, the most price improvement fall short of their best execution obligations. Instead, each broker must measure and monitor a variety of factors (most notably, historical price improvement, historical price disimprovement, speed, and likelihood of execution) to determine whether their order-routing practices are adequate.

Crucially, a broker cannot optimize every execution quality metric for every trade. There are necessary tradeoffs, especially for less liquid stocks and larger trades. Consider, for example, Apollo Asset Management’s Series A preferred stock (ticker: AAM-A).43 According to Virtu and Citadel’s public disclosures,44 in October of 2022, Virtu received 53 marketable limit orders to buy or sell between 500 and 1999 shares.45 Virtu’s average order size in the 500-to-1999-shares bucket was about 780 shares.46 Citadel, meanwhile, received 49 marketable limit orders to buy or sell 500 to 1999 shares with an average order size of about 837 shares.47 For shares that received price improvement, Virtu provided share-weighted average price improvement of $0.0615 per share.48 In contrast, Citadel provided share-weighted average price improvement of only $0.0321 per share.49 For an 800-share trade, assuming that all 800 shares received price improvement, that is a difference of $23.52 (in October, AAM-A was trading at roughly $21 to $23 per share).50 That said, Citadel executed all of its orders in less than ten seconds, while about 23% of the orders (by shares) that were routed to Virtu and were not canceled were executed in ten or more seconds.51 In fact, about 2% of the orders routed to Virtu (again, by shares) were executed in thirty or more seconds.52 Moreover, about 37.76% of the orders routed to Virtu were executed at or outside of the quote, while about 28.89% of the orders routed to Citadel were executed at the quote (and no order was executed outside of the quote).53

Virtu and Citadel executed orders under different market conditions, so the data is not necessarily comparable. But even assuming reasonably similar market conditions, it is not at all clear which wholesaler provided better execution quality. Different brokers will make different inferences and will focus on different parts of the data. For shares that received price improvement, Virtu performed better than Citadel, but by the time Virtu executed many of its orders, the price could have moved against the investor, which likely would have forced Virtu either to take a loss or to execute the trade at an inferior price (or both). In addition, some shares received no price improvement (and a small fraction of the orders routed to Virtu – about 1.67% – were actually executed outside of the quote).54 It is possible that Virtu provided more price improvement simply because the price moved in favor of customers before Virtu executed many of the trades, but it is also possible that Virtu provided significantly more price improvement when prices moved in favor of customers and avoided price disimprovement when prices moved against customers (e.g., by taking a loss). To make matters more complicated, 45.8% of the orders submitted to Virtu were canceled, while 83% of the orders submitted to Citadel were canceled. For trades like these, determining whether Virtu or Citadel is the better market is not so simple.55

Differences between venues are not always so dramatic, but in the aggregate, there can be tradeoffs. In the first quarter of 2019, for orders to buy or sell between 1 and 99 shares (i.e., the quintessential retail order), Virtu provided on average and across all stocks $0.04 more in price improvement than Citadel per order ($0.58 v. $0.54 or a 7.4% difference).56 Nonetheless, Virtu provided price improvement on only 87.17% of orders to buy or sell between 1 and 99 shares, while Citadel provided price improvement on 96.03% of orders.57 Again, a broker that mindlessly routes to the venue with the greatest average price improvement misses crucial metrics of execution quality. The expected value of any savings depends on not only average price improvement but also the likelihood of price improvement, the reliability of the venue, and the speed of execution, among other factors. Some brokers may worry more about frequency of price improvement than about the amount of price improvement. Some brokers may care very little about speed. Others (especially those that route more thinly traded stock) may focus on price disimprovement, and as the AAM-A example illustrates, the tradeoffs made by a broker may be different for some stocks than for others. Finally, some brokers may analyze the data itself differently (e.g., by focusing on the standard deviation for price improvement rather than percent of shares that were price-improved). Brokers uniformly acknowledge the complexity of their order-routing decisions, and presumably, brokers all make different tradeoffs.58

B. An Overview of the Broker-Wholesaler Relationship

Best execution is especially complex in the broker-wholesaler context. For one, there is no pre-trade transparency, so brokers cannot simply route to the wholesaler that displays the best quote.59 In 1997, just before the adoption of Regulation ATS and at a time when off-exchange trading was much less common, Jonathan Macey and Maureen O’Hara wrote that “the concept of best execution should be an all inclusive one, recognizing that it is the total transaction costs (including the opportunity costs from failing to execute the trade in a timely manner) that is of concern to traders.”60 Nonetheless, they continued, “absent an explicit demonstration of other offsetting costs, the duty of best execution requires that the trade execute at the best prevailing price.”61 Today, brokers like Robinhood—that route essentially all of their order flow to wholesalers—need to predict execution quality, and as a result, they cannot simply choose to execute a trade at the best available price.62 Instead, brokers increase or decrease the amount of order flow they send to wholesalers based on historical execution quality. As Charles Schwab explains in its 2022 report on U.S. market structure, “wholesalers must compete on the basis of execution quality to win more flow,” and “[f]or this competition between wholesalers to stay dynamic, Schwab has invested in its own order routing capabilities to ensure that seamless routing changes from one wholesaler can be made based on execution performance.”63 In its S-1, Robinhood explains that it “routes orders to certain market makers for execution based on [its] order routing system, which uses an algorithm to determine which market maker is most likely to provide the best price for each customer’s order based on the market maker’s historical performance.”64 Moreover, Robinhood reviews execution quality “based on a number of factors . . . including, where applicable, but not necessarily limited to, speed of execution, price improvement opportunities, differences in price disimprovement (i.e., situations in which a customer receives a worse price at execution than the best quotes prevailing at the time the order is received by the market), likelihood of executions, the marketability of the order, size guarantees, service levels and support, the reliability of order handling systems, client needs and expectations, transaction costs and whether the firm will receive remuneration for routing order flow to such market makers.”65 To effectively review the historical performance of wholesalers, brokers consider a variety of factors, and a broker cannot optimize every execution quality metric for every trade. Instead, brokers make non-obvious tradeoffs.

To further complicate the analysis, brokers need to consider the technological capabilities of wholesalers. Fidelity explains in its voluntary disclosures that, in routing to certain market makers, it considers whether the “market makers can handle the order flow Fidelity may send them, especially in volatile market conditions.”66 Even a wholesaler that is statistically likely to provide the best price given its historical performance may ultimately provide inferior execution quality if the wholesaler has inadequate or underdeveloped technology. In addition, brokers develop relationships with wholesalers, and they will route fewer orders to wholesalers they believe to be uncooperative or unaccommodating. Fidelity suggests that it is more likely to route to a wholesaler if the wholesaler provides “exception reports with follow-up action items” and is “willing . . . to ‘make good’ on orders in the event of system problems.”67 Over time, as wholesalers provide different levels of execution quality, invest in technological improvements, and cooperate with requests, brokers make iterative adjustments in the amount of order flow they route to each wholesaler.

