Event Contracts Are a Step Too Far for Derivatives Regulation

This Article develops two branches of history towards understanding derivatives markets and their regulation. First, using a comprehensive database of derivatives products that the Commodity Futures Trading Commission (CFTC) has authorized, this Article traces stages in the development of derivatives products. The empirical study examines key evolutionary steps from the birth of agricultural futures in the second half of the 1800s to where traders now bet on how long Taylor Swift’s most recent album dominates the Billboard 200, whether the President will pardon specific individuals, or how many times Bill Ackman (a notable hedge fund manager) accuses MIT professors of plagiarism. Second, the Article examines the statutory goals of the primary source of derivatives regulation: the Commodity Exchange Act (CEA). From their enunciation in the Grain Futures Act of 1922 to their most recent amendment under the Commodity Futures Modernization Act of 2000, these goals have consistently viewed derivatives as a means to benefiting Main Street rather than an ends in themselves. Specifically, the twin goals of the CEA are enabling hedging and price discovery in the “cash” markets underlying derivatives instruments. This Article argues that these goals may also serve as a limiting principle, enabling the CFTC to conclude that an instrument that fails to advance either goal is beyond the reach of the CEA. The jurisdictional boundary is significant because products the CFTC authorizes fall into the CFTC’s exclusive jurisdiction, preempting state law and displacing other federal regulation. This Article concludes that the CFTC has authority to require exchanges it regulates to delist a range of contracts (referred to as “event contracts” or “prediction products”) that fail to adequately serve the public interests motivating the CEA, instead shifting them to regulation under state law including state law restrictions on gambling. This approach is a powerful alternative to the strategy the CFTC has pursued in court to prevent exchanges from listing event contracts that settle on the basis of election outcomes and a narrow set of other socially sensitive activities.

I. Introduction

In the U.S., derivatives trading began when the Chicago Board of Trade (CBOT) developed a market in grain futures contracts soon after the Civil War.1 These contracts (i.e., futures) required one party to buy a specified amount of a grade of wheat at a specified time and location and the other party to sell that wheat, at the specified time and location.2 Since their inception, futures did not exist for their own sake but instead to assist activities in so called “cash” or “spot” markets, i.e., business activities involving assets referenced in the futures contract.3

For example, a farmer could go “short” through the futures contract (i.e., sell the grain under the contract) to neutralize her risk that grain prices fluctuate. Through selling wheat under the futures contract, the farmer effectively sells at a price fixed at the time of execution with settlement taking place in the future through an exchange of the referenced commodity for cash. If prices for wheat increase, the farmer will (i) lose money under the futures contract because the price of wheat at the time of delivery under the futures contract exceeds what she sold it for, but (ii) experience increased revenues from the harvest. If, on the other hand, prices fall, the farmer will (i) profit under the futures contract, and (b) suffer offsetting losses as she sells her harvest at the lower price. A bakery can similarly use grain futures to guard against price fluctuations. The bakery would go “long” through the futures contract (i.e., buy the grain). This would mean that if wheat prices decline, the bakery loses under the futures contract but is able to procure its ingredients at a lower cost. And reciprocally, if grain prices increase, the value of the bakery’s futures position increases although its procurement costs rise. These examples of a farmer and baker using a futures contract are quintessential examples of hedging, i.e., risk management. Trade in futures contracts also generates prices (i.e., how much do parties in the futures market demand to take a long or short position). Cash markets reference the prices established in futures markets in lieu of developing pricing independently. As reviewed in more detail in Part II, derivatives are not viewed as an end in themselves. Instead, the regulation of derivatives is based on their historical contributions to hedging and pricing in cash markets.4

This Article argues that the development of derivatives products has become unmoored from these twin statutory goals. The source of federal derivatives regulation is the Commodity Exchange Act (CEA).5 The federal regulator of derivatives markets is the Commodity Futures Trading Commission (CFTC).6 Among its various roles under the CEA, the CFTC authorizes the derivatives products that exchanges make available to market participants.7 The CFTC also provides a database of all products it has authorized since its birth in 1974.8 Through a review of futures contracts the CFTC has authorized, this Article traces a step-by-step drift in the design and function of permitted derivatives instruments.9 As described in Part III, the individual steps generally appear justifiable as they sacrifice fidelity to the twin goals to address new forms of risk or serve new clienteles10 —but in the aggregate, these steps trace a gross departure from the underpinnings of derivatives regulation.11

The cumulative drift in derivatives products has led to the authorization of contracts this Article refers to as “event contracts.” While the term “event contract” is not defined in the CEA or CFTC regulations, event contracts are generally understood to be contracts referencing the occurrence of an event where the payoff structure is binary, i.e., either the specified event occurs and a payment is made, or the event does not occur and no payment is made.12 As distinct from traditional futures and other derivatives, cash flows under event contracts do not track changes in prices of a referenced asset. As developed in Part III.C, prices for event contracts come to reflect expectations as to the event’s likelihood, which is why these products are sometimes referred to as “prediction products.”

Referenced events have been varied and range from the serious to the more trivial. They have included macroeconomic variables reaching a value (e.g., the unemployment rate reaching five percent) or a certain number of hurricanes making landfall in the U.S, as well as whether Taylor Swift’s most recent album spends a specified period at the top of the Billboard 200 or whether Bill Ackman accuses a certain number of MIT professors of plagiarism by a certain date.13 The CFTC has authorized all of the foregoing products and thousands more as exchanges have exploited automation and standardized commercial practice to cheaply launch new event contracts.14 In authorizing these products, the CFTC provides them with preemption from state law and enlarges its own jurisdiction. This results from a statutory provision that grants the CFTC exclusive jurisdiction over any products listed on CFTC-governed exchanges.15 As a result, the CFTC has amassed regulatory power and responsibilities while, among other things, (a) suspending protections market participants would receive under state gambling regulation and (b) expanding its enforcement jurisdiction to contexts in which it has little experience or expertise such as administration of the Emmys and other awards shows.16

Recently, however, the CFTC has found itself struggling to prevent the listing of event contracts. Relying on a narrow authorization it obtained under the Dodd-Frank Wall Street Reform and Consumer Protection Act to prevent the listing of certain contracts involving “(I) activity that is unlawful under any Federal or State law; (II) terrorism; (III) assassination; (IV) war; [or] (V) gaming”17 , the CFTC has rejected event contracts that settle on election outcomes such as which political party will control the Senate or the House after the November 2024 election.18 The CFTC’s theory is that event contracts that pay on the basis of election outcomes represent both gaming and activity unlawful under State law, as many states make betting on elections illegal. However, Kalshi—the exchange seeking to list these contracts—challenged the CFTC in court and won approval to list these contracts.19 Subsequently, Kalshi and Interactive Brokers hosted trading in event contracts that settled based on various outcomes in the upcoming 2024 election.20 These included politically relevant contracts with more attenuated connection to the balance of power between the two parties, such as which presidential candidate would win the popular vote (as distinct from the electoral college), which presidential candidate would win in Pennsylvania (and other swing states), and even whether President Biden would pardon his son, Hunter Biden.21 Not only does betting on elections raise serious questions as to election integrity and perceptions thereof, the listing of these instruments on CFTC regulated exchanges makes the CFTC responsible for policing election integrity as the CFTC holds enforcement authority to assure markets it regulates are free from fraud, manipulation and other abuse. The expansion of the CFTC’s purview to elections as well as other areas implicated by event contracts’ terms can detract from the agency’s technocratic character and core strengths.22

