Pills in a World of Activism and ESG

Easterbrook and Fischel’s The Economic Structure of Corporate Law advances their now famous passivity thesis, which posits that managers should remain passive in the face of an unsolicited tender offer for the company’s shares. Consistent with the broader Chicago-school economic belief, Easterbrook and Fischel argue that markets are generally efficient, and therefore restrictions on the market (like poison pills) are bad. In doing so, Easterbrook and Fischel also consider and reject externalities that might cause the market for corporate control to not function well. Thirty years have passed since Easterbrook and Fischel’s seminal work and the world has changed in meaningful ways, with the rise of stakeholder governance, ESG, and stockholder activism. We therefore propose some ground rules that would govern pills in today’s corporate world. These rules, we believe, would effectively balance the board’s interest in considering a broad set of constituencies and the challenges of facing increasingly sophisticated and coordinated shareholder activists against the rights of all shareholders, including activists, to solicit support for their ideas or attempt to gain control of the company.

I. Introduction

Poison pills (or “shareholder rights plans”)1 were just gaining traction in corporate America in 1991 when Frank Easterbrook and Daniel Fischel published their seminal work The Economic Structure of Corporate Law.2 One of us devoured the book a few years later, while a 2L in Professor Lucian Bebchuk’s advanced corporate law class at Harvard Law School; the other of us was not born at the time of publication but encountered its fingerprints throughout her work at Wachtell, Lipton, Rosen & Katz and now as a junior scholar in the field. Everyone in between us has read it, or at least knows its key points. It has influenced a generation of scholarship and practice, and it is impossible to be an academic in corporate law without having grappled with its provocative and powerful ideas.

On the question of pills, Easterbrook and Fischel were not fond of them.3 Because they dilute the potential acquiror’s or activist’s ownership interest if triggered, pills force the hostile acquiror or activist to negotiate with the target company’s board of directors and deter a hostile takeover or stockholder activism. In contrast, Easterbrook and Fischel’s famous passivity thesis posited that managers should remain passive in the face of an unsolicited tender offer for the company’s shares.4

When Professors Lucian Bebchuk and Ronald Gilson proposed that management should be allowed to resist tender offers just a bit—to generate an auction for the company—Easterbrook and Fischel vehemently disagreed in a now-famous debate, pointing out that facilitating auctions would only transfer wealth from buy-side shareholders to sell-side shareholders, and by reducing buy-side profits it would reduce incentives for the all-important buy-side search for under-performing targets.5 Easterbrook and Fischel rightly observed that if deals were generally value-creating, then the corporate law rules should maximize the frequency of such deals. Their passivity thesis would do just this.

As Easterbrook and Fischel noted in The Economic Structure of Corporate Law, their approach to pills is consistent with their overall Chicago-school belief that markets generally work well, and therefore things that restrict markets from working (like pills) are bad. Also following in the broader Chicago-school economic tradition, Easterbrook and Fischel consider externalities that might cause the market for corporate control to not work well. Here, they consider, but reject, the possibility that exploiting other constituencies might be a reason that motivates tender offers.6 Resembling others who were writing at the time,7 they consider—but reject—the specific possibility that a tender offer would be motivated by breaching implicit contracts with employees:

Although this is a logically possible method of exploitation, it also comes with a logical obstacle. Incumbent managers don’t pull this trick on other workers because the firm’s success depends on its reputation for honest and reliable dealing. . . . It makes no sense for an acquiring firm to pull off this stunt . . . Even if it can find a target at the end of its life cycle, the bidder must worry about its own reputation. Needing to attract its own labor force, it cannot squeeze the target’s workers without paying a large price. In other words, opportunistic, last-period exploitation of labor markets makes less sense when done by a bidder than it does by incumbent managers—the bidder’s costs of this strategy are much larger. A desire to squeeze workers therefore is not a plausible explanation of tender offers.8

Easterbrook and Fischel’s consideration of externalities in support of the passivity thesis was necessarily a product of the corporate landscape at the time of their writing. However, the world has changed in meaningful ways since the 1990s, and the relevant constituencies and role of poison pills must adapt accordingly.

This paper proceeds in four parts. Part I briefly introduces Easterbrook and Fischel’s position on poison pills. Part II describes the rise of stakeholder governance, ESG, and stockholder activism. Part III conducts an empirical analysis of currently active U.S. pills and provides recommendations for modern pill design that respond to the increasing sophistication of stockholder activists. Part IV concludes.

II. The Rise of Stakeholder Governance, ESG, and Stockholder Activism

Fast forward thirty years from the time of The Economic Structure of Corporate Law. The concept of corporate purpose and stakeholder governance—the consideration of shareholders, employees, customers, communities, and other stakeholders in corporate governance—has increased “as part of a corporate strategy that achieves sustainable long-term growth and creates long-term value for the benefit of all stakeholders.”9 With this rise in stakeholder governance, environmental, social, and governance (ESG) factors, which encompass issues ranging from diversity and human rights to climate change and sustainability, have become critical. 10 ESG is quickly rising to the top of boardroom and shareholder agendas.11 Amid the ongoing COVID-19 pandemic, the 2021 proxy season saw more ESG-focused shareholder proposals—and support of those proposals—than ever before.12 And on the corporate side, an increasing number of companies are embracing ESG issues “as a strategic business imperative.”13 At the end of the 2020 proxy season, a record 90% of S&P 500 companies published an ESG report, an increase from 20% a decade ago.14 Furthermore, complacency on ESG issues in the boardroom can backfire, as directors may find themselves facing an event-based derivative securities class action lawsuit for losses attributed to unexpected events like environmental disasters, cyberattacks, and employment practices.15 Most experts today agree that ESG is a desirable force.16 And even for those who question the value of ESG considerations in for-profit corporate structures, there is no doubt that ESG will be with us for the foreseeable future.

Stockholder activism—when a stockholder purchases a company’s shares with the primary intent of influencing corporate strategy or governance—is a hallmark of the modern corporate landscape and has sharply increased over the years. In 2021, 886 companies were publicly subjected to activist demands, an increase from just 155 a decade ago.17 Activist stockholders use proxy fights and other tools to pressure companies to change,18 often through demanding a company change management or operations, or pursue (or halt) a merger or other transaction. Despite an ongoing debate about whether activism is good or bad,19 there is no doubt that it too will be with us for the foreseeable future. Pill design features are critical now more than ever given the evolving role of shareholders and the resulting rise of “anti-activist” pills.20

Stockholder activism and ESG interact in meaningful ways. While traditional activism focuses on short-term profit and total shareholder return, the rise of ESG has brought with it a new set of activists concerned with ESG-related issues.21 Modern activism includes dual-purpose activists who combine shareholder-return and ESG arguments, as well as “pincer attacks” from ESG and shareholder-return activists acting independently or in concert against the same company.22

However, ESG and activism can also clash, particularly when a traditional shareholder-return activist seeks to maximize short-term shareholder profit in a manner that conflicts with a board’s long-term ESG considerations.23 As other scholars have aptly put it, “[a]ctivists acquire an economic interest in a target . . . [f]irst and foremost, [because] they want to profit,” and accordingly they “develop proposals that, in their assessment, would increase the company’s share price.”24 Many activist campaigns focus on mergers and acquisitions (M&A) rather than ESG issues, with campaigns centering on agitating for the sale or consolidation of a company, pressuring a company to divest a line of business, or efforts to sweeten or scuttle an existing deal. In 2021, for example, M&A-related campaigns remained the most common campaign objective, representing 43% of all campaigns.25

When ESG-related corporate governance objectives and shareholder activism conflict, pills serve a critical purpose in the current era by preventing activist plays (no longer hostile takeovers) motivated by extracting value from other constituencies that today’s corporate governance world feels the need to preserve and promote, such as the various stakeholders that benefit from the board’s consideration of ESG issues.

We therefore propose some ground rules that would govern pills in an activist and ESG world. Pills declined to the point of near irrelevance before 2019; 26 as a result, there was little commentary about them, both academic and practitioner. Then pills spiked in March 2020, due to the precipitous decline in market values from COVID-19, with correspondingly little guidance that wasn’t ten years old. Thankfully, while the pandemic is still very much with us, equity markets have come back to and in most cases exceeded their pre-COVID levels. It is useful on this relatively clear day to provide guidelines for good pill design. The overarching objective is to effectively balance the board’s interest in considering a broad set of constituencies and facing sophisticated and coordinated activists against the rights of all shareholders, including activists, to solicit support for their ideas or attempt to gain control of the company.