Wholesalers, for their part, adjust execution quality either to “win more flow” (as described by Schwab68 ) or to compensate for the risk of adverse selection. In a recent study, Christopher Schwarz et al. found that wholesalers systematically provided different levels of price improvement to different brokers.69 They also found that “current PFOF is too small to explain the variation in price improvement across brokers and, in the cross-section, is unrelated to the quality of price improvement across the brokers we analyze.”70 Instead, they offer three other explanations. First, “to benefit from economies of scale, market centers may compete more aggressively for order flow from brokers with large aggregate orders.”71 Second, some order flow may be less correlated with future price movements (i.e., there may be less adverse selection). Third, “brokers who care about dimensions other than price improvement might receive systematically worse price improvement.”72 I would restate this third reason: as brokers inevitably make tradeoffs between speed, average price improvement, reliability, and other measures of execution quality, wholesalers respond by iteratively increasing or decreasing each measure of execution quality.

The important point is that we should expect broker-wholesaler arrangements to evolve as brokers re-route order flow in response to execution quality and wholesalers adjust execution quality to attract more order flow and to compensate for adverse selection. As discussed in the following sections, individual investors have virtually no insight into the iterative adjustments made on their behalf or even the strategies behind those adjustments, and the lack of any wholesaler-specific disclosures is a meaningful disclosure gap with important implications for competitive dynamics in the market for order flow.

IV. A Disclosure Gap in the Market for Order Flow

A. Mandatory Disclosure

The only order-routing information required to be disclosed under Regulation NMS is the information required by Rule 605, Rule 606, and Rule 607.73 Rule 607 requires brokers to disclose their PFOF arrangements with wholesalers.74 Under Rule 606(a), brokers are required to publish a report every quarter on their routing of “non-directed orders in NMS stocks that are submitted on a held basis.”75 A “directed order” is “an order from a customer that the customer specifically instructed the broker or dealer to route to a particular venue for execution.”76 Thus, the report is limited to orders over which the broker at least had some discretion. Rule 606(a) also excludes orders submitted on a “not held basis.”77 With orders submitted on a not held basis, brokers have time and price discretion, and as commenters to a 2018 amendment to Rule 606 explained, “institutional investors in particular rely on such discretion for reasons such as minimizing price impact.”78 In other words, an institutional investor will submit a large order on a not held basis, so that its broker may gradually execute the order without leaking information to the market (and for other reasons). The broker will measure the price their customer received against a volume-weighted average price (VWAP).79 That process, however, is generally not relevant to retail investors (who usually submit small orders and are not worried about issues like information leakage). Therefore, 606 reports are limited to non-directed orders submitted on a held basis.

In the report, a broker must disclose information about the “ten venues to which the largest number of total non-directed orders . . . were routed for execution” and “any venue to which five percent or more of non-directed orders were routed for execution.”80 Most importantly, the broker is not required to disclose the execution quality provided by each venue or the reason the broker routed to particular venues. Instead, the broker is required to disclose only the percent of non-directed orders, market orders, marketable limit orders and non-marketable limit orders routed to each venue along with certain conflicts of interest (e.g., “a description of any arrangement for payment for order flow and any profit-sharing relationship and a description of such arrangements, written or oral, that may influence a broker’s or dealer’s order routing decision”).81 Customers may also request additional information on orders they submitted to their broker under 606(b), but they are entitled to information related only to the orders they submitted.82 It would be exceedingly difficult to understand the tradeoffs made by brokers in routing to certain wholesalers.

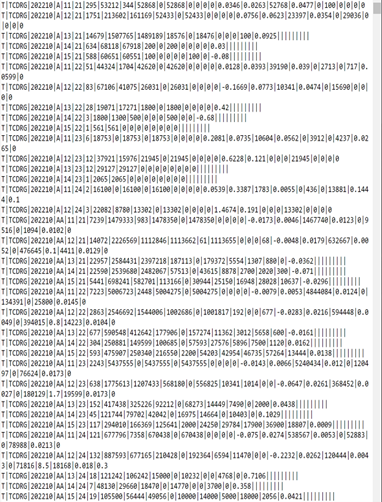

A retail investor interested in wholesaler-specific execution quality would have to access the Rule 605 report filed by each venue listed in the 606 report. Unlike in 606 reports, the data in 605 reports is not organized in a labeled table for the convenience of investors.83 In fact, to the average individual investor, the data presented in 605 reports is absolutely impenetrable. The very beginning of Citadel’s 605 report is reproduced below.

To decipher the report, an individual investor would need to locate the Joint-SRO Plan entered into under the predecessor to Rule 605 (Rule 11Ac1-5).84 Only then would the individual investor know, for example, that a row marked “11” includes only market orders and a row marked “21” includes only orders involving 100 to 499 shares.85 Crucially, 605 reports do not include orders to buy or sell fewer than 100 shares, so the data on execution quality most valuable to individual investors is not even included in the report.86

Even if an individual investor could compile the 605 data, reference the 606 report and track differences in speed, price improvement and reliability over time and even if they were interested only in orders involving 100 or more shares, there would still be no data on the bilateral arrangements negotiated between a broker and a wholesaler. Instead, the investor would only know the aggregate execution quality provided by each wholesaler for each stock. Specifically, for market orders and marketable limit orders, an individual investor would know (averaged across all brokers and for each equity) statistics like the average effective spread, the cumulative number of shares of covered orders executed with price improvement and (for shares executed with price improvement) the share-weighted average amount per share that prices were improved.87 For all covered orders (not merely market orders and marketable limit orders), the investor would know (again, averaged across all brokers and for each equity) statistics like the number of shares executed at the venue (versus another venue), the average realized spread and the number of shares executed within certain timeframes.88 The SEC when it initially promulgated Rule 605 explained that the data on execution speed is “intended to provide a substantial basis to weigh any potential trade-offs between execution speed and execution price.”89 Nevertheless, without broker-specific information, it would be impossible for the individual investor to make any meaningful comparisons between, e.g., the arrangement Robinhood negotiated with Citadel and the arrangement Fidelity negotiated with Citadel. Certainly, an individual investor has no insight into the tradeoffs made by their brokers between metrics like reliability, average price improvement, average price disimprovement, and speed.