This Article proposes an alternative strategy for the CFTC to take with respect to event contracts—a strategy that goes back to the first principles of the CEA. The CFTC should review listed derivatives products—and event contracts in particular—to identify those that have scant utility for hedging and pricing in cash markets. These products should be delisted, and instead regulated under state law. To reach this result, the CFTC can apply its interpretive discretion to determine that the statutory purpose enunciated in Section 3 of the CEA serves as a limiting principle on the products that it may authorize.23

This Article proceeds as follows. Part II provides a novel perspective on the history of U.S. derivatives regulation. After introducing futures and their pre-regulatory history, Part II identifies the twin goals driving derivatives regulation since its birth. Part II also explains the role of the CFTC, and how the CFTC is able to displace state regulation of listed products. Part III then presents the results of a review of derivatives product development that led to event contracts becoming authorized. This novel empirical inquiry reveals the gradual expansion of the universe of listed products, marked by specific innovations in contract design. The evolution is additive, with ingenuity adapting and expanding prior innovations while responding to commercial challenges and new market demands.24 Part III traces evolution in product offerings to the contemporary availability of event contracts to a retail clientele. Part IV applies the legal background developed in Part II to the evolution of instruments described in Part III. Part IV argues for prohibiting a range of products from CFTC-regulated exchanges. A range of the contracts reviewed in Part III likely fail to sufficiently advance either the hedging or pricing goals that Section 3 of the CEA asserts transactions subject to the Act advance. The CFTC may and should mandate such products be delisted. Part IV considers and dispenses with legal and policy arguments for making these products available through CFTC-regulated exchanges. This approach allows the CFTC to maintain its focus on core derivatives markets, and avoid wading into areas where it has limited expertise and its technocratic authority may be undermined. Part IV also recommends language for a statutory amendment in case the interpretive position advocated in this Article is not compelling from a legal standpoint. The conclusion discusses how the CFTC could operationalize the limiting principle on its jurisdiction in reviewing current and future derivatives products.

II. A Brief History of U.S. Derivatives Regulation

The origins of U.S. derivatives markets and their regulation are in agriculture. From its outset, derivatives regulation struggled to draw a boundary between gambling and justifiable speculation in the context of financial transactions.

A. The Birth of Futures Trading in the United States

The Chicago Board of Trade (CBOT) was established in 1848. Initially, it served as a wholesale market for grain. CBOT’s charter permitted it to set rules for membership, and these rules permitted members to trade on their own behalf as well as on behalf of customers while mandating certain practices meant to facilitate trading. Within a few decades, CBOT developed sophisticated trading and risk management processes based on self-regulation under its Illinois charter. Among other things, CBOT introduced standardized contracts that required the delivery of grain of a certain grade at a certain location one or more months in the future at a price established at the time of execution. In this manner, CBOT transitioned from being a “cash” or “spot” market where execution and settlement were largely contemporaneous to being a derivatives market where traders could take positions based on future prices of grain and transfer the risk of price fluctuation.25

These standardized contracts came to be called “futures,” as distinct from the tailored bilateral agreements for future delivery of an asset referred to as “forwards.” Forwards preexisted futures and continue to be used across various assets. And forwards differ from futures not only in their bespoke terms, but also in their idiosyncratic credit quality.

In 1883, CBOT developed a “clearing” mechanism,26 which other futures exchanges came to emulate. Clearing practices have evolved over time. Pursuant to contemporary clearing, exchange members entering into a futures transaction effectively split the transaction into two—one between the first member and a clearinghouse and a second between the clearinghouse and the second member. The clearinghouse is typically an affiliate of the exchange. The clearinghouse acts as guarantor of both transactions, standing in between the parties and standardizing credit risk similarly to how the delivery terms of the future standardize market risk (i.e., risk related to the price of the referenced asset).27 The standardization of futures contracts is an important function of market intermediaries, and explains unique dynamics within these multitrillion-dollar markets.28

Because futures contracts are standardized, a contract to buy a certain amount of grain at a certain location upon a certain date can be offset through entering a contract to sell the same grain at the same location and on the same date. This enables financial settlement of contracts through the purchase of inverse contracts, notwithstanding that on its face, a contract may require settlement through physical delivery.29

Three common properties help explain how futures function. First, the “value” of a position established through a futures contract changes over the lifetime of the contract. For example, a future to buy (or sell) 1,000 bushels of hard red winter wheat on a particular date at a particular grain depot will change price as the expected price of the wheat at delivery changes. If, for example, the expected price goes up by one dollar per bushel, the contract price should increase by $1,000. This represents a $1,000 gain to prior purchasers of grain delivery under the contract and a $1,000 loss to prior sellers. Pursuant to margin requirements, the seller in the preceding example would have to post $1,000 in additional collateral upon the change in expected price; this collateral (also called variation margin) helps assure performance and acts as a quasi-real time settlement mechanism against expectations.30 By design, as the settlement date approaches, the price of the futures contract should converge to the cash market price of wheat.

A second, related, quality is the relationship between futures prices and cash market prices in a “competitive” market. Arbitrage opportunities limit deviation of prices between futures and cash markets. To illustrate, assume that the market price of an obligation to deliver 1,000 bushels of hard red winter wheat on December 31 at a particular depot is $6,000. In other words, a futures contract to sell that wheat provides $6,000 to the seller. If the costs of obtaining the wheat, storing it until December 31, and then making delivery at the specified location are substantially below $6,000, it is sensible to procure, store and then transport that wheat while entering into futures contracts to sell that wheat. The various costs of obtaining an asset and making delivery in a manner that would satisfy the terms of the futures contract provide a ceiling on the price of a futures contract, and a linkage between cash and futures markets.31

Third, futures contracts generally imply “basis risk” for their commercial users. For example, if a grain exporter has an obligation to deliver 1,000 bushels of hard red winter wheat in six months at then prevailing market prices, the exporter faces a risk. First, she does not have the grain and needs to procure it. Second, if the price of grain declines after procurement and before the export, the decrease will be a loss to the exporter. To address these circumstances, the exporter may enter into two transactions. First, the exporter enters into a forward purchase agreement for the 1,000 bushels of wheat at a fixed price six months ahead of the export obligation. Second, the exporter hedges against price declines through selling futures contracts on 1,000 bushels to be settled in six months’ time. Pursuant to the combination of the forward and future position: (1) if prices for wheat increase, the exporter will gain based on the differential between the price of the exported grain and the price at which that grain was procured, while losing money on the futures contract; and (2) if prices for wheat decline, the exporter will lose based on the differential between the price at which the grain was procured and the lower price at which it will be exported, while profiting on the futures position. Notably, (1) and (2) only state that the performance of the futures position dampens the gain (or loss) on the commercial transactions (i.e., the combination of procurement and export). The claim is not that the futures position eliminates the risk from commercial operations. That is because of “basis risk”, which refers to risk that prices of the commodity underlying the futures transaction develop differently from prices of the commodity underlying the commercial transactions.

There are many potential sources of basis risk: for example, the wheat deliverable under the futures may be of a different quality than the wheat the exporter must ship; or the location of delivery under the futures contract is significantly different from the location where the exporter must deliver the wheat to its customer and this difference entails greater transportation costs; or the delivery deadline for the future and the forward differ. These types of slippage in pricing between the commodity in its commercial settings and the commodity as it satisfies futures contract delivery requirements mean that hedging through futures addresses risk to a degree, and that degree can vary. In this respect, asking whether a product serves a hedging purpose is somewhat like asking whether a relationship is romantic. Some relationships are clearly romantic, others clearly are not, and then there are some that are more romantic than others and some that are barely romantic or not romantic enough. This difficult assessment is revisited in Part IV, which recommends delisting products with inadequate hedging utility.

