Political Freedom and Economic Constraints: The Political Setting for the Problem of Twelve

This essay outlines foundations of the current moment facing corporations and politics, which I have characterized as a new “problem of twelve”—that is, the concentration of power in the hands of a small number of index and private equity fund sponsors.1 Through the middle of the twentieth century, public companies dominated the U.S. economy and government. They owed their dominance to having been socially legitimated coming out of the Great Depression, a legitimation built on their affirmative war efforts and on the negative constraints of securities law, progressive taxation, labor unions, and operational regulation. From 1970 on, however, they changed and were dramatically changed by politics and economics. American corporate leaders used politics to liquidate most of their New Deal constraints, simplifying governance of public companies, only to face a new political constraint in the form of the institutional investors, and new economic constraints in the form of globalization, automation and the “technology” of hostile takeovers and private equity.

How did corporations shake off their New Deal political constraints? Corporate leaders invested in their own political capital and applied the resulting power to roll back antitrust law, taxation and regulation. Most importantly, they laid low their most powerful political rival—private sector labor unions. As they achieved political victories, however, public companies’ autonomy in fact dramatically shrank. Indeed, they faced an existential crisis – in the form of globalization, inflation, automation, hostile takeovers, and LBOs (i.e., private equity). Since 1990, they have also faced an ongoing challenge in the form of a “shareholder rights movement,” in which institutional investors organized politically, first by public pension funds and hedge funds, and lately increasingly by index funds. Meanwhile, private equity, which seemed to diminish in the recession of 1989–91, has more than recovered and has been growing much faster than public equity markets, displacing public companies in both the economy and the political system.

This combination of “liberated” corporate power re-constrained by markets and shareholders sets the stage for the current politics of the “problem of twelve” created by the ongoing growth and concentration of index and private equity funds. If corporations had not been politically “liberated” from 1970 on, the influence of index and private equity funds would be less important to the political system and to the economy. If companies had not faced the whirlwind of global capitalism and the technology shocks it ushered in, choices in how they were governed would not have had such dramatic implications for the economy and polity. If institutional shareholders had not developed the standard suite of powers they use to influence companies—policy formation and coordination, lobbying, shareholder resolutions, and more in-the-weeds but crucial governance tools such as majority vote bylaws—the ability of index funds to influence companies would be significantly weaker. If labor had not been decapitated as a political force, the ability of private equity fund lobbying to eliminate the remaining New Deal constraints on their growth would likely not have been successful. If companies had not become the core not only of the U.S. economy but of its political economy, the stakes for how investment funds are governed would be lower.

With this context, it can be better understood why index and private equity funds are increasingly perceived as – and indeed often are – politically active and influential. It also becomes more understandable why other political actors – civil society organizations, social activists, political parties and politicians – have responded and are continuing to respond to these funds’ growing economic clout and political power. Without the backstory, it would be hard to understand how an application of one essence aspect of capitalism—finance—has increasingly attracted political focus on topics such as diversity, treatment of workers, and climate change. Asset managers now draw charges of “socialism” from the right, and charges of antitrust harm and of foot-dragging on other salient issues, such as corporate political disclosure, from the left.

I. The Legitimation of Berle-and-Means Companies in the New Deal and World War II

Going into the Great Depression, the U.S. economy was dominated by large public companies, famously diagnosed by Adolf Berle and Gardiner Means as illegitimate and unaccountable, serving neither social ends nor even the private interests of their owners.2 Coupled with the Crash of ‘29 and the revelations of the Pecora Hearings,3 U.S. capitalism and the corporations that dominated it were placed in serious political jeopardy. Ever fewer people brought themselves to defend a system that provided weak political accountability and poor economic performance alike.4

How did privately owned, publicly traded corporations come to re-acquire legitimacy and be seen as essential and beneficial, serving “all society,” as they largely did for much of the second half of the twentieth century? The legitimacy achieved by public companies was built on three foundations: (1) disclosure, (2) political constraints, and (3) contributions to U.S. military power. Franklin Roosevelt embraced a regime of “full and fair disclosure” in 1933, and in 1934 with the creation of the Securities and Exchange Commission (SEC). The SEC enacted and enforced rules for public companies—requiring them to publish annual reports, pay for independent audits, and follow rules for how dispersed shareholders could vote for directors.