III. Pill Design in an Activist and ESG World

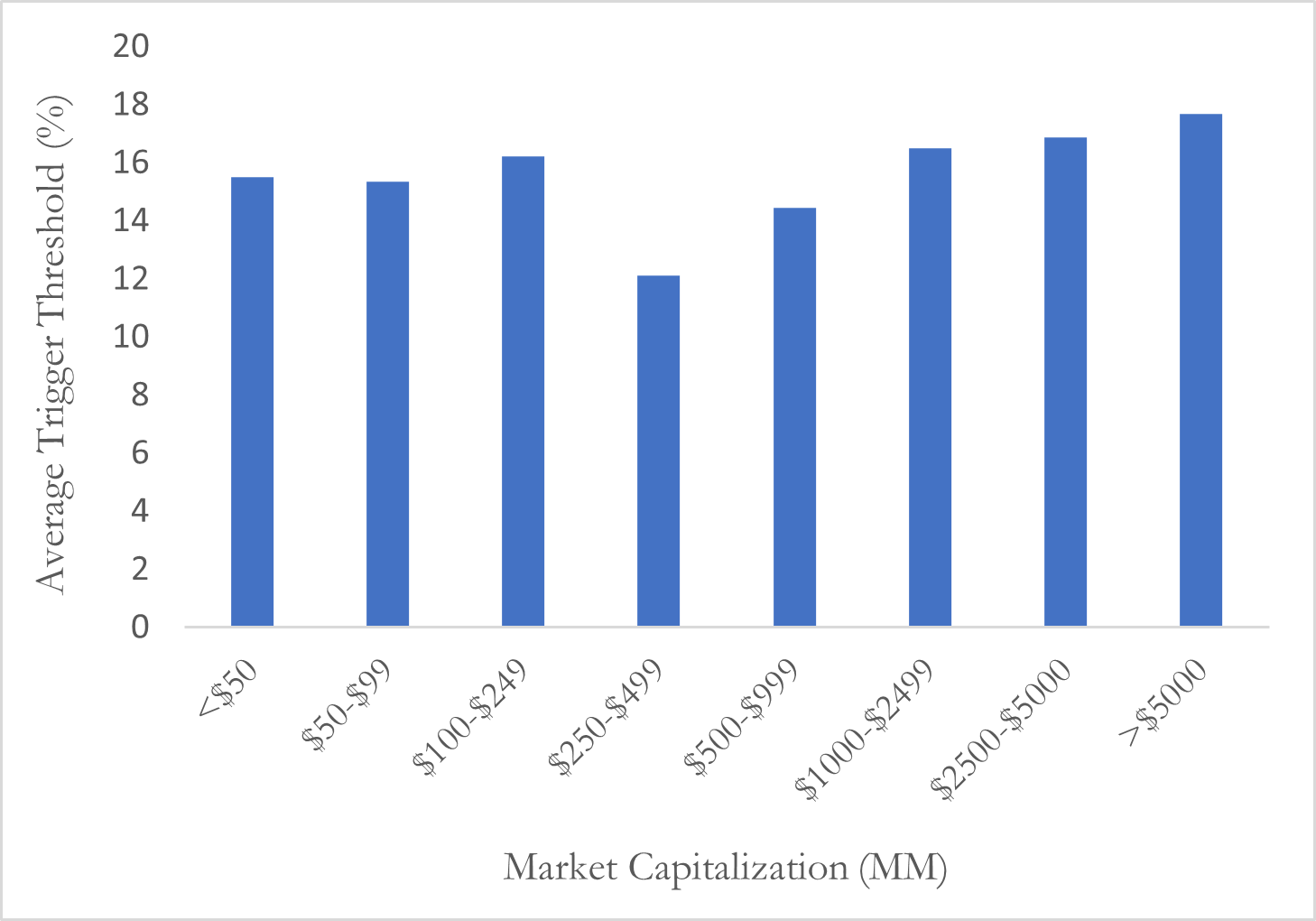

A. Pill trigger thresholds should be assessed against market capitalization.

When it comes to pills, the ownership threshold required for the pill to be triggered is typically 10–15% for non-passive investors. This threshold rarely discriminates by the size of the company in question.27 Indeed, there is no inverse correlation between market capitalization and trigger threshold. Exhibit 1 details the trigger thresholds for U.S. and Canadian pills as provided by the RiskMetrics database as of February 2022:

Exhibit 1: Trigger Thresholds for U.S. and Canadian Pills

(excludes NOL pills)

As a matter of policy, we propose that larger companies should be given more tolerance on the trigger percentage for poison pills because the toehold stake is so much larger; in today’s world, what is relevant is the dollar stake an activist can acquire, not the threshold percentage. For example, a 5% threshold in a large company (e.g. $30 billion market capitalization) is probably more friendly to an activist than a 10% threshold at a smaller company (e.g. $5 billion market capitalization). In part, this is because for small-market capitalization companies, there generally must be a higher percentage equity stake than for larger companies to make a proxy contest worthwhile.28 The reason for this distinction is that, as a proportion of the value of the company, the costs of a challenge tend to be higher for small companies than for large ones.29 To make these higher proportionate costs worthwhile, activists must have greater proportionate gains, and to convince other stockholders that increased company value (rather than private control) is the source of the gains, an activist must have a higher economic stake in the company.30