B. Telegraphs Forced a Difficult Distinction Between Futures Trading and Gambling

The derivatives business changed profoundly after the introduction of telegraphs. The commercial opportunities this technology unleashed threatened the exchanges and prompted the initial contact between derivatives markets and federal lawmaking. Telegraphs enabled bucket shops to compete with exchanges, undercutting exchange liquidity and undermining confidence in financial markets.

Before the days of computing, exchanges functioned through individuals communicating orders to buy and sell in designated locations.32 These humans were members of the relevant exchange or traders working for members organized as entities. Traders were not necessarily submitting orders for the member, but instead could submit orders for customers. With the advent of telegraphs, brokers could quickly serve customers in distant locations. But technology also allowed the prices established on an exchange to be broadly, swiftly disseminated over ticker tape. Major exchanges exhibited prices, which were updated as orders came in and were matched. This price information was disseminated from exchanges to distant exchange-member offices, from where it could (and sometimes was) disseminated further including to unauthorized third parties.33

Bucket shops obtained price information from brokers and others with access. Bucket shops would then display current price information to their customers. When a customer placed an order with a bucket shop, the order would represent a contract with the bucket shop. It was not routed to the exchange. Instead, a zero sum was created between the customer and the bucket shop, which took the other side of the position. Bucket shops tended to charge lower prices than brokers, so their services were a competitive substitute for placing an order through a broker. However, the relationship between shop and customer, as well as the character of many bucket shop owners, led to predatory dynamics. When a customer failed to meet margin requirements over the lifetime of a trade, the customer would lose her position (including all transaction fees). Bucket shops manipulated price information. For example, bucket shops placed sell orders on exchanges to settle at lower prices with customers. The same practice of placing strategic exchange orders to manipulate the bucket shop’s own pricing stream was used to create margin calls towards triggering customer defaults. Perhaps more importantly, a number of bucket shops were fly-by-night operations that took customer fees for a while and then—when the market turned against the bucket shop—absconded.34

Brokers working with exchange members, in contrast, were not subject to the same conflicts of interest or default risk, as they did not assume proprietary positions. Many customers probably did not appreciate the difference between submitting orders to a brokerage to establish a position through an organized exchange and submitting the same order to a bucket shop.35 All they saw was that the bucket shop charged lower fees, while wearing the dress of a brokerage and nominally putting the customer in the same position.

The difference between orders placed with a broker and orders placed with a bucket shop, however, was critical. Brokered orders led to transactions matched through the facilities of an exchange. That transaction would be with a third party and subject to bilateral margining, which decreased the risk of default. Brokered orders also necessarily added to the liquidity of an exchange. Understandably, exchanges such as the Chicago Board of Trade and the New York Stock Exchange campaigned against bucket shops and sought to prevent the flow of price data to them.36 The exchanges were concerned about the free riding, the reputational damage to their ecosystem, the loss of fees and the loss of liquidity.37 Initially, the exchanges brought cases in state courts. However, for decades, the exchanges consistently lost.38 Courts saw both the exchanges and the bucket shops as engaged in illegal gambling and would not protect data related to this illicit activity.

The crux of the gambling argument derived from a principle under state law, which looked to whether parties entered into the contract with intent to deliver.39 Under this principle, if a transaction in property was entered into with intent to transfer the property, it was not gambling. In contrast, if the contract was entered into with intent to settle it financially based on how the value of the property changed in the future, the parties were engaged in illegal gambling.40 The doctrine included an important exception that accounted for changes in circumstances. In this case, by the time of settlement, the intentions of the parties may have evolved so that instead of completing physical delivery, the parties resolve their obligations through a financial settlement.41 Anti-gambling prohibitions permitted enforcement in such contexts, again, focusing on the intent of the parties at the time the contract was executed.

Anti-gambling statutes captured intuitions distinguishing speculation from commercial arrangements in the context of ordinary, bilateral transactions. These intuitions did not coherently map onto the futures context where contracts both (a) required physical delivery, and (b) were overwhelmingly resolved through payment for offsetting transactions rather than physical delivery. Focusing on the economic substance as distinct from form, state courts repeatedly applied anti-gambling law to protect customers from futures-brokers’ attempts at collection. The same laws were used by bucket shops to argue that because futures predominantly settled financially rather than through physical delivery, futures exchanges were illegal gambling organizations ineligible for legal protections with respect to the subject of their operations.

Ultimately, the exchanges brought their case to the Supreme Court in a case that pitted CBOT against a large bucket shop, Christie Grain & Stock Co. Board of Trade v. Christie Grain & Stock Co., 198 U. S. 236 (1905), distinguished between gambling and futures trading, holding the latter was permissible under state law and thus eligible for protection under contract law. In writing for the majority, Justice Holmes asserted without any principled basis that financial settlement and settlement through offsetting transactions were distinct and the latter did not violate Illinois state anti-gambling law.42 This was a formalist argument that focused on the language of contracts rather than the course of financial performance. Although Justice Holmes was unable to find logic to support the outcome, his opinion expressed sophisticated intuitions for distinguishing futures trading from gambling.43 Read charitably, his distinction rested on the context of contracting rather than the content or performance of specific contracts. Holmes made three observations that are excerpted below and returned to subsequently, which are fundamental to justifying and defining the extent of regulated derivatives markets.

(1) Utility of Hedging to Commercial Market Participants: “There is no doubt that a large part of [futures contracts are] made for serious business purposes. Hedging, for instance, as it is called, is a means by which collectors and exporters of grain or other products, and manufacturers who make contracts in advance for the sale of their goods, secure themselves against the fluctuations of the market by counter contracts for the purchase or sale, as the case may be, of an equal quantity of the product, or of the material of manufacture. It is none the less a serious business contract for a legitimate and useful purpose that it may be offset before the time of delivery in case delivery should not be needed or desired.”44

(2) Use of Prices from Futures Markets in Commercial Dealings: “[T]he quotation of prices from the [futures] market are of the utmost importance to the business world, and not least, to the farmers; so important, indeed, that it is argued here and has been held in Illinois that the quotations are clothed with a public use.”45

(3) Speculation and Price Formation: “[I]n a modern market, contracts are not confined to sales for immediate delivery. People will endeavor to forecast the future, and to make agreements according to their prophecy. Speculation of this kind by competent men is the self-adjustment of society to the probable. Its value is well known as a means of avoiding or mitigating catastrophes, equalizing prices and providing for periods of want. It is true that the success of the strong induces imitation by the weak, and that incompetent persons bring themselves to ruin by undertaking to speculate in their turn.”46

In distinguishing futures trading from gambling and the CBOT from a bucket shop, Board of Trade v. Christie Grain & Stock Co. enabled the contemporary ecosystem of standardized derivatives trading. Bucket shops were parasitic in this ecosystem and endangered exchange operation. First, bucket shops could not operate without exchange sourced data, but the reverse was untrue. Second, if bucket shops drew sufficient transactional volumes from exchanges, the latter would lose the liquidity that attracted traders and justified membership. Without liquidity (i.e., orders to buy and sell futures), an exchange like the CBOT would lose its raison d’être and no longer be able to justify the costs of membership or support its operations. As a result, if bucket shops could divert trading from exchanges, they endangered both the exchanges and the price information they used to attract customers and operate their own business. Furthermore, confusion among customers between legitimate brokers and bucket shops combined with malfeasance on the part of the latter contributed to deterioration in overall trust. In a classic tragedy-of-the-commons,47 however, individual bucket shops had no incentive to limit how much they undermined the exchanges through diverting order flow or, more generally, subverting trust. The Supreme Court and then Congress came to protect futures exchanges from parasitic competition from bucket shops.