B. Voluntary Disclosure

In addition to 606 and 605 reports, brokers and wholesalers also voluntarily disclose some data on execution quality. But even with the voluntarily disclosed data, there is a meaningful disclosure gap. Below I summarize the voluntary disclosures made by a sample of retail brokers.90 Note that none of the brokers I consider disclose wholesaler-specific execution quality or stock-specific execution quality.

1. Broker Websites

a) Robinhood

Robinhood provides three numbers on its website: (1) net price improvement per 100 shares; (2) the percent of orders executed at the NBBO or better; and (3) the effective spread for Robinhood orders over the quoted spread.91 In calculating the percent of orders executed at the NBBO or better and the effective spread over the quoted spread, Robinhood excludes orders with “a fractional share component.”92

b) Charles Schwab

Schwab discloses (1) the percent of shares executed at the quote or better; (2) the percent of shares that received price improvement; (3) average savings per order (i.e., average price improvement); and (4) average execution speed. Schwab also organizes the data by order size (“1 - 99 orders”, “100 - 499 orders”, “500 - 1,999 orders” and “2,000 - 4,999 orders”).93 Schwab only reports execution quality for S&P 500 stocks.

c) Fidelity Investments

Fidelity discloses (1) the percent of shares executed at the quote or better; (2) the percent of shares that received price improvement; (3) average savings per order (i.e., average price improvement); (4) average execution speed; and (5) average effective spread.94 Fidelity provides aggregate data on its website, but like Schwab, Fidelity also organizes the data by order size (“1 - 99 orders”, “100 - 499 orders”, “500 - 1,999 orders” and “2,000 - 4,999 orders”). For each order-size bucket, Fidelity also provides an average order size.95 Fidelity claims that all of its orders for NASDAQ and listed shares are executed in nine seconds or less, and it discloses average price improvement for a 100-share order and a 1,000-share order.96 Finally, Fidelity organizes the data into two sets of aggregate data: one set for S&P 500 stocks and one set for non-S&P 500 stocks.

d) Vanguard

Much like Robinhood, Vanguard discloses three numbers on its website: (1) the effective spread for Vanguard orders over the quoted spread; (2) the average savings per a 100-share order; and (3) the percent of orders for Vanguard ETFs executed at midpoint.97 The effective spread over quoted spread (“E/Q”) data is limited to “market orders on the S&P 500 Index sizes 100 - 499.”98

e) Interactive Brokers

Interactive Brokers is unique. Unlike other retail brokers, it discloses the average difference between the volume-weighted average price (VWAP) for a security and the price received by its customers. It then divides that amount by the total trade value to arrive at the “net expense as a percent of trade value.”99 Interactive Brokers claims that other “industry-touted statistics” only “discuss the percent of orders that saw price improvement, and conveniently ignore the percentage of their orders that were dis-improved or had no improvement.”100 Interactive Brokers also discloses average order size (both by dollar value and by number of shares).101

f) E*Trade

E*Trade discloses (1) the percent of shares executed at the quote or better; (2) the percent of shares that received price improvement; (3) average savings per order (i.e., average price improvement); (4) average execution speed; and (5) average effective spread.102 E*Trade also divides the data into S&P 500 stocks and non-S&P 500 stocks, and it reports data only for orders with 100 to 9,999 shares.

g) TD Ameritrade

TD Ameritrade discloses (1) the percent of orders price improved; (2) net price improvement per share in the 1-1,999-orders bucket multiplied by 100 shares; (3) a “liquidity multiple” (i.e., the average size of order execution at or better than the NBBO at the time of order routing, divided by average quoted size103 ); and (4) average execution speed for market orders.104 TD Ameritrade’s statistics cover “market orders in exchange-listed stocks 1-1,999 shares in size.”105

2. FIF Supplemental Retail Execution Quality Statistics

In January of 2018, the Financial Information Forum (“FIF”) brought together retail brokers and wholesalers “to review the historical reporting requirements of Rule 605.”106 FIF advocates for amendments to Rule 605, and it is referenced throughout the SEC’s recently published notice of proposed rulemaking.107 In addition to its advocacy work, FIF encourages brokers and wholesalers to make standardized disclosures of execution quality. FIF’s website currently includes disclosures from Fidelity (a retail broker) and Two Sigma Securities (a wholesaler),108 but I have also found earlier FIF disclosures from Citadel109 and Virtu110 elsewhere on the internet. I referenced those disclosures earlier in this section. The wholesaler disclosures add data on smaller orders, which is certainly helpful, and they also summarize execution quality. Specifically, in an FIF report, brokers and wholesalers disclose (i) the percent of shares executed at the quote or better; (ii) the percent of shares that received price improvement; (iii) average savings per order; and (iv) average execution speed. They also organize the data by order size (1 - 99 shares, 100 - 499 shares, 500 - 1,999 shares, 2,000 - 4,999 shares and 5,000 - 9,999 shares), and they provide an average order size for each bucket. The data I described in the “Fidelity Investments” section is pulled in part from Fidelity’s FIF report.

Most brokers, however, have not provided FIF data.111 Instead, brokers disclose a few aggregate measures of execution quality. No broker meaningfully discloses data on its relationships with individual wholesalers.

C. The Disclosure Gap

There is a meaningful disclosure gap. Individual investors generally know that their broker provides a certain amount of price improvement on average, executes orders at a certain speed on average, and provides price improvement for a certain percent of orders. They also know which wholesalers execute orders routed by their broker, and they know the execution quality provided on average by each of those wholesalers (but not the execution quality provided by a wholesaler to their specific broker). Some (but not all) brokers provide data on execution quality by order size, and some brokers separate S&P 500 stocks from non-S&P 500 stocks. Nevertheless, an individual investor choosing between two brokers still cannot know the tradeoffs made by each broker in its negotiations with wholesalers and the willingness of each wholesaler to provide better price improvement, speed, or reliability to each broker. Thus, it is difficult to know (i) whether the aggregate data disclosed by each broker is predictive of the execution quality the individual is likely to receive for any given trade (or whether it merely reflects, e.g., the stocks that are popular among customers of the broker); and (ii) whether the aggregate data disclosed by each wholesaler is predictive of the execution quality the individual is likely to receive for any given trade (or whether it reflects the superior execution quality provided to a competitor).

The disclosure gap is particularly significant for non-S&P 500 stocks, which vary widely in volatility and liquidity. For example, Interactive Brokers (which markets to more sophisticated traders) likely trades less well-known (and perhaps less liquid) stocks.112 Commentators, regulators and industry participants have noted a growing concentration of liquidity in U.S. equity markets among just a few stocks.113 More liquid stocks have greater trading interest on both sides of the market, so it is easier for wholesalers to consistently buy at higher prices and sell at lower prices. Therefore, brokers with customers who trade more liquid stocks are likely to receive better execution quality.