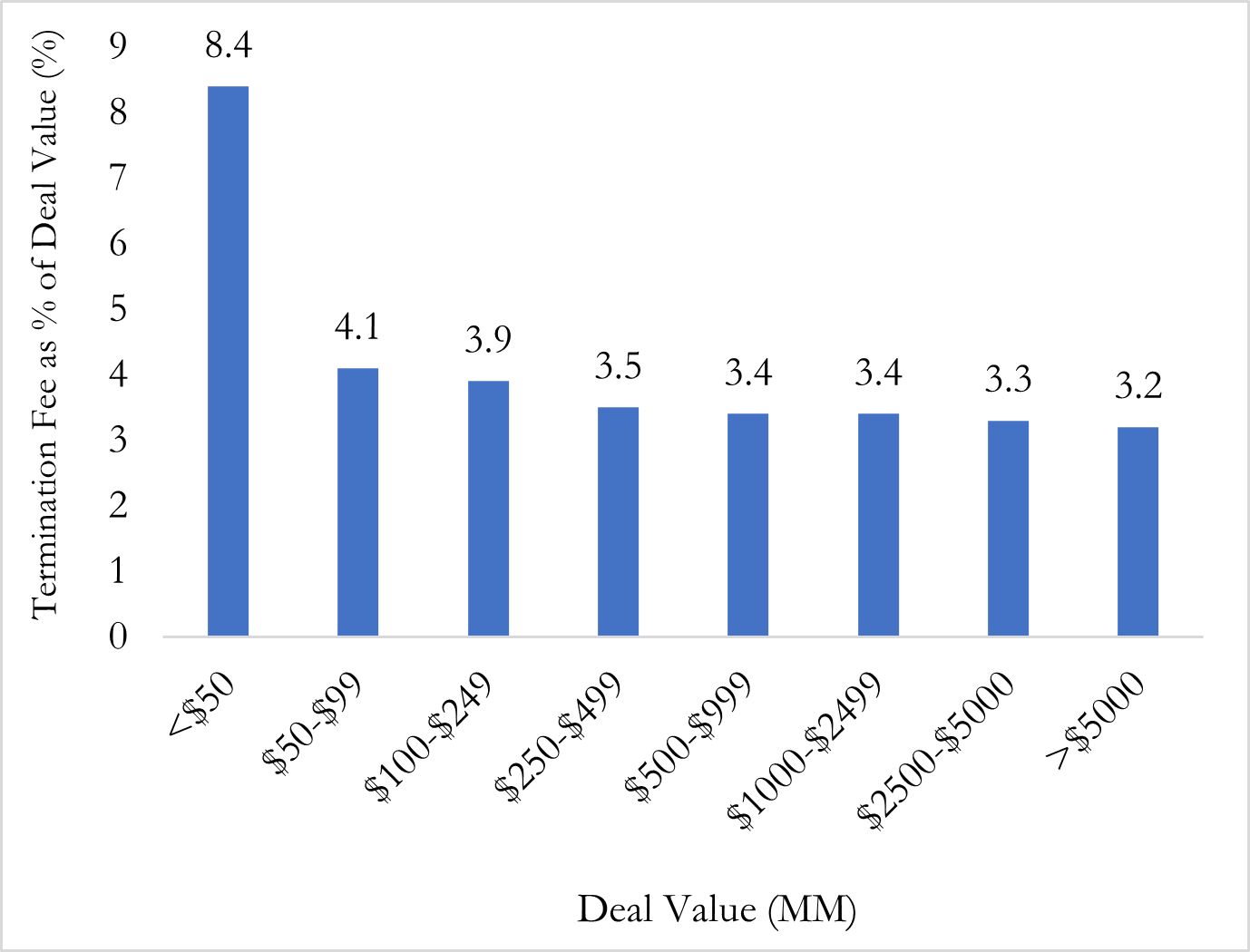

Employing differing thresholds based on overall value is not a new phenomenon in corporate law. This practice has already been endorsed with respect to deal protection. For example, when it comes to termination (or “break-up”) fees payable by the target company if a merger agreement is terminated under specified circumstances, Delaware courts have made clear that there is no bright line rule or fixed percentage;31 rather, Delaware courts consider the size of the deal in determining the reasonable magnitude of the termination fee. Thus, a 6% termination fee in a $50 million deal may be permissible, but a 6% fee in a $5 billion deal may not. Indeed, as illustrated in Exhibit 2, prior studies have shown that as the deal size increases, the percentage of the fee decreases.32

Exhibit 2: Termination Fees Assessed Against Deal Size

While variation by company size (i.e. market capitalization) has not yet been implemented in pill doctrine, it would seem logical to apply the same principle that exists in deal protection doctrine to pill trigger thresholds. Such an approach would also represent good policy, particularly given the ten-day window before stockholders must file their Schedule 13D with the Securities and Exchange Commission (SEC), which allows stockholders to amass significant stakes in a company before the company can adopt a poison pill.33 Because the SEC and Congress have failed to close this ten-day window, which would prevent lighting-strike attacks, larger companies should be able to engage in self-help. Accordingly, a threshold of 5% for particularly large companies may be appropriate and also aligned with Schedule 13D.

In addition, a pill may have different (or “bifurcated”) triggers for different shareholders. There are two common discriminatory triggers; a pill may grandfather in an existing large shareholder, as in Yucaipa, or impose different thresholds for certain filers (e.g. Schedule 13D and 13G (passive) filers), as in Third Point.34 At first glance, grandfathering in an existing large stockholder seems problematic, in part because it results in an uneven playing field that preserves the power of a grandfathered stockholder (who is often supportive of management). However, as prior commentators have noted, such pills can serve a purpose in limited scenarios when antagonistic stockholder conduct alerts the board to the need to adopt the pill and the board wants to constrain other subsequent investors.35 Differing triggers for Schedule 13D and 13G filers, in contrast, are easier to justify. This categorical distinction makes logical sense given that Schedule 13G filers acquired the securities in the ordinary course of business and not with the purpose or effect of changing or influencing the control of the company. Thus, a Schedule 13G filer is less of a “threat” than a 13D filer, who has a history of activism or may turn active.36 More than half of the seventy non-net operating loss poison pills adopted in 2020 bifurcated the triggering percentage.37

B. Acting in Concert provisions should prohibit parallel conduct.

Contrary to academic commentary, which has only focused on AIC provisions over the past decade or so, even the very earliest pills, including the Household International pill that was litigated in Moran,38 had an AIC concept. Early pills used language tied to the definitions of a “group,” “affiliate,” and “associate” under Section 13D and Rule 12b-2 of the Exchange Act.39 Later pills—call them second-generation—broadened the concept but still required an “agreement, arrangement, or understanding.”40 Whether tethered to Section 13D or something broader, this “group” concept was necessary because, without aggregation of affiliated entities, it would be exceedingly easy for an acquiror to, for example, acquire 3% through each of ten affiliated entities without triggering the pill.

The express agreement pills observed that the agreements did not need to be in writing. Nevertheless, by requiring express agreement, these first and second-generation pills did not capture implicit agreements. Savvy activists, fully aware of the “express agreement” language, might (and did) collaborate with other investors through informal arrangements (also known as “wolf pack” activity) rather than explicit agreements, thereby not triggering these pills.41

Third-generation AIC provisions filled this gap by capturing shareholders “acting in concert” even without an express agreement. Instead, what is required is “parallel conduct.” Typical language defines “acting in concert” as follows:

[A Person shall be deemed to be] ‘Acting in Concert’ with another Person if: such Person knowingly acts (whether or not pursuant to an express agreement, arrangement or understanding) at any time after the first public announcement of the adoption of this Right Agreement, in concert or in parallel with such other Person, or towards a common goal with such other Person, relating to changing or influencing the control of the Company or in connection with or as a participant in any transaction having that purpose or effect.”42

The standard formulation further requires that “each Person is conscious of the other Person’s conduct and this awareness is an element in their respective decision-making processes” and that “at least one additional factor supports a determination by the Board that such Persons intended to act in concert or parallel.”43

In our opinion, these third-generation “parallel-conduct” AIC provisions, along with the protection of a board-determination guardrail, represent an appropriate response to increasingly sophisticated activist attacks. Such third-generation AIC provisions are not only appropriate, but indeed best practice in response to activists who could too easily evade the “express agreement” AIC provisions through parallel conduct and/or wolf pack activity. In fact, recently the SEC recognized the importance of a conception of groups that extends beyond express agreement, proposing to amend Rule 13d-5 to “make clear that the determination as to whether two or more persons are acting as a group does not depend solely on the presence of an express agreement and that, depending on the particular facts and circumstances, concerted actions by two or more persons for the purpose of acquiring, holding or disposing of securities of an issuer are sufficient to constitute the formation of a group.”44

Once the AIC provision is no longer tethered to an express agreement, concern arises, of course, over a board’s judgment calls about whether shareholders “intended to act in concert or parallel.” These judgment calls introduce ambiguity, and critics of third-generation AIC provisions might argue that the ambiguity will have a chilling effect on socially desirable conversations among shareholders about the company. In response to these valid criticisms, we would suggest that the guardrail of a board determination is not a trivial thing. In general, no board wants to trigger a pill—it can wreak havoc on the company’s balance sheet45 —and in instances where it does not wreak such havoc (due to the availability of a share exchange feature) it still represents a significant board decision to deliberately dilute a shareholder; and all of these board determinations are of course subject to the board’s fiduciary duties to all shareholders. In contrast to certain board decisions that are deliberately prevented in order to avoid triggering fiduciary duties (such as don’t-ask-don’t-waive standstills in confidentiality agreements), these third-generation pills require a board determination as a guardrail on a pill trigger, with full awareness that such decisions are subject to fiduciary duties.