C. Federal Regulation of Derivatives

The Grain Futures Act of 1922 (GFA) initiated federal derivatives regulation.48 The GFA established the paradigm for federal regulation of derivatives markets, which continues through the present day. That paradigm focuses on regulating market intermediaries, rather than the end-users of financial products. Under the GFA, contract markets (i.e., exchanges) applied to the Department of Agriculture for designation. Unless a contract market was designated, the GFA made it illegal to trade futures on the contract market.49 To qualify for designation, a contract market had to meet various criteria related to the quality of its grain delivery facilities, the volume of deliveries, and its regulation of members.50 An exchange had to prohibit its members from making or disseminating misleading reports about grain as well as engaging in corners and other manipulation. Additionally, an exchange had to require its members to follow reporting and recordkeeping requirements that the Secretary of Agriculture developed.51 Although the GFA primarily assigned administration of the Act to the Department of Agriculture, it also reserved roles for the Attorney General and Secretary of Commerce who together with the Secretary of Agriculture composed “the commission”. The commission reviewed suspensions and revocations of contract market designation as well as rejections of contract markets’ applications for designation. As a leading scholar of derivatives regulation, Jerry Markham, explains:

The GFA limited futures trading to ‘contract markets’ licensed by the federal government, thereby establishing the exchange trading floor’s exclusivity over trading in futures contracts for decades to come. Like most congressional actions, the limitation of trading to [designated] ‘contract markets’ was a balance of interests, promoting the dissemination of price information, expanding the regulation and monitoring of the marketplace, and eliminating bucket shops.52

The GFA regulated futures trading on “wheat, corn, oats, barley, rye, flax, and sorghum.” Futures on commodities that were not referenced in the statute—such as silver—remained outside of federal regulation until the Commodity Futures Trading Commission Act of 1974, which is discussed below. In the interim, Congress occasionally expanded the scope of commodities triggering federal regulation.53

Following the initial raft of New Deal legislation, the Commodity Exchange Act (CEA) was enacted in 1936.54 The CEA substantially expanded the regulation of derivatives markets, including through (a) requiring the registration of exchange members and floor brokers, (b) imposing a variety of requirements intended to protect customers directly on exchange members (e.g., prohibitions on members defrauding their customers and requirements that members segregate customer funds from proprietary assets).55 The CEA also addressed widespread concerns about speculation and manipulation causing artificial prices through delegating to the “Commodity Exchange Commission”56 the power to set position limits.57 Position limits restrict the size of positions traders can take through futures transactions, with an important exception for bona fide hedging transactions.58 This was the first obligation to apply to end-users in derivatives markets as distinct from intermediaries.

The CEA remains the source of federal derivatives regulation and followed the birth of federal securities regulation under the Securities Act of 1933 and the Securities Exchange Act of 1934. Whereas the latter created the Securities Exchange Commission as a standalone agency to regulate securities markets, the CEA continued to rely primarily on the Department of Agriculture to regulate derivatives markets.59 It was only the CFTC Act of 1974 that created an independent agency modeled on the SEC to regulate derivatives markets.60

The birth of the CFTC coincided with the expansion and firming of derivatives regulation. It was the CFTC Act that expanded the scope of regulated derivatives beyond agricultural products to all products listed on designated contract markets.61 This was done through a terse, complex and powerful revision to the term “commodity.” That term defines the ambit of the CEA. The CFTC Act expanded the term to include “all services, rights, and interests in which [futures] are presently or in the future dealt in.”62 As a result of this amendment, any subject of a futures contract became a commodity, allowing CFTC jurisdiction to expand as derivatives exchanges developed new contracts.63 This elegant but not unproblematic drafting put markets in the driver’s seat, while giving the CFTC veto powers through the contract authorization process. This expansion was especially powerful because the CFTC Act also gave the CFTC exclusive jurisdiction over exchange traded contracts.64 As a result, product approval both expanded CFTC jurisdiction and displaced state regulation.65 As discussed below, this would become important as exchange proposals for products strayed further from the roots of the CEA and implicated the gambling concerns traditionally addressed through state law.66

Part III below traces the evolution of products traded on CFTC-regulated exchanges. Given the evolution of products and the consequences of a product being listed on a derivatives exchange—for expansion of CFTC jurisdiction and preemption of other regulation—a natural question is whether there are statutory bounds on the products the CEA governs. Section 3 of the CEA addresses this question in specifying the transactions that are subject to regulation. Section 3 predates the CEA, being present in the original Grain Futures Act. That section specifies that futures contracts, as Holmes had observed almost twenty years earlier, were used both for hedging and for setting prices in grain cash markets. According to the GFA, these two uses imbued futures with a cognizable public interest and enabled their federal regulation under the Commerce Clause.67 The Commodity Exchange Act retained this language. In fact, this language did not change until 1983 when Congress enacted the Futures Trading Act (FTA) of 1982.68 The FTA’s revisions to Section 3 caught up with the 1974 expansion of CEA authority beyond agricultural commodities through replacing references to “grain” in the description of the Act’s purpose with references to “commodities.”69 Then, almost eight decades after Section 3(a) was adopted, it was substantially shortened under the Commodity Futures Modernization Act (CFMA) of 2000 to read as follows:

The transactions subject to this Act are entered into regularly in interstate and international commerce and are affected with a national public interest by providing a means for managing and assuming price risks, discovering prices, or disseminating pricing information through trading in liquid, fair and financially secure trading facilities.

These changes replaced longer and more concrete explanations of the public interest implicated in derivatives transactions with an abstract summary. Nevertheless, the purpose of the CEA continues to be linked to the utility of derivatives for hedging (i.e., “managing and assuming price risks”) and discovering and disseminating pricing in cash markets as Justice Holmes had intuited almost a century earlier. In identifying the purpose of the CEA, Section 3(a) also provides a basis for a principled limit on the CEA’s authority over financial products. Products that lack the functions identified in Section 3(a) can fall to other regulators. Part IV below will return to Section 3(a) in discussing whether CFTC-regulated exchanges should have authority to list various products that lack hedging and price setting functions. As discussed there, the CFTC may interpret Section 3 in accordance with its original intent as simultaneously justifying and circumscribing federal derivatives regulation. But before engaging in this analysis, Part III follows the evolution of derivatives products to where they have ceased to appreciably serve either of these twin purposes.

III. The Evolution of Futures Contracts

Prior to the CFTC Act of 1974, federal derivatives regulation governed exclusively agricultural derivatives. With the CFTC’s founding, the range of federally governed derivatives vastly expanded, coming to encompass futures on metals and a variety of other exchange-traded products. This era is referred to as the financialization of derivatives, as the variables driving cash flows under derivatives instruments came to include intangibles such as currencies and interest rates. The CFTC provides a database listing products it has authorized since its inception.70 Through reviewing this database—including the contracts that were already being traded on designated exchanges as of the time of the CFTC’s formation—this Part III chronicles the gradual unmooring of regulated derivatives from the hedging and price discovery justifications of the CEA.71

A. The Development of Currency and Interest Rate Futures and the Dawn of Financial Futures

The first futures contract designed to manage risk related to an intangible asset was the foreign currency future. The New York Produce Exchange (NYPE) was founded in 1862 and had been a successful commodity exchange in the late 1800s and early 1900s. By the middle of the 1900s, however, the NYPE encountered scandal and began to struggle.72 The exchange then pivoted, seeking to reinvent itself. It developed a stunning proposal to list first futures on currencies and then futures on stock.73 In April 1970, the NYPE launched the International Commercial Exchange, which began trading in currency futures.74 By 1973 the NYPE closed, and its International Commercial Exchange futures market would come to fail.75 Instead, it was the Chicago Mercantile Exchange (CME) that would come to develop the first deep markets in currency futures.