The NBBO itself is also an imperfect measure of the liquidity available in the market, so it will be difficult to understand differences between brokers based solely on average price improvement across all S&P 500 (or non-S&P 500) stocks relative to the NBBO. A limit order may be displayed as the NBBO if and only if the limit order is a “round lot” (i.e., an order to buy or sell at least some specified number of shares).114 As a result, the NBBO can be underinclusive (i.e., it may not include odd-lot quotes that are substantially better than the NBBO), and it can be overinclusive (i.e., there may not be sufficient depth of liquidity in public equity markets to avoid price disimprovement relative to the NBBO).115 To assist brokers in making stock-by-stock routing decisions, third-party data analytics providers frequently provide a volume-weighted BBO.116 The NBBO also excludes dark liquidity. Consequently, even assuming brokers separate their execution quality for S&P 500 stocks from their execution quality for non-S&P 500 stocks, it still will be exceedingly difficult to compare the tradeoffs made by one broker to the tradeoffs made by another broker. Customers simply cannot effectively monitor the iterative adjustments made by brokers on their behalf.

To be a little more concrete, imagine that an individual investor is choosing between Robinhood and TD Ameritrade. Robinhood reports in its voluntary disclosures that 84.67% of its orders (by shares) are executed at the NBBO or better, and its customers receive an average of $1.74 of price improvement per 100 shares.117 TD Ameritrade, meanwhile, reports that 98.5% of its orders (by shares) are executed at the NBBO or better, and its customers receive an average of $1.32 of price improvement per 100 shares.118 Even assuming that the metrics are comparable, a customer still cannot know whether more price improvement at TD Ameritrade but less reliability is attributable to the arrangements negotiated with wholesalers or simply the stocks that are popular among TD Ameritrade customers (or, for that matter, the size of TD Ameritrade orders). Moreover, to confidently make inferences about order-routing practices, a customer would need to reference earlier execution quality reports and search for trends over time. In contrast, if TD Ameritrade and Robinhood disclosed execution quality by wholesaler over time (and accompanied their disclosure with some commentary), customers could see tradeoffs made by brokers in real time and, on that basis, determine which broker is a better agent in light of their preferences.

Even if a customer could infer some tradeoffs from the aggregate data provided by their broker, it would require unnecessary and inefficient effort for each individual investor to truly understand the differences between, e.g., Fidelity order-routing strategies and Schwab order-routing strategies. Ideally, brokers would disclose wholesaler-specific arrangements along with any adjustments they have made over time (based on differences in speed, average price improvement, etc.). Individual investors could evaluate those adjustments and determine which broker is the better agent (given the preferences of the investor). In other words, wholesaler-specific disclosure (as described in greater detail in Section VI) would allow individual investors to understand some of the nuances of order-routing strategies with very little effort.

For some time, the SEC has considered regulations that would require brokers to fully and efficiently disclose the tradeoffs they make to individual investors. It is a difficult question of regulatory design since the SEC needs to “avoid the dangers of overly general statistics” while still disclosing useful data to individual investors and maintaining low compliance costs for brokers.119 The predecessor to Rule 606—Rule 11Ac1-6—as originally proposed would have required a “narrative section” that “discusses and analyzes . . . order routing practices.”120 Ultimately, “to maintain the brevity and reduce the compliance burdens of the reports,” the SEC abandoned the “narrative section.”121 Similarly, the SEC’s newly proposed regulations would require broker-specific, stock-by-stock disclosure along with a summary of execution quality.122 In my view, wholesaler-specific disclosure (in combination with aggregate execution quality and a discussion of the reasons brokers increased or decreased the amount of order flow routed to each wholesaler) would strike a good balance: investors could review easily understandable aggregate data that still adequately communicates the tradeoffs made by each broker. The most important responsibility of a broker is to determine which wholesalers will execute which orders, and it is impossible for a customer to determine which broker is more likely to meet their specific preferences in routing to different wholesalers unless the customer has some insight into the arrangements negotiated with wholesalers. In Section VI, I will propose a specific regulation based on this general framework.

V. The Economics of Disclosure

For the analysis to be complete, we need to know whether brokers fail to disclose wholesaler-specific data because the market is inefficient or whether extra disclosure (in spite of the discussion above) simply would not increase overall utility in the market for order flow. We should expect brokers to disclose wholesaler-specific execution quality if the expected marginal benefit of disclosure is greater than the expected marginal cost. To conduct a marginal analysis, it will be helpful to compare voluntary disclosure by brokers with voluntary disclosure in another context: companies seeking capital. Nearly forty years ago, Easterbrook and Fischel observed that firms have strong incentives to voluntarily disclose financial information to shareholders, and in the years since, there has been growing empirical evidence that equity financing increases incentives for voluntary disclosure.123 If a firm would like to finance a project, it needs to provide information for investors to be interested. Ultimately, by disclosing information, the firm will “coordinate the acts of many investors who could not bargain directly.”124 That is not to say, of course, that mandatory disclosure is unnecessary in securities markets. There are limits to the principle of self-induced disclosure, including (i) that firms cannot charge for certain types of information and (ii) that no firm has the appropriate incentives to create the least-cost formula for disclosure.125 Nonetheless, it is a helpful conceptual framework for an analysis of voluntary disclosure by brokers.

The principle of self-induced disclosure seems to be at work in the market for order flow. There is no need for customers to bargain with brokers for disclosure of general data on execution quality. Higher-quality brokers (e.g., brokers with better overall price improvement, speed, and reliability) will disclose enough information to individual investors to distinguish themselves from lower-quality brokers. Moreover, once a broker discloses, it has an incentive to continuously disclose since, otherwise, individual investors will assume the broker no longer has marketable execution quality.

The logic of self-induced disclosure does not extend to wholesaler-specific disclosure. For one, the logic rests on an assumption that investor preferences are predictable. In public equity markets, investor preferences generally are predictable. If the present value of future cash flows for Firm 1 is higher than the present value of future cash flows for Firm 2, then Firm 1 will be more valuable and will have an incentive to distinguish itself from Firm 2. Some firms will have higher betas (and thus more volatile returns), but assuming that borrowing costs are not too high, the investor should be mostly interested in risk-adjusted returns.126 In contrast, execution quality, as explained in Part III, is not so simple. Customers have predictable preferences for overall execution quality (e.g., customers prefer more price improvement as compared to less and faster execution as opposed to slower). That said, brokers need to make non-obvious tradeoffs, and customers presumably have heterogeneous preferences with respect to those tradeoffs. The firm with a more attractive project knows that it will lower its cost of capital by disclosing information on the project to the market.127 Similarly, a broker with better aggregate execution quality is likely to increase revenue by disclosing execution quality to the market. But the expected marginal benefit of disclosing the tradeoffs made by the broker in its negotiations with wholesalers does not obviously exceed the expected marginal cost. Customers may be surprised if, e.g., their broker re-routes order flow from the wholesaler that provides better but less frequent price improvement to a wholesaler that provides worse but more frequent price improvement. Without more information on customer preferences (which may be costly to obtain and would be useful only until those preferences change), a broker is unlikely to disclose wholesaler-specific execution quality.