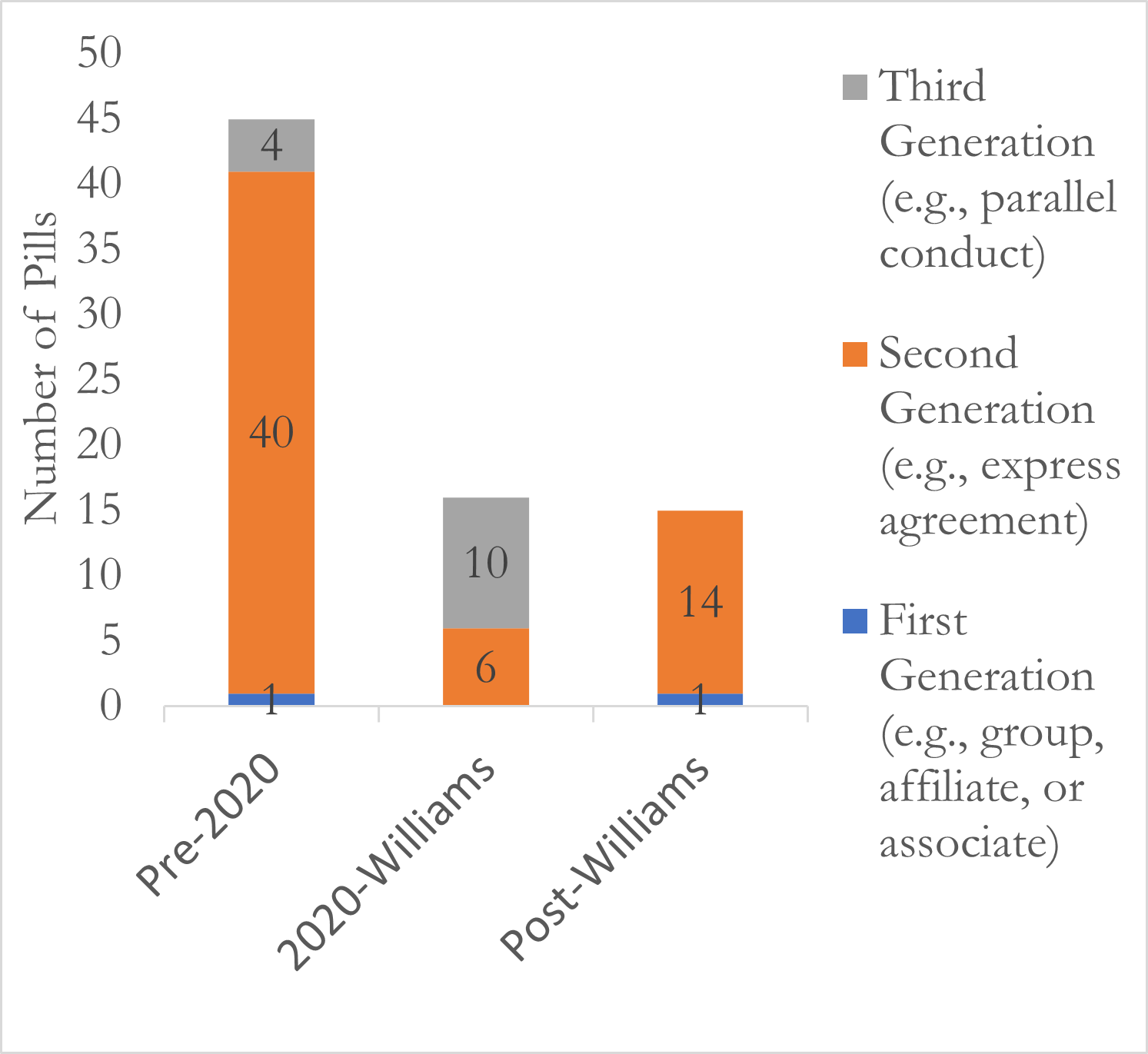

To examine the proliferation of what we claim to be best practices for AIC provisions, we examined pills in force as of February 2022 for U.S. companies identified in the RiskMetrics database (n=76) (the Sample).46 Across the Sample, 45 of these AIC provisions were adopted before 2020; the remaining 31 were adopted in 2020 and later, mostly in the immediate aftermath of the stock market decline caused by the global outbreak of COVID-19 in March 2020. We find that across the Sample, 18% (14 out of 76) were third-generation pills with a parallel conduct structure, i.e., shareholders acting “in concert or in parallel,” regardless of whether there was an express agreement. The majority (71%) of these third-generation pills were adopted in 2020 or later. All but one of these third-generation pills had a “parallel conduct + guardrails” structure, i.e., with a board determination of an additional factor indicating “that such Persons intended to act in concert or parallel.” Exhibit 3 illustrates the prevalence of certain AIC structures in the Sample.

Exhibit 3: Acting-in-Concert Structure

(excludes NOL pills)

In the years leading up to the recent case, Williams Companies Stockholder Litigation, where the plaintiffs successfully challenged an anti-activist pill adopted by The Williams Companies, Inc. at the outset of the pandemic,47 practitioners were gravitating to a better mouse trap (at least with respect to deterring wolf packs) by including third-generation pills with greater frequency. Prior to Williams (n=61), 23% of pills included a third-generation parallel conduct structure. In the four years preceding Williams (n=33), the proportion of pills with a parallel conduct provision rises to 42%. And in the year prior to Williams, nearly two-thirds (63%) of the pills included a parallel conduct AIC provision. All of the third-generation parallel conduct pills (n=14) were adopted in the four years prior to Williams. The fact that the “parallel conduct + guardrails” structure for third-generation AIC provisions was significantly increasing in incidence over time is at least suggestive evidence that practitioners were trending towards considering the third generation “parallel conduct + guardrails” structure to be the best response to increasingly sophisticated activist attacks.

However, practitioners quickly reversed course following Williams. None of the fifteen pills post-Williams contain a parallel conduct structure. Instead, these pills use first- and second- generation structures. Given the timing of this reversal in relation to the timing of the Court of Chancery’s decision in Williams, the reversal is likely in reaction—perhaps an overreaction—to Williams. Recall in Williams that the plaintiffs successfully challenged an anti-activist pill that contained “a more extreme combination of features than any pill previously evaluated by [the Delaware Court of Chancery].”48 The Williams court did not single out third-generation, parallel conduct provisions as the sole source of its decision, instead discussing the combination of “a 5% trigger threshold, an expansive definition of ‘acting in concert,’ and a narrow definition of ‘passive investor.’”49 Nevertheless, in the wake of Williams, practitioners have taken a cautious approach and avoided parallel conduct structures entirely despite the uncertainty of whether parallel conduct provisions alone would warrant the holding in Williams. It remains unclear whether this wholesale departure from third-generation pills in the wake of Williams can be justified as an appropriate reaction to the holding of the case alone.50

Despite the pervasiveness of AIC provisions in practice, Delaware courts have expressed skepticism about AIC provisions that go beyond express agreements to also capture parallel conduct.51 Nevertheless, if AIC provisions can only capture express agreements, activists will simply avoid express agreements. This would create a barn-door size loophole for poison pills in today’s markets.

C. Pill details matter: daisy-chain provisions and provisions capturing synthetic equity are not only appropriate, but necessary.

Just as vaccines must evolve to block ever-mutating strains of COVID-19, pills have morphed over the past thirty years to respond to increasingly complex and sophisticated activist attacks.52 These pill details matter: without certain features, a pill can be rendered completely ineffective by end-run attacks. In this section we primarily discuss two such features: daisy-chain provisions and provisions that capture synthetic equity. Each should be endorsed as a reasonable response to the increasing sophistication of activist “offense.”

1. Daisy Chains

Many modern poison pills may also include a “daisy chain” concept, which provides that stockholders are acting in concert with one another by separately acting in concert with the same third party. A typical formulation reads as follows: “[a] Person who is Acting in Concert with another Person shall be deemed to be Acting in Concert with any third party who is also Acting in Concert with such other Person.”53 That is, any stockholder acting in concert with one person is also acting in concert with every other person with whom that one person is independently acting in concert. The majority (71%) of third-generation pills in the Sample contain a daisy chain provision. Without a daisy chain provision, it would be again too easy to evade a pill: large shareholders could coordinate their activities through a middleman who holds a trivially small percentage of the company. Accordingly, absent a daisy chain provision, activists could coordinate explicitly (even in writing), as long as each individual activist plus the middleman stayed below the trigger threshold. The absence of a daisy-chain provision would create yet another barn-door size loophole for today’s pills, when viewed against the sophistication of activist attacks.

2. Synthetic Equity

In addition to daisy-chain provisions, the definition of beneficial ownership in a pill plays an important role in determining its effectiveness. Historically, most pills contained triggers based on a stockholder acquiring beneficial ownership exceeding a certain threshold of the company’s stock. However, the bounds of “beneficial ownership” under a classic poison pill definition are not entirely clear. Thus, in recent years, poison pills have increasingly included “synthetic equity” (swaps, options, or other instruments that confer an economic interest to the holder) in the definition of ownership.54 While synthetic equity entails no voting rights, it still creates threats that may justify a poison pill by empowering the activist with a larger economic stake, some or all of which may be convertible or “morphable” into shares, and credibility (and influence) with the other shareholders.55 In Williams, the court criticized the pill’s “beneficial ownership” definition as going beyond the federal definitions to capture synthetic equity, such as options.56 But a pill that does not capture synthetic equity (at least with regards to synthetic equity that is morphable into shares with voting rights) would provide yet another loophole that weakens the pill, if not rendering it virtually illusory. The structure of “ownership” would simply shift from standard equity to synthetic equity and the activist would achieve the same result while avoiding triggering the pill. For many of the same reasons, practitioners have highlighted inadequacies of Section 13D and pushed for expanding Section 13D to include derivative positions and other synthetic equity.57 Similarly, regulators in Canada are also concerned with the abuse of synthetic equity arrangements in takeover and activism contexts to circumvent applicable regulation, with a panel of the Alberta Securities Commission recently condemning a bidder’s failure to disclose its ownership of cash-settled total return swaps prior to its unsolicited takeover bid.58

The Delaware courts have not directly addressed synthetic equity in pill triggers, but some guidance can be distilled from the Delaware case law. For example, over a decade ago in 2008, would-be acquirors of the semiconductor company Atmel challenged the Atmel board’s decision to amend the company’s poison pill to include derivative instruments in its definition of beneficial ownership because the derivatives language was so vague.59 In a transcript decision, the Delaware Court of Chancery refused to preliminarily enjoin the pill on those grounds and the parties later settled.60 Similar derivative language was also included in the poison pill that the Delaware Court of Chancery upheld in Yucaipa, but the language was not directly at issue in the case.61 While Yucaipa seems to suggest that triggers should be based on the Section 13D of the Exchange Act definition of beneficial ownership,62 it remains unsettled in the courts whether beneficial ownership in poison pills encompasses derivatives.