In December 1971, the CME created an affiliate—the International Monetary Market (IMM)—to list financial futures. On May 16, 1972, the IMM launched seven currency futures contracts.76 The timing was important. On August 15, 1971, shortly before the birth of IMM and its introduction of a suite of currency futures, President Nixon abandoned the gold standard.77 This initially devalued the dollar and permanently unmoored foreign exchange rates. The result was that market participants with international operations faced less predictable cash flows.78 Figure III.A illustrates the increased volatility through showing the cost of British Pounds Sterling in U.S. dollars over the relevant timeframe.

Figure III.A: Cost of £ in U.S. dollars79

The IMM launched currency futures with an eye to serving a substantial market. At the time, there was an established interbank forward market for hedging currency exchange risk.80 However, that interbank market had restrictions on eligible participants. Most firms that recognized revenues in one currency but had expenses in another could not directly access the market, and many smaller businesses faced high costs or difficulties in accessing the interbank market. The CME served these clients, allowing them to buy contracts that locked-in the future price of foreign currency. While the exchange that invented futures to manage foreign exchange risk failed, the CME’s suite of products succeeded and was soon emulated by other major exchanges.81

CBOT and CME—the two successful Chicago-based futures exchanges that trace their roots to the 1800s—would continue to compete and shape U.S. derivatives markets for decades until their merger in the early 2000s.82 It was these two exchanges that took the next step in the evolution of risk transfer markets. Along with significant increases in currency exchange rate volatility, the 1970s saw sustained interest rate volatility.83 Figure III.B shows short term interest rates throughout the 1900s, reflecting growth of interest rate risk.

Figure III.B: U.S. short term interest rates84

The first derivative enabling hedging of interest rate risk was the futures contract on U.S. Government National Mortgage Association (GNMA) pass through certificates, which the CBOT began trading on October 1975.85 The GNMA pass through certificate represents an interest in a securitization of mortgages.86 Those mortgages produce cash as homeowners make principal and interest payments. Those payments are guaranteed by the GNMA, which effectively has the backing of the U.S. government and thus is not subject to default risk.87 As a result of the federal government’s backing, the holder of a GNMA certificate is subject only to the risk that the value of cash flows the certificate produces changes in real terms. This is synonymous with interest rate risk, i.e., changes in the cost of funds over time.

The insight behind the first interest rate future exploits the financial relationship between interest rates and the price of debt instruments such as loans, bonds and notes. For example, as interest rates rise, the value of a GNMA certificate declines because identical cash flows to those due on the certificate can be obtained through a smaller extension of principal.88 As background, GNMA certificate futures, like the initial currency futures, were physically settled. Although their underlying asset was financial as distinct from tangible, these futures adopted settlement mechanics from agricultural and other tangible commodity futures markets established about a century prior. When an IMM currency futures settled, dollars would be delivered in exchange for the contractually defined amount of foreign currency. Similarly, when the GNMA future settled, dollars would be delivered in exchange for the contractually specified GNMA certificate representing $100,000 in principal on mortgages paying an effective annual interest rate of eight percent.89 By design, the difference in price between a GNMA certificate at the time of execution and its price at the time of settlement expressed interim changes in risk-free interest rates.90 Each basis point decrease (increase) in interest rates led to a constant increment (decrement) in the price of the deliverable certificate. GNMA futures proved to be successful and the market expanded rapidly.91 By July 1979, open contracts were outstanding for more than $7 billion face value of GNMAs.92

A variety of interest rate hedging futures arrived on the scene by the early 1980s, although experts expected relatively few to attract sufficient liquidity and survive.93 CME and CBOT followed up on the GNMA contract through introducing futures linked to other U.S. risk-free interest rates based on short, medium, and long-term U.S. government debt.94 Exchanges also worked on developing products that tracked private market interest rates (i.e., interest rates charged to non-governmental borrowers).95 These included two distinct CBOT futures on commercial paper that were approved in July 1977 and September 1978 and went on to fail,96 as well as futures on domestic bank certificates of deposit that were first proposed by the New York Futures Exchange and shortly thereafter by CBOT and CME.97

Probably the most important evolution within interest rate futures following the GNMA contract was the design of the so called “Eurodollar” futures contract. Eurodollar futures were approved for the CME and soon thereafter for CBOT and the New York Futures Exchange in early to mid-December 1981.98 The asset referenced in these futures contracts was a Eurodollar deposit collecting interest at the London Interbank Overnight Rate (LIBOR). As background, these deposits became popular after deposits within the U.S. became subject to reserve requirements, expensive FDIC assessments and interest rate caps.99 Eurodollar deposits (e.g., a deposit of dollars at a U.S. bank’s European location by a multinational corporate client) were used to skirt these restrictions and collect higher interest rates than were available in the U.S. Partly, these interest rates compensated for the deposit accounts being ineligible for support from FDIC insurance or the Federal Reserve.100

Like other interest rate futures, Eurodollar futures were designed so the long position lost value as interest rates increased (and reciprocally, rose in value as rates dropped) with a fixed increment (and decrement) per basis point change in the referenced rate. Unlike all prior futures however (including all CFTC-regulated interest rate products), Eurodollar futures were cash settled. There was no deposit account outside of the U.S. that would be delivered to the futures purchaser (i.e., long position) at settlement. Instead, the difference between the value of a hypothetical account at the time of execution and the time of settlement was used to calculate an amount of cash the purchaser would receive if LIBOR dropped in the interim or pay if LIBOR rose. This dispensed with Holmes’s fictive distinction101 of futures contracts from illegal gambling instruments. And the distinction was no longer necessary because futures contracts traded on CFTC-regulated exchanges were protected through preemption of state law, which as discussed above was expressly provided for under the CFTC Act of 1974. With the CFTC’s approval of Eurodollar futures, precedent was set for a more attenuated link between futures and cash markets.

Eurodollar futures had another feature that would be influential in product development. These contracts settled on the basis of an index rather than a concretely observed price. Adriana Robertson defines an index as “an aggregation of different pieces of information into a single number based on some algorithm.”102 LIBOR, as an index, was calculated through soliciting banks for the rates they would hypothetically charge to loan funds, and then pruning outliers.103 Through collecting quotes for hypothetical loans in the London interbank funds market, the index expressed the cost of unsecured funds to major banks.104 This served as a reference point to other private borrowers, who could generally expect a similar or higher rate depending on how their default risk compared to that of major banks.105

B. Stock and Other Index Futures

A few months after approving Eurodollar futures, the CFTC approved the first futures based on an equity index. Their story is similar to the birth story of currency futures related above. The Kansas City Board of Trade (KBOT) operated since 1856 and was known for agricultural commodities, and in particular, futures on the relatively nutritious hard red winter wheat.106 In February 1982, the CFTC approved an application from KBOT to list stock index futures that referenced the Value Line Index. The Value Line Index represents the combined value of stock from approximately 1,681 public companies. Nowadays, relatively few mutual funds, exchange traded funds, or other financial products track the Value Line Index.

While futures on the Value Line Index floundered, futures settling on equity indices multiplied and became a substantial portion of derivatives markets.107 The CME obtained approval for futures on the S&P500 two months after KBOT’s approval. Like prior futures contracts, the Value Line futures from KBOT and the S&P500 futures from CME were designed to enable hedging.108 Various financial market participants (e.g., investors, dealers) had portfolios of stocks, which short positions on an index composed in significant part of those stocks could hedge.