In addition, if a broker discloses the execution quality provided by a wholesaler, it could benefit its competitors in negotiations with the same wholesaler. There are reasons to believe that wholesalers earn supracompetitive returns. There are high fixed costs and massive economies of scale in the wholesaler business, so wholesalers are somewhat insulated from competition. In fact, according to Hu and Murphy (2022), Citadel and Virtu alone account for about 70% of retail order flow.128 The SEC estimates that Citadel and Virtu captured “approximately 66% of the executed share volume of wholesalers as of the first quarter of 2022.”129 In Robinhood’s 606 report for the third quarter of 2022, Citadel and Virtu together accounted for over 86% of its non-directed S&P 500 order flow.130 Hu and Murphy (2022) calculate the Herfindahl-Hirschman Index (HHI) for the “internalizer market”.131 They conclude that the “average internalizer HHI has significantly increased over time, from a low of 2,450 in 2018 to a high of 2,900 in 2021, for an overall change of 450 points.”132 In comparison, “the US Department of Justice (DOJ) considers a marketplace to be moderately concentrated if the HHI is between 1,500 and 2,500, and highly concentrated if the HHI is greater than 2,500.”133

Extreme concentration is entirely predictable. To attract order flow, wholesalers generally need to make substantial upfront investments in their trading systems. Brokers frequently hesitate to route more order flow to smaller wholesalers because those wholesalers have not invested as much in technology and may not have the sophistication to handle increased order flow or more volatile order flow.134 Schwab explains that it routes to wholesalers because they “heavily invest in technologies and risk management” and have “invested in specific capabilities including better inventory risk management, increased capital commitment, smart order routing to source more hidden liquidity in the marketplace, and robust order management and risk management systems.”135 The implication is that a competitor cannot just enter the market one day and exert competitive pressure, and even among existing wholesalers, to take market share from a larger wholesaler, a smaller wholesaler needs to invest aggressively upfront, which can be costly if the smaller wholesaler ultimately fails to capture greater market share. A little less intuitively, in addition to high fixed costs and extreme economies of scale, the value of a wholesaler may increase the more retail brokers route to the wholesaler. For one, wider spreads on some stocks (or on orders routed by one broker) may subsidize narrower spreads on other stocks (or on orders routed by another broker). A larger wholesaler may take a loss periodically to maintain their relationship with a broker.136 The result is that large wholesalers may be somewhat insulated from competition (and thus earn supracompetitive returns).

Nonetheless, if a broker discovers that another broker receives better execution quality at the same wholesaler (in spite of similarities in adverse selection, the stocks that the brokers trade, and other relevant factors), there are ways for the broker to exert pressure on the wholesaler. The broker could signal to other wholesalers that it will route more orders to them, encouraging them to make the necessary upfront investments to leverage economies of scale and thus to compete with larger wholesalers like Citadel and Virtu (of course, the success of this strategy would turn on whether (1) the broker is large enough to exert meaningful pressure or (2) other brokers follow). Most likely, some brokers have simply been more successful than others in negotiations with Citadel and Virtu, resulting in systematically different levels of price improvement for each broker, and more information on the execution quality provided to competitors would increase their leverage.137 Thus, there are strong incentives for brokers not to signal to their competitors that large wholesalers have the ability to provide better execution quality. Note that, even though brokers have access to aggregate execution quality data in 605 reports, they cannot know the execution quality provided to individual brokers. Note also that the hypothetical broker conducting a marginal analysis need only worry that its competitors will benefit from disclosure. The logic applies, even if wholesalers are not actually earning supracompetitive returns.

Even if brokers knew the preferences of their customers, those preferences were reasonably stable, and brokers had no reason to believe competitors would use wholesaler-specific data to their advantage, brokers still would not disclose unless they believed it would provide a competitive advantage, and brokers are generally unaware of the execution quality provided to their competitors by each wholesaler. Schwarz, et. al. (2022) reported that, in their conversations with brokers, “brokers indicated they could not have predicted their relative ranking in our study.”138 Most likely, given that large wholesalers like Citadel and Virtu are somewhat insulated from competition, it would be difficult for brokers to negotiate for data on the execution quality provided to competitors.

Note finally that, unlike in other parts of financial markets, retail investors cannot simply free ride off more sophisticated institutional investors. The whole purpose of the broker-wholesaler relationship is to separate retail order flow from institutional order flow and thereby reduce the likelihood of adverse selection.139 To the extent institutional order flow is mixed with retail order flow, institutional investors generally submit a much more statistically significant sample of trades to their broker, so it is easier for them to monitor. Moreover, literal bargaining between retail investors and brokers is exceedingly unlikely. Therefore, given that (1) customers have heterogeneous preferences that are difficult to predict, (2) competitors may use wholesaler-specific disclosure to their advantage and (3) brokers are unable to determine whether a particular wholesaler provides better execution quality to other brokers, market mechanics alone are unlikely to prompt wholesaler-specific disclosure, even though wholesaler-specific disclosure would improve overall welfare.

VI. A Mandatory Disclosure System

Thus far, I have argued that (i) brokers make non-obvious tradeoffs in their negotiations with wholesalers, (ii) customers have little insight into those tradeoffs, and (iii) brokers have no incentive to disclose those tradeoffs voluntarily. The simple solution, then, is mandatory disclosure. Brokers should be required to disclose their arrangements with wholesalers and the iterative adjustments they make on behalf of their customers. Customers would then evaluate those adjustments and choose the broker they believe to be their best agent (given their preferences for certain tradeoffs in execution quality). By mandating wholesaler-specific disclosure, the SEC would reduce agency costs, allow customers to make a more efficient choice of broker and encourage brokers to compete for customers based on their order-routing strategies.