3. Other Pill Features

While AIC provisions, daisy chains, and synthetic equity are the most important features for ensuring that a pill serves its intended purpose, pill chewability and “last look” provisions are also important in pill design. “Chewability” refers to the stockholders’ ability to decide whether or not to trigger the pill; if a pill is chewable, stockholders can vote to either cancel the pill or leave it in place. Most pills will set threshold requirements (qualifying offers) before the pill that requires the decision be submitted to a stockholder vote (e.g. a certain premium or proof of financing). However, if a pill is providing protection from substantive coercion,63 then a chewable pill that permits stockholders, who presumably hold an ignorant or mistaken belief, to cancel the pill, will be tainted by that mistaken belief and be rendered illusory. One way to reconcile the benefits of chewability against the costs of substantive coercion would be to determine a qualifying offer at a sufficiently high premium (say, a 30% premium over the 52-week-high) such that concerns about substantive coercion are minimal at best.

In addition, while many poison pills are drafted such that if a stockholder exceeds the triggering percentage the pill is automatically triggered without an additional action (and cannot be undone or reversed), some pills contain a “last look” provision. These provisions include a period, usually ten days, between their trigger date and the date the rights can be exercised, during which the board may amend the pill (e.g. to exempt a bidder or activist). The provisions are surprisingly common, with one study finding that slightly less than half of the poison pills adopted in a four-month period studied contained a last-look provision.64 While there is some debate on whether last-look provisions are beneficial to the company,65 these last-look provisions can likewise be problematic as they diminish the board’s bargaining power. On one hand, it puts the power of activating the pill back in the board’s hands (rather than the triggering stockholders’ hands), which may make sense given the significant impact a pill being triggered can have on the company’s capital structure and finances.66 But on the other hand, a poison pill loses its potency when it provides the option, and time, for the triggering stockholder (and other stockholders) to pressure the board. Thus, the board’s bargaining power is weakened when a triggering stockholder knows the board may be incentivized to negotiate and cancel the poison pill.67

IV. Conclusion

The world has changed in meaningful ways in the thirty years since Easterbrook and Fischel’s seminal work, with the rise of stakeholder governance, ESG, and stockholder activism. When increasingly sophisticated activists collaborate in subtle, implicit ways, or ESG-related corporate governance objectives and stockholder activism conflict, pills can play a critical role in protecting the corporation’s long-term value and preventing activist plays motivated by extracting value from other constituencies that today’s corporate governance world feels the need to preserve and promote. Our proposed ground rules for pills in the modern corporate landscape preserve the efficacy of pills and balance the board’s interest in considering a broad set of constituencies against the rights of all shareholders, including increasingly sophisticated activists, to solicit support for their ideas or attempt to gain corporate control.

- 1Shareholder rights plans are tools used to protect against a hostile takeover or shareholder activism. They work by diluting a shareholder’s stake once that shareholder crosses a certain threshold of ownership, known as the “trigger threshold.” The pill dilutes such shareholder by giving all other shareholders the right to buy additional stock in the target company, the acquiring company, or both, at a substantial discount (typically 50%).

- 2Frank H. Easterbrook & Daniel R. Fischel, The Economic Structure of Corporate Law (1991).

- 3Easterbrook and Fischel are not alone in their opposition to poison pills. Many institutional stockholders and proxy advisory firms such as Institutional Shareholder Services and Glass Lewis & Company generally oppose poison pills except in limited circumstances. See, e.g., Paul J. Shim, James E. Langston & Charles W. Allen, ISS and Glass Lewis Guidances on Poison Pills During COVID-19 Pandemic, Harv. L. Sch. F. on Corp. Governance (Apr. 26, 2020), https://perma.cc/64HH-DMTL. Critics of poison pills emphasize that a poison pill can prevent hostile takeovers at a premium, reduce management accountability, chill potential acquirors or activists, limit a stockholder’s ability to increase their ownership stake, and lower share price at the time of adoption. See, e.g., Aaron Bertinetti, Poison Pills and the Coronavirus: Understanding Glass Lewis’ Contextual Policy Approach, Glass Lewis (Apr. 8, 2020), https://perma.cc/X58S-TFG3 (“[T]hese provisions carry the potential to reduce management accountability by substantially limiting opportunities for corporate takeovers.”); Marcel Kahan & Edward B. Rock, How I Learned to Stop Worrying and Love the Pill: Adaptive Responses to Takeover Law, 69 U. Chi. L. Rev. 871, 876 (2002) (“[P]rominent legal scholars” have “painted in dark colors the world in which a ‘just say no’ [refusal to redeem a pill indefinitely] defense was valid.”); Jonathan R. Macey, The Legality and Utility of the Shareholder Rights Bylaw, 26 Hofstra L. Rev. 835, 837 (1998) (“Courts have become far too reluctant to second-guess directors who refuse to eliminate their firms’ pills. These courts are shirking their responsibility to safeguard shareholder value by failing to enforce fiduciary duties and by failing to police director and management conflicts of interest.”); Joseph A. Grundfest, Just Vote No: A Minimalist Strategy for Dealing with Barbarians Inside the Gates, 45 Stan. L. Rev. 857, 858 (1993) (A “remarkable transformation in the market for corporate control resulted from the emergence of the ‘poison pill’ as an effective antitakeover device.”); id. at 862–64 (“With the demise of the hostile takeover, shareholders can no longer expect much help from the capital markets in disciplining or removing inefficient managers. . . . As a result, corporate America is now governed by directors who are largely impervious to capital market or electoral challenges.”).

- 4Easterbrook & Fischel, supra note 2, at 171 (“Successful resistance frustrates the achievement of [social] gains. Consequently, managers should remain passive and let investors decide whether to tender.”); id. at 174 (“Managers should leave to shareholders and rival bidders the task of ‘responding’ to offers. Managerial passivity is best, ex ante, but privately and socially.”); see also, e.g., Frank H. Easterbrook & Daniel R. Fischel, The Proper Role of a Target’s Management in Responding to a Tender Offer, 94 Harv. L. Rev. 1161 (1981) [hereinafter Easterbrook & Fischel, The Proper Role] (arguing that investor and societal wealth is increased if the managers do not resist takeover bids or seek competing offers); Frank H. Easterbrook & Daniel R. Fischel, Auctions and Sunk Costs in Tender Offers, 35 Stan. L. Rev. 1, 1 (1982) [hereinafter Easterbrook & Fischel, Auctions and Sunk Costs] (“In most cases resistance reflects either mismanagement (to the extent it pointlessly denies shareholders the opportunity to obtain a premium) or manager’s self-protection (to the extent its point is to preserve managers’ jobs or ‘sell’ their acquiescence in exchange for bonuses or promises of future employment.)”); id. at 2 (“[A]ll defensive tactics, whether or not for the purpose of triggering an auction, reduce shareholders’ wealth.”); Ronald J. Gilson, Seeking Competitive Bids Versus Pure Passivity in Tender Offer Defense, 35 Stan. L. Rev. 51, 52 (1982) (“[T]here is no coherent justification for allowing target management to engage in defensive tactics that may deprive shareholders of the opportunity to tender their shares. . . . [C]ourts must recognize that the legal rules that facilitate this conduct, under the guise of deference to business judgment, do no more than sanction corporate treason.”).