Since then, a variety of equity indexes have been developed covering various sectors (e.g., energy, aerospace, healthcare), geographies (e.g., East Asia, Europe, Emerging Markets) as well as broad composites of public equities listed in the U.S. (e.g., NASDAQ 100, Russel 2000 and 3000). To enable more participation and fine tuning, mini- and micro- contracts have been developed that allow purchase of futures with smaller exposure.109 All of the equity indexes have in common that their values are aggregates of public companies’ share prices. The construction of indices varies, however; for example, some indices give equal weight to all shares in the index while others apply a market weighting so that companies with relatively more shares outstanding have higher representation in the index.

Equity index futures are cash settled. Delivery of a basket of stock is operationally costly and may require fractions of shares. Instead of requiring physical settlement, the Value Line futures and subsequent equity index futures applied the cash settlement mechanics developed for Eurodollar futures.110 Where the index declines over the lifetime of the trade, the purchaser of the future (i.e., the long position) pays the difference between the value at execution and the value at settlement.111 The inverse applies where the index increases in value. It is worth noting an important distinction between a position through stock index futures and the same position through underlying stock. Stock index futures do not enable the holder to exercise the rights of shareholders, such as rights to receive dividends or vote. This is identical to the position the buyer of futures would be in if the buyer instead contracted for a delivery of the stock on a future date through an off-exchange forward agreement (e.g., the deferred buyer would not be able to vote shares she did not yet have or receive dividends on such shares). However, this is a new feature relative to prior futures contracts. Prior futures did not involve an asset that could profitably be used in the interim between execution and settlement (e.g., the foodstuffs underlying agricultural commodities could not be eaten and then delivered, and interest rate futures were designed to reference an obligation that did not pay coupons between execution and settlement). This step further attenuated the requisite linkage between futures and related cash markets through a relatively greater “convenience” benefit to short party.112

In the few years after the approval of stock index futures, CFTC approval followed for a wide variety of cash-settled index-based products. For example, cash settled futures were approved based on indices representing the aggregate value of baskets of:

(1) foreign currencies, which were introduced starting in 1985 to enable positions based on the U.S. dollar’s relative value in global currency markets as opposed to its value relative to a specific currency;113 and

(2) corporate bonds, which were introduced starting in 1987 to enable positions based on bond portfolios such as those held by pension funds and insurance companies.114

Freight rate futures illustrate some of the ingenuity powering futures innovation as well as its dispersion beyond the U.S.115 Freight rate futures were the first service-based as opposed to property-based futures. They began trading on London’s Baltic International Futures Exchange (BIFFEX) on May 1, 1985.116 BIFFEX futures settle based on an index that reports the aggregate price of shipping cargo along a set of trade routes.117 While the routes vary greatly, as do the ships that are eligible to participate in the survey on which pricing is based, this aggregate provides a loose metric that reflects costs of shipping. After the BIFFEX futures, additional futures were developed with the first U.S. freight futures being approved two decades later in 2006 upon application from the newly formed Merchants Exchange of St. Louis.118

Index based futures, as developed below, pushed further on the traditional role of CFTC-regulated futures and their relation to cash markets. The Eurodollar contract had a concrete if hypothetical asset it referenced for purposes of calculating settlement price. Namely, Eurodollar futures settled against the market value of a deposit account with a specified balance bearing a rate of interest for a specified term. The deposit account was an asset with cash (i.e., spot) market equivalents, namely actual deposits made for specific terms in London and other financial centers outside of the U.S. The interest rate raised a complication, as LIBOR represented a rate synthesized from reported interest rates rather than a rate observed in cash market transactions. However, because LIBOR was a widely published and used reference for interest rates, it was relevant to cash markets.

Stock index futures differed from Eurodollar futures due to the multi-component nature of their referenced index. Admittedly, an “underlying asset” is recognizable in the context of an equity index futures.119 But this asset has a composite nature. The asset is not based on one transaction (e.g., purchase of grain, purchase of a Treasury bond, extension of credit through making a term deposit) but instead related to a large combination of transactions (e.g., 500 distinct purchases of shares from 500 different firms in the case of the S&P500 index). No single cash market is related to the futures contract, or is substitutable for the futures contract. As a result, pricing of the futures contract does not serve as a reference for pricing in cash markets. At the time Holmes wrote the majority in Board of Trade v. Christie Grain & Stock Co., farmers, wholesalers, exporters and others used prices established through futures trading on the CBOT and other exchanges to set the price at which they sold or purchased grain. This function of futures markets continued and was expressed in Section 3 of the Grain Futures Act and then the Commodity Exchange Act. This function is wholly absent in the context of equity index futures and other futures that use an index reflecting the price of a multi-transaction basket.

Other index contracts drifted even further from traditional links between cash and futures markets. A prominent illustration came on April 16, 1985 when the CFTC approved an application from the Coffee, Sugar, & Cocoa Exchange (CSCEX) of futures based on the consumer price index (CPI). A futures contract to hedge inflation was the brainchild of economists. Over a decade earlier–soon after the birth of currency futures and prior to interest rate products—Michael Lovell and Robert Vogel authored an article proposing a futures product that allowed hedging against inflation.120 CSCEX’s launch of CPI futures based on a basket of consumer expenditures drew tepid market interest, despite the nation’s difficult experience with inflation in the 1970s.121 Although economically of little import, conceptually this contract further expanded the CFTC’s jurisdiction to products with attenuated cash market linkage. To be fair, there are specific consumer expenditures (i.e., cash market activities) that compose the CPI. However, these transactions are myriad. The Bureau of Labor Statistics, which gathers the CPI, explains that:

The CPI represents changes in prices of all goods and services purchased for consumption by urban households. User fees (such as water and sewer service) and sales and excise taxes paid by the consumer are also included. Income taxes and investment items (like stocks, bonds, and life insurance) are not included.

The basket of purchases that the CPI tracks is extraordinarily broad, and as with the initial freight index, it is unlikely that any market participant will be exposed to the changes it tracks with any specificity.122 That is not to say that CPI futures cannot be used to hedge. They can, albeit only for the relatively short-term period for which futures are available. However, the multi-component nature of the index aggravates basis risk. A farmer selling one kind of wheat but hedging using CBOT’s wheat futures knows roughly the relationship between her wheat’s prices and the prices of the wheat underlying the CBOT contract. However, an exporter using BIFFEX contracts to hedge a few specific routes carries substantial basis risk that the index price changes due to prices of routes that are irrelevant to the shipper. Similarly, someone purchasing a CPI future may find that the CPI changes due to changes in the costs of services or goods the hedger doesn’t usually use. This is an important point. It may be that the hedger’s housing or food costs evolve differently from the housing or food costs reflected in the CPI. That is traditional basis risk (i.e., distinctions in prices of grain by grade, location or timing). Multi-component indices, however, raise a distinct type of non-correlation. It may be that the CPI includes expenditures that the hedger simply does not make, such as car-related expenses where the hedger lives in New York City and relies on public transportation. This slippage between indices and actual exposure may be more of a difference in degree than a difference in kind—again, basis risk is as old as futures—however, the attenuation is important in observing the expansion of the CEA’s reach.

Suitability for investment is an additional dimension along which agricultural futures, for which the CEA was established, differ from the futures markets the CFTC enabled by the end of the 1980s. Investors are distinct from hedgers and speculators. Investors have savings, which they seek to grow at market rates. This is distinct from hedgers, who seek to transfer risks incurred in the course of their business or other activity. And it is distinct from informed traders, who seek to make above market returns based on private information. While agricultural futures are not suitable investment products, futures the CFTC authorized since 1974 have features that may allow them to function as investment instruments.