A more efficient disclosure system would have two parts: one part focused on aggregate execution quality and another part focused on wholesaler-specific execution quality. In the part focused on aggregate execution quality, brokers would make monthly stock-specific Rule 605 disclosures, much like wholesalers, and they would summarize the 605 data in an easily understandable format. In the part focused on wholesaler-specific execution quality, brokers would make their quarterly Rule 606 disclosures, but in addition to disclosing the percent of orders routed to each wholesaler, brokers would disclose for each wholesaler, separated into S&P 500 stocks and non-S&P 500 stocks and separated into five different size buckets (i.e., 1-99, 100-499, 500-1,999, 2,000-4,999, 5,000-9,999): (1) the average effective spread; (2) for shares executed with price improvement, the share-weighted average amount per share that prices were improved; (3) the percent of shares executed at the quote or better; (4) the percent of shares executed with price improvement; (5) the average speed of execution for market orders and marketable limit orders; and (6) any other data necessary to explain their decision to re-route order flow from one wholesaler to another wholesaler. At the top of the report, each broker would provide a concise explanation of its decision to re-route order flow from one wholesaler to another wholesaler along with a general assessment of the performance of each wholesaler.

Of course, as explained in Section III, the decision to re-route order flow from one wholesaler to another wholesaler can be incredibly complex, so a disclosure accessible to retail investors is unlikely to capture the many nuanced differences between brokers. Nonetheless, there are undoubtedly general trends (e.g., perhaps Virtu has provided greater price improvement for smaller orders to buy or sell stocks with deep liquidity but Citadel has executed at a much better price for larger orders to buy or sell thinly traded stocks). If a broker has received inferior execution quality from a wholesaler, the broker will have every incentive to explain inferior execution quality by disclosing useful information about orders routed to each wholesaler (e.g., that many of the orders routed to a particular wholesaler were for illiquid stock).

VII. 2022/2023 Regulations

It is worth considering whether the SEC’s proposed Order Competition Rule (Rule 615) and proposed amendments to Rule 605 solve any of the problems I have discussed. Recall that, under proposed Rule 615, with limited exceptions, a “restricted competition trading center” (like a wholesaler) may not execute a “segmented order” until after “a broker-dealer has exposed such order to competition at a specified limit price in a qualified auction operated by an open competition trading center.”140 The SEC defines “segmented order” under proposed Rule 600(b)(91) as an order for an NMS stock for an account of a natural person or for an account held in legal form on behalf of a natural person or group of related family members provided that “for such an account, the average daily number of trades executed in NMS stocks [is] less than 40 in each of the preceding six calendar months.”141 The definition is supposed to include orders that would ordinarily be more attractive to wholesalers (because the risk of adverse selection is low). Rule 615 would fundamentally restructure off-exchange trading in U.S. equity markets.

Much like my proposed regulation, Rule 615 is intended to solve a principal-agent problem. The commission believes that brokers have not exposed retail stock trades to the competition necessary to execute those trades at the best possible price.142 In other words, “the current isolation of individual investor orders from order-by-order competition results in suboptimal price improvement for such orders.”143 The SEC argues that there are liquidity providers (most notably, large institutional investors like mutual funds) that cannot interact with retail order flow, resulting in inferior execution quality.

In my view, Rule 615 would actually relieve wholesalers of competitive pressures. Today, brokers route to different wholesalers, assess their overall execution quality and reward wholesalers that provide the price improvement, speed, and reliability demanded by the broker. To attract more profitable order flow, wholesalers will sometimes “overpay” for less profitable order flow (in the form of better execution quality).144 In contrast, if Rule 615 is adopted, wholesalers will be entitled by law to interact with orders submitted by a broker. Most likely, wholesalers will simply interact with the orders they determine to be profitable and will ignore the orders they determine to be unprofitable (or at least execute those orders at an inferior price). It is possible that customers will receive better execution quality for certain deeply liquid stocks. Nevertheless, brokers will have much less leverage in their negotiations with wholesalers, so we should generally expect wholesalers to provide inferior execution quality for less profitable stocks and, in some cases, to refuse to execute an order entirely. Proposed Rule 615(c)(1) requires a broker routing a segmented order to a qualified auction to disclose the identity of the originating broker.145 Consequently, a wholesaler that participates in the auction will have the information necessary to estimate the risk of adverse selection, just as if the originating broker had initially routed the order to that wholesaler.

In addition, there is likely to be a negative effect on the overall amount of liquidity in the market. There are substantial “network externalities” (i.e., “network effects”) in the market-making business.146 Specifically, “the more liquid a market is, the easier it is to trade in that market—and so the more attractive that market becomes to individuals who want to trade.”147 The result is even more liquidity, which makes the market even more attractive.148 Because there are network externalities, without subsidies, market makers will not ordinarily provide the socially optimal amount of liquidity. Traditionally, to ensure that on-exchange market makers provide more liquidity, exchanges have balanced trading privileges (which encourage market makers to enter the business) with trading obligations (which ensure that market makers provide adequate liquidity when they would otherwise exit the market).149 In the off-exchange context, there is no balancing of obligations and privileges.150 Instead, brokers essentially force wholesalers not to retreat from an illiquid market, which encourages customers to participate in the market (thereby increasing liquidity). Rule 615 has no comparable mechanism to guarantee an adequate level of liquidity provision.

There is also a risk that Rule 615 will entrench incumbent wholesalers, which could widen spreads in the long run. Currently, a broker may increase competitive pressures on dominant wholesalers like Citadel and Virtu by signaling to other wholesalers that it will route more orders to them, encouraging them to make the necessary upfront investments to leverage economies of scale and to take market share. Brokers like Fidelity and Schwab consistently route some of their order flow to wholesalers other than Citadel and Virtu.151 But with order-by-order competition, all wholesalers will need to compete with Citadel and Virtu on every trade. To take market share, wholesalers will need to make massive investments in their technology without any support from brokers. As a result, the return on any investment in technology will be even more uncertain, and dominant wholesalers are likely to be further entrenched, which could, in the long run, result in inferior execution quality. In this respect, Rule 615 may be analogous to the SEC’s open access and interoperability requirements for clearinghouses, which accelerated market consolidation by allowing larger incumbents to dictate the pace of innovation and investment and by reducing the scope of possible product differentiation.152

Even if the SEC adopts Rule 615, brokers are still likely to underdisclose, such that mandatory wholesaler-specific disclosure would be necessary for customers to adequately monitor their brokers. There are some exceptions to the auction requirement, which means (i) brokers still will make non-obvious tradeoffs in routing to different wholesalers and (ii) there is still some incentive for wholesalers to compete for retail order flow. One notable exception is that wholesalers may execute the “fractional share or fractional component” of a segmented order if no qualified auction is available to execute the fractional share or fractional component.153 Note that a share can be hundreds or even thousands of dollars, so the fractional-share exception may be significant, especially since retail investors are likely to submit smaller orders. A wholesaler that receives an order also has the responsibility, when submitting an order to an auction, to set a limit price for the auction that “would inform auction responders on how to price their orders and also, if the segmented order did not receive an execution in the qualified auction, would be the price (or better) at which the wholesaler . . . subsequently could execute the segmented order as soon as reasonably possible.”154 Thus, brokers are still likely to hold wholesalers responsible (though to a much lesser extent) for price improvement, price disimprovement, speed and reliability, and with wholesaler-specific disclosure, customers could monitor the tradeoffs made by brokers in their negotiations with wholesalers.