- 5See Lucian Arye Bebchuk, The Case for Facilitating Competing Tender Offers: A Last (?) Reply, 2 J. L. Econ. & Org. 253 (1986); Easterbrook & Fischel, Auctions and Sunk Costs, supra note 4; Lucian A. Bebchuk, The Case for Facilitating Competing Tender Offers: A Reply and Extension, 35 Stan. L. Rev. 23 (1982); Lucian Arye Bebchuk, The Case for Facilitating Competing Tender Offers, 95 Harv. L. Rev. 1028, 1054 (1982); Gilson,  supra note 4; Ronald J. Gilson, A Structural Approach to Corporations: The Case Against Defensive Tactics in Tender Offers, 33 Stan. L. Rev. 819, 868–75 (1981); Easterbrook & Fischel, The Proper Role, supra note 4, at 1199–1204.

- 6Easterbrook & Fischel, supra note 2, at 181–83.

- 7See, e.g., Andrei Shleifer & Lawrence H. Summers, Breach of Trust in Hostile Takeovers, in Corporate Takeovers: Causes and Consequences (Alan J. Aurbach ed., 1988) (arguing that breach of implicit contracts can motivate hostile takeovers and such takeovers may be inefficient in the long run).

- 8Easterbrook & Fischel, supra note 2, at 182.

- 9See, e.g., Martin Lipton, Further on the Purpose of the Corporation, Harv. L. Sch. F. on Corp. Governance (July 20, 2021), https://perma.cc/SY5B-QXVK.

- 10In recent years, “ESG” is increasingly referred to as “EESG” in recognition of the importance of employees, as well as environmental, social, and governance factors. See, e.g., Leo E. Strine, Jr., Toward Fair and Sustainable Capitalism 6 (Roosevelt Inst., Working Paper No. 202008, 2020), https://perma.cc/5H93-HKDA. However, “ESG” remains the more prominent acronym and will be used within this paper.

- 11Russ Banham, Board Action on ESG Needed to Ensure Long-Term Performance Gains, Forbes (Dec. 10, 2019), https://perma.cc/E9T9-R9A6 (“[ESG interests] demand diligent board-of-director oversight; otherwise, an ESG-related failure may result in consumer boycotts, employee walkouts, and adverse proxy votes by institutional investors at annual meetings. By effectively overseeing ESG risks, boards also help ensure that governance practices within the companies they serve are aligned with the long-term sustainability of the business.”).

- 12PwC’s 2021 Annual Corporate Directors Survey, PwC, https://perma.cc/4YS7-246K (last visited Feb. 7, 2022).

- 13Jamie Smith, Four Opportunities for Enhancing ESG Oversight, Ernst & Young (June 29, 2021), https://perma.cc/M6BK-PZ65 (noting that 82% of boards discuss ESG as part of board composition, refreshment, and evaluation discussions and nearly 60% of companies report ESG information externally); see PwC’s 2021 Annual Corporate Directors Survey, supra note 12 (finding that 64% of directors say ESG is linked to company strategy); Caroline Davis Schonecker & Bob Lamm, Boards Face Rising Complexity of ESG Oversight Role, Deloitte (Nov. 17, 2021), https://perma.cc/TP5D-RSQR. But see Tensie Whelan, Boards Are Obstructing ESG—at Their Own Peril, Harv. Bus. Rev. (Jan. 18, 2021), https://perma.cc/8G6U-UVNQ (arguing that while “[a]sset owners, asset managers and even many chief executives now consider ESG issues essential for financial performance . . . corporate directors are lagging” and emphasizing that “only 38% of board members think ESG issues have a financial impact on a company”).

- 14Peter Reali, Jennifer Grzech & Anthony Garcia, Nuveen, ESG: Investors Increasingly Seek Accountability and Outcomes, Harv. L. Sch. F. on Corp. Governance (Apr. 25, 2021), https://perma.cc/GD5U-M3VX.

- 15See Banham, supra note 11. In addition, board audit committees are increasingly considering ESG oversight part of their risk and regulatory compliance activities. Id.

- 16See, e.g., Martin Lipton, Steven A. Rosenblum & William Savitt, A Framework for Management and Board of Directors Consideration of ESG and Stakeholder Governance, Harv. L. Sch. F. on Corp. Governance (June 5, 2020), https://perma.cc/D245-652Y; Business Roundtable Redefines the Purpose of a Corporation to Promote ‘An Economy That Serves All Americans,’ Bus. Roundtable (Aug. 19, 2019), https://perma.cc/S2TS-2Y9U (embracing ESG-factors). But see, e.g., Lucian A. Bebchuk & Roberto Tallarita, The Illusory Promise of Stakeholder Governance, 106 Cornell L. Rev. 91 (2020).

- 17See Shareholder Activism in 2021, Activist Insight at 4 (Jan. 2022), https://perma.cc/7ZLB-229V; Activist Investing, Activist Insight at 9 (2015), https://perma.cc/2N7B-FHHT.

- 18For a report on recent shareholder activism trends, see generally 2021 Review of Shareholder Activism, Lazard (Jan. 2022), https://perma.cc/6KGP-W8RW (noting that an average of 193 activist campaigns were initiated in each of the past four years).

- 19See, e.g., Zohar Goshen & Reilly S. Steel, Raiders, Activists, and the Risk of Mistargeting (European Corp. Governance Inst., Law Working Paper No. 613/2021, 2021) (arguing that activists are more likely than raiders to destroy social wealth through “mistargeting,” resulting in harm to other stockholders and the economy), https://ssrn.com/abstract=3945764; Lucian A. Bebchuk, Alon Brav & Wei Jiang, The Long-Term Effects of Hedge Fund Activism, 115 Colum. L. Rev. 1085 (2015) (finding no evidence that interventions by activist hedge funds boost short-term value at the expense of-long term value); Zohar Goshen & Richard Squire, Principal Costs: A New Theory for Corporate Law and Governance, 117 Colum. L. Rev. 767, 822 (2017) (“[A]ctivist campaigns could generate both positive and negative externalities.”); Ronald J. Gilson & Jeffrey N. Gordon, The Agency Costs of Agency Capitalism: Activist Investors and the Revaluation of Governance Rights, 113 Colum. L. Rev. 863, 892 (2013).

- 20See Marcel Kahan & Edward Rock, Anti-Activist Poison Pills, 99 B.U. L. Rev. 915, 919-20 (2019) (“In takeovers, the bidder’s primary gains are expected to come from acquiring the company and improving it. As a result, bidders neither need to nor, it turns out in fact, do buy substantial blocs of shares before they acquire a company . . . . By contrast, today’s activists generally expect to profit from an increase in the value of their stakes in the target that they hope to result from significant operational changes, increased dividends, asset sales, or the sale of the company.); id. at 920 (“For activists, pill features that affect the size of their stake are thus of the utmost importance.”)

- 21See, e.g., Williams Cos. S’holder Litig., No. CV 2020–0707–KSJM, 2021 WL 754593, at *29 (Del. Ch. Feb. 26, 2021), aff’d sub nom. Williams Cos. v. Wolosky, No. 131, 2021, 2021 WL 5112495 (Del. Nov. 3, 2021) (“More recently, ‘ESG activism’ has come to the fore, and stockholders have begun pressuring corporations to adopt or modify policies to accomplish environmental, social, and governance goals.”).

- 22See, e.g., Andrew R. Brownstein, Steven A. Rosenblum & Trevor S. Norwitz, The ESG/TSR Activist “Pincer Attack,” Harv. L. Sch. F. on Corp. Governance (Jan. 26, 2021), https://perma.cc/SU2Y-DZA8.