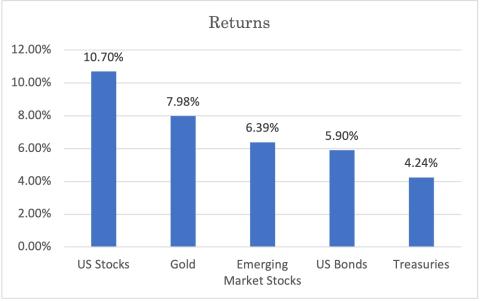

Derivatives are not a monolithic asset class. As already shown and will continue to be explored in reviewing the history of futures authorization, products have different features and have evolved over time. The asset(s) underlying a futures contract are important for understanding the behavior and potential uses of the contract. Foodstuffs are perishable goods that result from a production process that has become more efficient through time. This is reflected in the prices of many agricultural commodities. For example, the price of wheat increases by less than one percent per year, falling short of inflation.123 While agricultural commodities may have been suitable for short term speculation in anticipation of sharp supply changes (e.g., war, crop disease, weather), they generally cannot be used for investment.124 As a result, people typically do not use agricultural futures to park their savings. The expansion of regulated futures to other tangible commodities as well as financial assets, however, expanded the potential uses of futures to investment. Annual returns on gold, oil, government and private debt, and perforce baskets of public equities substantially exceed returns on foodstuffs. Figure III.C below illustrates returns on assets referenced in popular futures contracts to provide a general sense of how vastly their returns outperform the sub-inflation returns on agricultural commodities.

Figure III.C: Annual returns by asset class 1971–2024125

Investment using futures products is admittedly non-trivial relative to investment through funds and cash markets. An investor can buy shares or warehouse receipts for tangible non-perishable commodities and hold them in a brokerage account. Alternatively, a person can invest in a pool that holds these assets (and perhaps, other assets). In contrast, an investor using futures markets has to regularly incur transaction costs as futures expire, settlement takes place, and new futures have to be purchased. This is particularly true as typically futures with longer expiration periods have lower liquidity and higher transaction costs. Putting aside these practical considerations, however, the observation stands: the assets underlying regulated futures after the CFTC was established became increasingly suitable for investors willing to take market returns rather than just cash market participants seeking to hedge and speculators seeking to outperform the market. This was a reason that the CFTC began a turf battle with the SEC, which had traditionally overseen instruments through which firms obtained capital and investors allocated savings.126 This subject will be returned to in Part IV below.

C. Introduction of Event Contracts

In the two decades after its birth in 1974, the CFTC approved contracts referencing increasingly more exotic variables with pricing further and further removed from identifiable cash market transactions. These were heady days for those arguing against government involvement in market activity. By 1995, the Interstate Commerce Commission was abolished. Prior to that, the Berlin Wall fell and the Soviet Union collapsed. Although these events expressed something far more complex, and distinct from, the theorized merits of “free markets” as compared with centralized planning under the Communist model, these epochal milestones anchored popular perception, politics and directions of regulatory policy.

It was no accident that the approval of index-based products began under Ronald Reagan’s presidency. James Stone, who was chair of the CFTC under Carter, refused to approve the Value Line index futures. He likened equity index futures to “gambling.”127 It was only after Reagan’s chairman Phillip McBride Johnson took over running the CFTC that index-based futures were authorized. First, Johnson led approval of the Eurodollar futures and then the approval of Value Line and other equity index futures.128

Derivatives implicate longstanding social concerns with the balance between profits and productivity. Humans have been suspicious of financiers for millennia as examined in usury scholarship, among other fields.129 As people get wealthy through financial activity, some mix of resentment and genuine concern over resource allocation poses the question: what has this person really done to earn her wealth? Allen Frankel, who was among other things a chief economist at the Federal Reserve in the 1980s, frankly and eloquently reflected:

[I]n many quarters, questions continue to be raised about the rationale and justification of the proliferation of financial futures contracts and about whether, in fact, such markets mainly serve to provide opportunities for speculation. Those who take this view generally see recent innovations in financial techniques as having adversely affected economy-wide productivity growth. James Tobin has expressed such sentiments by admitting to ‘. . . an uneasy Physiocratic suspicion, perhaps unbecoming in an academic, that we are throwing more and more of our resources, including the cream of our youth, into financial activities remote from the production of goods and services, into activities that generate high private rewards disproportionate to their social productivity.’130

Complicating views on the value of financial activity are the resemblances and overlaps between financial activity and gambling, which were already introduced above. Judgments, or simply assumptions, about the risks and social utility of finance—and derivatives specifically—define political positions.131 And appointees predictably express party positions as they lead agencies.132 Under the post-Cold War pre-2008 Financial Crisis presidencies of George H. W. Bush, Bill Clinton and George W. Bush, futures markets (and derivatives markets more generally) received increasing deference from lawmakers.133

Before George H. W. Bush completed his presidency, the CFTC began to approve futures and options without cash market references. These included contracts that CBOT submitted to the CFTC in June 1990, which would settle on the basis of insurers’ operating experience.134 CBOT catastrophe insurance futures provide an example. Following a protracted approval process, these futures began trading in December 1992.135 The futures settled on the basis of an index tracking experience among property and casualty insurance providers.136 The index consisted of a numerator and a denominator. The former expressed claims for property and casualty losses over a quarter under a set of policies. The latter aggregated premia paid for those policies. As a result, the index proxied for the ex post profitability of a set of policies (i.e., it was a ratio that captured important features of insurers’ cost and revenue structures).137 The index was not based on the price of any product, instead reflecting a partial measure of financial performance.138 Contemporaneously, the CFTC approved similar products for health insurance and homeowners insurance. With the approval of these products, the CFTC effectively announced that futures could be settled based on variables other than market prices.

In the same period, Hayekian philosophy concerning the information aggregating capacity of market-pricing bloomed into application. Naturally, the first to express theory in action were academic economists. In June 1988, the Iowa Electronic Market (IEM) began trading contracts that settled on the basis of who would win the 1988 election in which the main three candidates were George Bush, Michael Dukakis and Jesse Jackson. The market offered participants a bundle of four contracts it sold for two dollars and fifty cents ($2.50). There was one contract for each of the main three candidates and one for the rest of the field. Market participants could unbundle and sell the contracts via the exchange. Following the election, each contract would pay a product determined by multiplying $2.50 by the relevant candidate(s) share of the popular vote. Because the popular vote would sum to 100% across the contracts, the bundle of contracts would necessarily pay $2.50 at settlement. However, the price of each individual contract within the bundle fluctuated based on how much of the popular vote the referenced candidate(s) were expected to receive. For example, if a candidate received 10% of the vote, the contract referencing that candidate would pay $0.25 (i.e., 10% * $2.50). As a result, to the extent market participants could anticipate the outcome of the popular vote, they would sell the contract for anything over a quarter and buy the contract for prices below that. The IEM reflected the computerization of the financial industry in the 1980s and was wholly electronic, allowing participants to submit orders to buy or sell contracts at specific prices via personal computer. The IEM had 192 participants trading on the 1988 election and the pricing that derived from their judgments predicted the popular vote extremely well.