Finally, the proposed amendments to Rule 605, while helpful, are simply not enough. The SEC has suggested that larger brokers should be subject to Rule 605, meaning that each broker would be required to report stock-specific data on execution quality.155 Proposed Rule 605(a)(1)(ii) would require entities subject to Rule 605 to disclose price improvement statistics “specifically related to the best available displayed price,” not just the NBBO, and proposed Rule 605(a)(1)(i)(F) would require entities to disclose “the cumulative number of shares of the full displayed size of the protected bid [or offer] at the time of execution,” which would allow customers to measure “size improvement” (i.e., “whether orders received an execution greater than the displayed size at the quote).156 Entities subject to Rule 605 would also be required to include smaller orders in their data, to provide more useful data on execution speed and “to produce summary execution quality statistics, in addition to the more detailed reports required by Rule 605(a)(1).”157 The proposed amendments certainly would provide valuable information. Nonetheless, most individual investors are likely to read only the summary report, and without more context, data on aggregate execution quality can be misleading, as discussed in Section IV. In contrast, with mandatory, wholesaler-specific disclosure, brokers would provide useful, high-level data while still disclosing meaningful tradeoffs in their negotiations with wholesalers. Stock-specific disclosures should supplement—not replace—wholesaler-specific disclosures.

VIII. Conclusion

There is a meaningful disclosure gap in the market for order flow. Unlike aggregate disclosures (which provide too little information) or pure stock-specific disclosures (which are likely to overwhelm individual investors), wholesaler-specific disclosure would allow customers, with very little effort, to monitor the tradeoffs made by brokers in their negotiations with wholesalers and to understand order-routing strategies. Thus, wholesaler-specific disclosure is more likely than other mandatory disclosure systems to successfully close the disclosure gap.

- 1See, e.g., Payment for Order Flow, Exchange Act Release No. 33026, 58 Fed. Reg. 52934 (proposed Oct. 13, 1993).

- 2See, e.g., Note, The Perils of Payment for Order Flow, 107 Harv. L. Rev. 1675 (1994).

- 3See, e.g., Virtu Financial, Measuring Real Execution Quality, U.S. Sec. & Exch. Comm‘n (June 10, 2021), https://perma.cc/6FZH-KZ4A (“Wholesalers provided over $3.6B in price improvement to retail investors in 2020, based on Rule 605’s calculation method; however, this method greatly understates the value provided to retail investors.”). To be sure, price improvement relative to the NBBO is an imperfect measure of savings since only displayed limit orders are included in the NBBO.

- 4See U.S. Sec. & Exch. Comm’n, Staff Report on Equity and Options Market Structure Conditions in Early 2021 (Oct. 14, 2021), https://perma.cc/2SKP-G9ER.

- 5See Gary Gensler, Chairman, Sec. & Exch. Comm’n, Market Structure and the Retail Investor, Remarks Before the Piper Sandler Global Exchange Conference ‘n (June 8, 2022), https://perma.cc/DEN2-UN9T.

- 6Id.

- 7See, e.g., Elad L. Roisman, Commissioner, Sec. & Exch. Comm’n, Enhancing Equity Market Competition (Oct. 15, 2021), https://perma.cc/KY5X-MXLQ.

- 8Order Competition Rule, Exchange Act Release No. 34-96495, 88 Fed. Reg. 128 (proposed Jan. 3, 2023) (to be codified at 17 C.F.R. pts. 240, 242); Regulation NMS: Minimum Pricing Increments, Access Fees, and Transparency of Better Priced Orders, Exchange Act Release No. 34-96494, 87 Fed. Reg. 80266 (proposed Dec. 29, 2022) (to be codified at 17 C.F.R. pt. 242); Disclosure of Order Execution Information, Exchange Act Release No. 34-96493 (Dec. 14, 2022), 88 Fed. Reg. 3786 (proposed Jan. 20, 2023) (to be codified at 17 C.F.R. pt. 242); Regulation Best Execution, Exchange Act Release No. 34-96496, 88 Fed. Reg. 5440 (proposed Jan. 27, 2023) (to be codified at 17 C.F.R. pts. 240, 242).

- 9Christopher Schwarz et al., The ‘Actual Retail Price’ of Equity Trades (September 14, 2022), https://perma.cc/3JCW-R7WP.

- 1017 C.F.R. § 242.605; 17 C.F.R. § 242.606.

- 11Frank H. Easterbrook & Daniel R. Fischel, Mandatory Disclosure and the Protection of Investors, 70 Va . L. Rev . 669, 682–85 (1984).

- 12See, e.g., Edwin Hu & Dermot Murphy, Competition for Retail Order Flow and Market Quality (June 8, 2022), https://perma.cc/NB7D-EQXX; infra Section V.

- 13Schwarz et al., supra note 9 (“Aside from general information from public disclosures, brokers have no direct information about trade execution for other brokers. In our conversations with brokers, brokers indicated they could not have predicted their relative ranking in our study.”).

- 14Order-type proliferation is itself a complicated topic. See, e.g., U.S. Dep’t of the Treasury, A Financial System That Creates Economic Opportunities: Capital Markets, (Oct. 2017), https://perma.cc/GUP3-EVQE.

- 1517 C.F.R. § 242.602 (“Every national securities exchange and national securities association shall establish and maintain procedures and mechanisms for collecting bids, offers, quotations sizes, and aggregate quotations sizes from responsible brokers or dealers who are members of such exchange or association . . . and mak[e] such bids, offers, and sizes available to vendors . . . .”); 17 C.F.R. § 242.603.

- 16See, e.g., Held NMS Stocks and Options Order Routing Public Report, Charles Schwab (July 20, 2022, 2:00 PM), https://perma.cc/7DXY-Y88Q; Held NMS Stocks and Options Order Routing Public Report, Robinhood Held Securities, LLC (July 28, 2022, 2:38 PM), https://perma.cc/5CMS-R96R; Held NMS Stocks and Options Order Routing Public Report, TD Ameritrade, Inc. (July 11, 2022, 11:09 AM), https://perma.cc/37ZS-W9WE; National Financial Services LLC, Held NMS Stocks and Options Order Routing Public Report, Fidelity (July 20, 2022, 10:10 AM), https://perma.cc/JC7T-TJJR.