- 23Numerous practitioners, managers, executives, and judges have highlighted the concern that activists induce managers to pursue short-term financial goals at the expense of long-term value. See, e.g., Kahan & Rock, supra note 20, at 918–19, 930–33. Politicians have also become involved with the problems that can arise due to activist shareholders, with Senators Bernie Sanders and Elizabeth Warren co-sponsoring the Brokaw Act (named for a small town that went bankrupt after a paper mill targeted by activist hedge funds closed) to “increase transparency and strengthen oversight of activist hedge funds.” See Portia Crowe, Bernie Sanders and Elizabeth Warren Are Going After Activist Hedge Funds, Bus. Insider (Mar. 18, 2016, 9:08 AM), https://perma.cc/Y6A4-52KV; Michael R. Levin, The Mystery of the Brokaw Act, Activist Blog (May 17, 2016), https://perma.cc/DVH9-LBB9 (explaining that the plant in Brokaw was obsolete and that after being targeted by the activist, the company closed several plants and was eventually sold). But see Alon Brav, J.B. Heaton & Jonathan Zandberg, Failed Anti-Activist Legislation: The Curious Case of the Brokaw Act, 11 J. Bus. Entrepreneurship & L. 329, 342 (2018) (arguing that activists played no role in the plant closing). In some cases, shareholders may even launch anti-ESG campaigns. See Liz Dunshee, An Anti-ESG Campaign Begins, TheCorporateCounsel.net (May 25, 2018), https://perma.cc/5HEN-5FA5; Leading National Associations Announce Launch of First-of-Its-Kind Investor Coalition, PR Newswire (May 22, 2018, 9:00 ET), https://perma.cc/X2NH-25HJ.

- 24Kahan & Rock, supra note 20, at 923.

- 25See 2021 Review of Shareholder Activism, supra note 18, at 16.

- 26As an illustrative example, at one point, over 3,000 companies and 60% of the S&P 500 had adopted a poison pill. See Wachtell, Lipton, Rosen & Katz, Takeover Law and Practice Guide 2020, at 122 (Oct. 2020), https://perma.cc/U634-WPWN (relying on data from FactSet). As of December 31, 2019, only 160 U.S. companies and 1% of the S&P 500 had a poison pill in effect. Id.

- 27A 15% triggering percentage corresponds with the ownership percentage that would cause a stockholder to be an “interested stockholder” under Delaware’s anti-takeover statute, and thus has already been endorsed by the Delaware legislature as a sufficient threat to trigger Delaware’s anti-takeover statute. Del. Code Ann. tit. 8, § 203 (2019).

- 28Kahan & Rock, supra note 20, at 956–57. Even a small percentage of equity investment can result in a significant amount of equity investment depending on the market capitalization. For example, “[g]iven Williams’ market capitalization in March 2020, triggering the 5% threshold at the time the Plan was adopted would have required an economic investment (sometimes referred to as a ‘toehold’) of approximately $650 million.” Williams Cos. S’holder Litig., 2021 WL 754593, at *10.

- 29See Kahan & Rock, supra note 20, at 956–57 (noting that costs include the costs of developing an alternative strategy, legal expenses, the costs of writing a proxy statement, and campaign expenditures).

- 30Id. While toeholds are important for activists, they are largely irrelevant for bidders. Id. at 922–23 (noting that “in modern takeover practice, bidders rarely acquire substantial pre-bid toeholds” and finding that of the twenty-four hostile proposed takeovers between 2010 and 2015, the bidder acquired a stake close to the pill threshold in only five instances).

- 31La. Mun. Police Emps.’ Ret. Sys. v. Crawford, 918 A.2d 1172, 1181 n.10 (Del. Ch. 2007) (noting that while “a ‘3% rule’ for termination fees might be convenient for transaction planners, it is simply too blunt an instrument, too subject to abuse, for this Court to bless as a blanket rule”); In re Cogent, Inc. S’holder Litig., 7 A.3d 487, 503 (Del. Ch. 2010) (noting that when evaluating the reasonableness of the size of a termination fee, “the reasonableness of such a fee depends on the particular facts surrounding the transaction”) (citation and internal quotation omitted).

- 32See Fernán Restrepo & Guhan Subramanian, The New Look of Deal Protection, 69 Stan. L. Rev. 1013 (2017); see also, e.g., In re Answers Corp. S’holders Litig., No. CIV. A. 6170–VCN, 2011 WL 1366780, at *4 & n.52 (Del. Ch. Apr. 11, 2011) (finding that the median termination fee as a percentage of transaction value decreases as the transaction size increases and describing a termination fee of 4.4% of equity value as “near the upper end of a ‘conventionally accepted’ range”); David Fox, Breakup Fees—Picking Your Number, Harv. L. Sch. F. on Corp. Governance (Sept. 11, 2021), https://perma.cc/SF9D-77ZE (“Studies have also shown that, as deal size goes up, fees, measured on a percentage basis, tend to go down.”); In re Topps Co. S’holders Litig., 926 A.2d 58, 86 (Del. Ch. 2007) (upholding a 4.3% termination fee but calling it “a bit high in percentage terms”); Phelps Dodge Corp. v. Cyprus Amax Minerals Co., No. CIV.A. 17398, 1999 WL 1054255, at *2 (Del. Ch. Sept. 27, 1999) (criticizing a 6.3% fee as “seem[ing] to stretch the definition of range of reasonableness . . . beyond its breaking point”); see also William T. Allen, Reinier Kraakman & Guhan Subramanian, Commentaries and Cases on the Law of Business Organization, 575 & n. 54 (4th ed. 2012) (“Lump-sum termination payments no larger than 3 to 4 percent of the deal price are easily rationalized as a means to assure that a would-be acquirer will recover its transaction expenses (including opportunity costs) if the favored contract does not close. There have been indications, however, that courts will question the bona fides of amounts beyond a certain range (perhaps 4 to 5 percent of the deal price).”).

- 33See Williams Cos. S’holder Litig., 2021 WL 754593, at *33 (“Lightning strikes go undetected under the federal disclosure regime, which requires stockholders to disclose their ownership position after crossing the 5% threshold but gives stockholders ten days to do so.”). Recently, the SEC proposed amendments to the reporting requirements for such beneficial owners, which would accelerate the deadline for filing a Schedule 13D from ten calendar days after the triggering event to five calendar days. See Modernization of Beneficial Ownership Reporting, 87 Fed. Reg. 13,846 (Mar. 10, 2022) (to be codified at 17 C.F.R. pts. 232, 240).

- 34See Yucaipa Am. All. Fund II, L.P. v. Riggio, 1 A.3d 310, 329–30 (Del. Ch. 2010) (upholding a poison pill that grandfathered in an existing stockholder as a reasonable and proportional response to a threat), aff’d, 15 A.3d 218 (Del. 2011); Third Point LLC v. Ruprecht, No. CIV.A. 9469–VCP, 2014 WL 1922029 (Del. Ch. May 2, 2014) (endorsing a pill that imposed a 20% triggering percentage on passive investors and a 10% triggering percentage on others).

- 35See Kahan & Rock, supra note 20, at 957–59.

- 36See id. at 959–61.

- 37Mara Elyse Goodman, Spencer Klein, Michael O’Bryan & Joseph Sulzbach, 2020 Poison Pill Recap and Current Trends, JDSupra (Feb. 25, 2021), https://perma.cc/R43E-57W4.

- 38See Household Int’l, Inc. & Harris Tr. & Sav. Bank, Rights Agreement (Aug. 14, 1984), in Penn. L. Del. Corp. L. Res. Ctr. § 1(c), https://perma.cc/F2GR-B5E2 (“A person shall be deemed the ‘Beneficial Owner’ of any securities . . . which are beneficially owned . . . by any other Person with which such Person or any of such Person’s Affiliates or Associates has any agreement, arrangement or understanding for the purpose of acquiring, holding, voting or disposing of any securities of the Company.”).

- 39See, e.g., 15 U.S.C. § 18(a) (imposing a constraint on activist shareholders’ trading under the HSR Act if it exceeds a certain monetary threshold); see also 15 U.S.C. § 78m; 17 C.F.R. § 240.12b–2.

- 40Delaware courts have generally upheld this approach. See, e.g., Stahl v. Apple Bancorp, No. CIV. A. 11510, 1990 WL 114222 (Del. Ch. Aug. 9, 1990).

- 41“Wolf packs” are a feature of modern pills, and the term is often used to refer to “a loose association of hedge funds that employs parallel activist strategies toward a target corporation while intentionally avoiding group status under section 13(d).” William R. Tevlin, The Conscious Parallelism of Wolf Packs: Applying the Antitrust Conspiracy Framework to Section 13(D) Activist Group Formation, 84 Fordham L. Rev. 2335, 2337 (2016).

- 42See, e.g., Williams Cos. S’holder Litig., No. CV 2020–0707–KSJM, 2021 WL 754593, at *10 (Del. Ch. Feb. 26, 2021), aff’d sub nom. Williams Cos. v. Wolosky, No. 131, 2021, 2021 WL 5112495 (Del. Nov. 3, 2021).