The IEM was unregulated when it was formed. To avoid state law prohibitions on gambling, the IEM exclusively served members of the University of Iowa community.139 To expand participation, the IEM sought relief from the CFTC prior to the 1992 election. The IEM submitted a request for a no-action letter to the CFTC, which the CFTC granted on February 5, 1992. Notably, the no-action letter did not take a position as to whether IEM markets traded in CFTC regulated contracts.140 Whether or not the proposed contracts were subject to CFTC regulation, the no-action letter stated that the CFTC would not take enforcement action provided certain conditions were met.141 The conditions were meant to assure that the IEM operated at a small scale as an experimental, non-commercial venture that lacked the economic clout to seriously impact political outcomes. These conditions included that the professors operating the IEM did not receive related compensation, that there were fewer than 2000 participants, that the maximum purchase by any participant was capped at $500, and that the IEM operate exclusively for an academic or experimental purpose.142 Following the birth of the IEM, additional academic projects were launched that used markets to predict election outcomes.143 The no-action relief granted to IEM birthed a parallel strain of instruments, which were outside of the CFTC’s jurisdiction, and devoted uniquely to aggregating information as distinct from enabling hedging, pricing, or investment.

While IEX and other small or foreign prediction markets began to operate outside of the CFTC’s jurisdiction, regulated exchanges continued to develop more and more exotic regulated products. In 1995, CBOT received authorization for a number of futures144 with settlement based on crop yields of specific agricultural products in specific areas. Yield futures demonstrate both a gap in traditional agricultural futures and a step beyond them. The prototypical farmer could use traditional grain futures to hedge against fluctuations in the price of grain. For example, at the time of planting, the farmer could enter into a contract to deliver 1,000 bushels in the September or December following the summer. The farmer would be paid based on current prices of wheat when selling those futures. In exchange, the farmer would deliver the wheat in lieu of selling it at September or December prices (or, alternatively, offset the futures obligation through buying inverse futures at the time of settlement and then delivering her grain to the market based somewhat on the price of the offsetting futures). This enabled the farmer to shed price risk. But this transaction did nothing about “yield” risk, or the farmer’s uncertainty as to the volume of her harvest. How could the farmer know when planting how many bushels of wheat she would have to sell? If she used her historical averages, she may oversell futures in a bad season or remain partly exposed to market price fluctuations in a good season. As a result, farmers generally waited long after planting to get a sense of their harvest (i.e. yield) before hedging price. Yield futures addressed this distinct source of risk.

For example, the CBOT introduced futures covering the harvest of corn in Illinois within specific periods.145 These contracts settled on whether actual yields exceeded or fell short of historical averages. Crop yield futures were not-price based. Instead, they settled based on growing and harvest season-end reports of yield from the U.S. Department of Agriculture.146 The futures enabled hedging based on the volume of wheat produced. Where state level events (such as weather, pests, fertilizer costs, diseases) as distinct from farm-specific events affect harvests, farmers and other users of grain can use the futures to obtain a hedge against variations in volume.147 Notably, the underlying events referenced in yield futures are not financial. As discussed above, insurance futures approved in 1992 moved beyond price variables in calculating settlement values. However, the insurance futures were based on financial events, namely, payments of premia and coverage of related claims. In contrast, yield futures were based on natural phenomena, namely, the volume of plants generated by an acreage. The index was sourced from a government agency, thought to be neutral and credible. As the variables permitted to drive cash payments under regulated futures contract became more exotic and departed further from prices observed in cash markets, the CFTC drew no lines and instead approached contract submissions on a case-by-case basis.

The CME became an innovator in weather derivatives, i.e., futures and options that settled on the basis of weather events. Since harvest futures had been approved, phenomena from the natural world were fair game for settlement. In 1999, the CME obtained approval for futures and options that settled against an index tracking temperatures.148 Specifically, the index tracked the extent to which daily temperatures in a period exceeded or fell short of the sixty-five degree Fahrenheit threshold below which utilities need to provide heating and above which additional electricity is needed for air-conditioning. Subsequent weather-related exchange traded contracts would settle on the basis of other natural phenomena such as wind-related events (e.g., number of named storms that make landfall in the U.S.), levels of precipitation (e.g., regional snowfall or rainfall), and various fluctuations in temperature.

Without any requirement to transfer risk based on changes in market prices, instruments only had to serve hedging purposes to demonstrate their listing eligibility. But as already observed, the extent to which a contract has hedging utility is a question of degree. Even traditional grain futures impose basis risk. The extent to which a contract’s settlement price evolves inversely with a hedger’s exposure is a highly context dependent question and can only be observed in hindsight with all the defects of hindsight bias. Thus conditioning contract approval on a level of hedging utility poses difficult questions for the CFTC.149 How are the lawyers and economists at the agency to judge whether a proposed product would meaningfully serve market participants’ hedging needs? To what extent should the CFTC be too liberal or too conservative in permitting contracts, particularly given the myriad reasons even contracts with substantial hedging utility fail? The CFTC could choose to err in favor of being too deferential to markets and approve contracts with scant hedging functions, or it could err in favor of being too strict and reject contracts that could have had substantial uses in neutralizing risk. Instead of taking time to reflect and formulate a comprehensive policy on product approval that takes into account the CFTC’s legal authority and the principles that the agency serves, the CFTC engaged in decades of contract-by-contract review that led it down a slippery slope. There are a number of possible explanations for the CFTC’s failure to invest in long-term guidance, which this Article leaves largely unexamined.150 Whatever the explanation, the result was a step-by-step expansion in the permissible types of contracts and put the CFTC in the difficult position of considering applications for futures wholly unmoored from cash market prices.

In 2001, HedgeStreet filed an application to become a CFTC-designated trading market.151 From its inception, HedgeStreet sought only to list event contracts.152 Its application went through a grueling process during the first term of the George W. Bush presidency.153 HedgeStreet was the first applicant to seek designation under a new regime that came into place with the Commodity Futures Modernization Act of 2000. As amended by that Act and discussed further below, the CEA continued to serve a “public interest” defined as enabling hedging and cash market pricing;154 however, a requirement that the CFTC review every listed futures and options contract to assure that the product would serve this public interest was removed.155 Prior to its approval, HedgeStreet represented that it “anticipat[es] that its contracts would allow institutions and individuals risk management opportunities that existing exchanges do not provide, although HedgeStreet did not file any contracts with its application.”156 On February 10, 2004, after more than two years of analysis and a resubmission, the application from HedgeStreet was granted.

HedgeStreet was a unique contract market when it was formed. It included a clearing facility, which was approved together with the exchange. The clearing facility was trivial, because of how HedgeStreet designed its contracts. As detailed in its rulebook,157 HedgeStreet listed only binary options.158 These were contracts similar to what the IEX had designed, which required no margin or other sophisticated risk management because they were fully prepaid, i.e., parties to the contract did not have contingent payment obligations.159 HedgeStreet sold two-contract bundles, and supported trading in the individual contracts. The components of the bundle were designed to be mutually exclusive and comprehensive of all potential outcomes. For example, in a bundle referencing a merger between two companies, the two contracts would pay in opposite cases.160 The first contract would pay the price of the bundle less transaction fees if the merger occurred within the year; the second contract would pay the price of the bundle less transaction fees otherwise.161

Between 2006 and 2007, Hedge Street began trading contracts that settled on the basis of whether a specified level of (a) yield per acre was achieved for an agricultural product in a particular region and time period; (b) damage was done by hurricanes or other storm events in a specified region over a specified time period; and (c) initial jobless claims was reported by the U.S. Department of Labor. HedgeStreet also listed binary options that settled on the basis of: (1) natural gas and crude oil inventory levels; (2) economic variables such as retail sales, unemployment claims, manufacturing levels, and nonfarm payrolls; (3) prices of gasoline, heating oil, propane, residential real estate, prescription drugs, hospitality services and other consumer expenditures; (4) currency exchange rates; and (5) storm and hurricane damage estimates.162