- 1717 C.F.R. § 242.602; 17 C.F.R. § 242.301(b)(3)(ii) (“[If an ATS meets the conditions of 301(3)(i), s]uch alternative trading system shall provide to a national securities exchange or national securities association the prices and sizes of the orders at the highest buy price and the lowest sell price for such NMS stock, displayed to more than one person in the alternative trading system, for inclusion in the quotation data made available by the national securities exchange or national securities association to vendors pursuant to § 242.602.”); see also Kevin S. Haeberle, Discrimination Platforms, 42 J. Corp. L. 809 (2017); Hide-and-Seek: Hidden Liquidity on U.S. Exchanges, Cboe global markets, (Dec. 21, 2022), https://perma.cc/J6BV-RMRT. FINRA is the only “national securities association” in the U.S.

- 18Wholesalers sometimes enter into “order handling agreements” with brokers, but their business model requires inventory risk. See, e.g., Equities and Options Order Handling Agreement, E*Trade Financial Corporation, (November 29, 2007), https://perma.cc/78W5-7PG3; see also Stanislav Dolgopolov, Wholesaling Best Execution: How Entangled Are Off-Exchange Market Makers?, 11 Va. L. & Bus. Rev. 149 (2016).

- 19See, e.g., Order Competition Rule, 88 Fed. Reg. at 129 (“[I]ndividual investor orders are segmented because they are ‘low-cost’ flow—they impose lower adverse selection costs on liquidity providers than the unsegmented order flow routed to national securities exchanges.”).

- 20Virtu Financial, supra note 3.

- 21U.S. Market Structure: Order Routing Practices, Considerations, and Opportunities, Charles Schwab (2022), https://perma.cc/J4ST-FUNVf.

- 22Id. (“These firms heavily invest in technologies and risk management to effectively navigate and extract the fragmented liquidity that spans across public and private trading venues . . . to provide the best execution for retail orders.”).

- 23 SEC To Publish Regulation NMS for Public Comment, U.S. Sec. & Exch. Comm’n (February 24, 2004), https://perma.cc/2ZEZ-3ANE; 15 U.S.C. § 78k-1(a)(2) (“The Commission is directed . . . to use its authority under this chapter to facilitate the establishment of a national market system for securities . . . .”).

- 2417 C.F.R. § 242.611; Division of Trading and Markets, Memorandum: Rule 611 of Regulation NMS, U.S. Sec. & Exch. Comm’n (April 30, 2015), https://perma.cc/84VG-KYUP.

- 2517 C.F.R. § 242.610.

- 2617 C.F.R. § 242.612.

- 2717 C.F.R. § 242.601 (post-trade data); 17 C.F.R. § 242.602; 17 C.F.R. § 242.603; see also 17 C.F.R. § 242.614.

- 2817 C.F.R. § 242.605 (“Disclosure of Order Execution Information”); 17 C.F.R. § 242.606 (“Disclosure of Order Routing Information”).

- 29Regulation NMS, 70 Fed. Reg. 37496 (Jun. 29, 2005) (Final Rule).

- 30Division of Trading and Markets, supra note 24.

- 31Gensler, supra note 5; Roisman, supra note 7.

- 32See, e.g., Order Competition Rule, 88 Fed. Reg. at 129.

- 33Dennis M. Kelleher, Jason Grime & Andres Chovil, Securities – Democratizing Equity Markets with and without Exploitation: Robinhood, Gamestop, Hedge Funds, Gamification, High Frequency Trading, and More, 44 W. New Eng. L. Rev. 51, 75 (2022) (“Robinhood’s customers lost more than $34 million due to undisclosed costs associated with their acceptance of PFOF ‘even after’ assuming they had paid a ‘$5 per-order commission.’”); Regulation Best Execution, 88 Fed. Reg. at 5447, n.78 (noting the “inherent trade-off between payment for order flow for a retail broker-dealer and price improvement for their customers”).

- 34Payment for Order Flow, 58 Fed. Reg. 52934, 52936, 52941 (Oct. 13, 1993) (proposing Rule 11Ac1-3 (later Rule 607) and amendments to Rule 10b-10).

- 35Kelleher, supra note 33, at 102.

- 36Order Competition Rule, 88 Fed. Reg. at 129.

- 37See, e.g., David Easley, Nicholas M. Kiefer & Maureen O’Hara, Cream-Skimming or Profit-Sharing? The Curious Role of Purchased Order Flow, 51 J. Fin. 811, 812 (1996); Disclosure of Order Execution and Routing Practices, Exchange Act Release No. 43,590, 65 Fed. Reg. 75,414 (Nov. 17, 2000).

- 38Order Competition Rule, 88 Fed. Reg. at 146.

- 39See, e.g., Newton v. Merrill, Lynch, Pierce, Fenner & Smith, Inc., 135 F.3d 266, 270 (3d Cir. 1998); FINRA, Rule 5310; Regulation Best Execution, 88 Fed. Reg. at 5485 (“In situations where broker-dealer best execution-related misconduct has involved fraud, the Commission can exercise its discretion to bring best execution-based fraud charges pursuant to the Exchange Act’s or the Securities Act’s antifraud provisions.”). SLUSA generally bars class actions based on a breach of the state law duty of best execution. See Fleming v. Charles Schwab Corporation, 878 F.3d 1146 (9th Cir. 2017); Lewis v. Scottrade, Inc., 879 F.3d 850 (8th Cir. 2018).

- 40FINRA, Rule 5310(a)(1).

- 41FINRA Regulatory Notice 21-23; FINRA, Rule 5310.09(b).

- 42Sec. & Exch. Comm‘n, Final Rule: Disclosure of Order Execution and Routing Practices, SEC Release No. 34-43590 (Mar. 9, 2001), https://perma.cc/7CWT-9879; see also Office of Economic Analysis, Report on the Comparison of Order Executions Across Equity Market Structures, U.S. Sec. & Exch. Comm’n (Jan. 8, 2001), https://perma.cc/F3Y2-FRBN (“There is no single, all-encompassing measure of execution quality.”).

- 43 Apollo Global Management Inc Preference Shares Series A, Google Fin. (Jan. 20, 2023), https://perma.cc/J7HA-WAD8.

- 44Virtu and Citadel are the two largest wholesalers in the U.S.