- 43Id.

- 44Modernization of Beneficial Ownership Reporting, 87 Fed. Reg. 13,846, 13,868–13,869 (Mar. 10, 2022) (to be codified at 17 C.F.R. pts. 232, 240). See id. (discussing proposed rules 13d-5(b)(1)(i) and (b)(2)(i)).

- 45See Guhan Subramanian, Bargaining in the Shadow of PeopleSoft’s (Defective) Poison Pill, 12 Harv. Negot. L. Rev. 41, 45, 55, 65 (2007).

- 46The Sample excluded two companies that were identified in the RiskMetrics database but did not have their rights agreements readily available to the public (MGM Holdings, Inc. and KS Bancorp, Inc.).

- 47Williams Cos. S’holder Litig., 2021 WL 754593.

- 48Id. at *1.

- 49Id.

- 50Indeed, the Williams court placed great emphasis on both the 5% trigger and the AIC provision. See, e.g., id. at *35 (“[T]he 5% trigger alone distinguished the Plan; only 2% of all plans . . . had a trigger below 10%.”); id. at *37 (“Although the 5% trigger is a marked departure from market norms, it is not the most problematic aspect of the Plan . . . . The primary offender is the AIC provision”). Practitioners perhaps similarly over-reacted to the Delaware Supreme Court’s decision in Paramount Commc’ns, Inc. v. QVC Network, Inc., moving significantly away from stock option lockups and toward breakup fees, even though the Court rejected the specific stock option lockup in that case and not stock option lockups more generally. See John C. Coates IV & Guhan Subramanian, A Buy-Side Model of M&A Lockups: Theory & Evidence, 53 Stan. L. Rev. 307, 331–32 (2000).

- 51See, e.g., Williams Cos. S’holder Litig., 2021 WL 754593, at *11 (invalidating a pill with a 5% trigger and a parallel-conduct + guardrails AIC provision); In re Versum Materials, Inc. S’holder Litig., Consolidated C.A. No. 2019–0206–JTL (Del. Ch. July 16, 2020) (transcript), aff’d, No. 266, 2020, 2021 WL 755096 (Del. Feb. 22, 2021) (awarding the plaintiff $12 million in fees and expressing concern with the “truly expansive” acting in concert clause at issue). But see Yucaipa Am. All. Fund II, L.P. v. Riggio, 1 A.3d 310, 332, 359 (Del. Ch. 2010), aff’d, 15 A.3d 218 (Del. 2011) (upholding a poison pill’s prohibition on “acting in concert,” noting that the key inquiry is whether the pill “fundamentally restricts” a successful proxy contest); see also Frank Aquila & Melissa Sawyer, Perfect Pill, Imperfect Defense, 47 Rev. Sec. & Commodities Reg. 231, 234–35 (2014) (“[D]rafters should take care that a ‘stockholders acting in concert’ provision does not unduly interfere with the valid exercise of shareholder rights, such as the right to meet and to communicate with other shareholders.”).

- 52We recognize that this analogy might be provocative if read to suggest that activists are like COVID-19. We discourage any such inference. Our review of the academic literature suggests to us that activists can be forces for good or bad, unlike COVID-19.

- 53See, e.g., Williams Cos. S’holder Litig., 2021 WL 754593, at *11.

- 54See Sam Ro, Synthetic Equity: A Way to Buy Stocks Without Buying Stocks, Bus. Insider (Sept. 18, 2011, 12:13 PM), https://perma.cc/RA8K-BMZ6. One study by Latham and Watkins found that 76% of all pills adopted or amended in 2013 included such provisions. Mark D. Gerstein et al., Latham & Watkins, The Resilient Rights Plan: Recent Poison Pill Developments and Trends 7 (2014), https://perma.cc/U5V9-XAZU (“Seventy-six percent of all traditional rights plans adopted or amended in 2013 contained provisions including synthetic equity positions.”).

- 55Some forms of synthetic equity, such as options exercisable for stock, are even included in the ownership definition of Section 203 of the Delaware General Corporation Law. Del. Code Ann. tit. 8, § 203(c)(9) (2019) (defining “owner” as one who beneficially owns stock and has “the right to acquire such stock . . . pursuant to any agreement, arrangement or understanding, or upon the exercise of conversion rights, exchange rights, warrants or options”). But see Kahan & Rock, supra note 20, at 948–53 (arguing that “[b]ecause synthetic equity entails no voting rights, it does not create threats that justify a pill in principle”). For a discussion of “hidden” or morphable ownership, see, e.g., Henry T.C. Hu & Bernard Black, The New Vote Buying: Empty Voting and Hidden (Morphable) Ownership, 79 S. Cal. L. Rev. 811, 836–40 (2006).

- 56Williams Cos. S’holder Litig., 2021 WL 754593, at *10, *35 (“The Plan’s definition of ‘beneficial ownership’ starts with the definition found in Rule 13d–3 of the Exchange Act, then extends more broadly to include ‘[c]ertain synthetic interests in securities created by derivative positions,’ such as warrants and options.”) (alteration in original).

- 57See David A. Katz & Laura A. McIntosh, 13(d) Reporting Inadequacies in an Era of Speed and Innovation, 254 N.Y. L.J. 5 (Sept. 24, 2015) (“Decoupling arrangements can lead to ‘empty voting,’ in which an investor holds voting rights in excess of their economic interest, and ‘morphable ownership,’ in which an investor holds economic interest in excess of formal voting rights but has the ability to transform the economic position into a traditional ownership position.”). But see Gilson & Gordon, supra note 19, at 915 (arguing that synthetic equity should not count towards beneficial ownership under Section 13D and suggesting the SEC define “beneficial ownership” more narrowly “to exclude a total return swap that has been ‘sterilized’ through a mirrored voting commitment with respect to any proposal or proxy contest by the activist counterparty”). Additionally, it is unclear whether stockholders must disclose the ownership of derivative instruments or synthetic equity under federal securities law reporting requirements. See CSX Corp. v. The Children’s Inv. Fund Mgmt. (UK) LLP, 654 F.3d 276 (2d Cir. 2011).

- 58Re Bison Acquisition Corp., 2021 ABASC 188 (Can. Alta. Sec. Comm’n), https://perma.cc/W8D5-NKHM (finding that bidder did not meet its disclosure obligations under National Instrument 62-104 – Take-Over Bids and Issuer Bids (NI 62-104) and that the bidder’s decision to not publicly disclose its increased economic exposure through the swaps triggered the Alberta Securities Commission’s public interest jurisdiction).

- 59Atmel Corp. S’holders Litig., C.A. No. 4161–CC (Del. Ch. May 19, 2009) (transcript).

- 60Id.

- 61Yucaipa Am. All. Fund II, L.P. v. Riggio, 1 A.3d 310 (Del. Ch. 2010), aff’d, 15 A.3d 218 (Del. 2011).

- 62See id. at 341–42.

- 63See discussion infra Section III.B.

- 64Spencer D. Klein et al., Poison Pill Deep Dive Series: Last Look, Morrison & Foerster (June 25, 2020), https://perma.cc/JCN8-H7MM.

- 65See id.

- 66See Subramanian, supra note 45, at 45, 55.

- 67In response to Elon Musk’s offer to buy the company in March 2022, the Twitter board of directors adopted a poison pill with just such a last look provision. Given Mr. Musk’s penchant for unorthodox behavior, it is possible that he would have deliberately triggered the pill and then (effectively) dared the Twitter board to permit the dilution. During the ten-day window between Mr. Musk’s trigger event and the warrant distribution date, Mr. Musk would have had the power to exert (and encourage others to exert) tremendous influence on the Twitter board, including through his 90 million followers on Twitter. More likely, in our view, the Twitter board would have caved at that point and negotiated a friendly deal with Mr. Musk. Even in the worst case where the Twitter board permitted the dilution to occur, we calculate that the dilution would have cost Mr. Musk either $2.7 billion (if the Twitter board utilized the flip-in feature to effectuate the dilution) or $2.8 billion (if the Twitter board utilized the exchange feature) (calculations on file with authors). This would have been a large loss to almost anyone other than Mr. Musk. In our opinion, the last look feature of the Twitter pill was a defect, particularly in view of the fact that the Twitter board installed it to defend against the specific threat of a tender offer from Elon Musk. Of course, none of these issues have materialized as of the time of this publication.