More broadly, the New Deal layered multiple constraints on private business. Congress passed the Fair Labor Standards Act of 1938,5 overriding business resistance and lawyers who idealized the largely imaginary “freedom” of an agrarian economy long lost to urban industrialization. Unions gained power, pushed up wages, and eventually their own legitimacy, with legal recognition in the National Labor Relations Act of 1935 and supervision by the National Labor Relations Board.6 Federal supervision and regulation of entire industries tightened or emerged – from banking to airlines to trucking.7 Antitrust laws were augmented and enforced with greater vigor.8 Wealth was redistributed through Depression-era programs such as the Agricultural Adjustment Act (AAA) and the Civilian Conservation Corps (CCC),9 and social welfare programs such as Social Security.10 Wealth was also redistributed downward through the progressive income tax, which steadily mounted, peaking at 92% for individuals and 50% for corporations under President Eisenhower.11

More affirmatively, large public companies powered the “arsenal of democracy” during World War II and the Cold War that followed.12 Public companies “converted” to quasi-state actors through active, coordinated participation in the war effort: General Motors became the largest defense contractor on the planet,13 while producing only 139 new ordinary cars during the war;14 Ford and Alcoa produced jeeps and airplanes,15 and Chrysler built tanks and airplanes.16 During World War II itself, unions were kept in check by the tightly concentrated War Planning Board and Office of Production Management – the birthplace of the “military-industrial complex.”17 But the economic effects of the war and its aftermath were (as with World War I) to massively redistribute wealth downward, earning the period the moniker the “Great Compression.”18

(Not all U.S. public companies’ activities aided the U.S. Standard Oil of New Jersey actively conspired with I.G. Farben and the Nazi regime and pled “no contest” to criminal charges in 1942.19 “Sullivan & Cromwell floated bonds for Krupp A.G., the arms manufacturer, and also worked for I. G. Farben, the chemicals conglomerate that later manufactured Zyklon B, the gas used to murder millions of Jews.”20 Fred C. Koch, founder of what became Koch Industries, profited from managing the construction of a major oil refining facility in Hamburg, Germany in 1934.21 Chase Bank derived massive revenue from Nazis in occupied Paris even after Pearl Harbor.22 As late as 1944, ITT was supplying “switchboards, telephones, alarm gongs, buoys, air raid warning devices, radar equipment, and thirty thousand fuses per month for artillery shells used to kill British and American troops.”23 News about business support for the Third Reich, however, was largely suppressed and did not undermine the improvement in the image of public companies overall.)

An unappreciated effect of war was the creation of the “venture capital” industry. Nominally private but heavily subsidized by defense contracts, venture capital transformed an area touted in 1950 as “the Prune Capital of America” into what is now globally famous as “Silicon Valley,” and went on to make massive investments in technology and production, creating such public companies as Hewlett-Packard, Intel and Apple.24 Victorious in war and relatively magnanimous to Germany and Japan due to the need to create stable allies against the Soviet Union, the U.S. enjoyed a sustained period of global acclaim, industrial growth and geopolitical clout as militarily victorious liberators. The reputation of public companies grew along with the American economy.25

A final component of public company legitimation was ethical, normative and ideological. Under labels such as “corporate social responsibility” (CSR), business leaders and academics advanced a vision of an elite set of autonomous corporate managers who would wield corporate power in the public interest. Writing somewhat skeptically in 1950, Peter Drucker asked if public companies could form the basis of a “new society,” noting corporate managers’ promises to “manage their companies in the best balanced interest of shareholders, employees, consumers, suppliers, plant-cities and the economy and society as a whole.”26 Boards of directors were encouraged to think of themselves as stewards of social welfare. Instead of seeing the managerial autonomy critiqued by Berle and Means as a problem, the CSR movement celebrated it as the basis for an effective blend of market forces and long-term organizational planning, which would encourage research, innovation, and economic growth. Companies should be good citizens, according to this ideology, donating to charities, providing benefits such as pensions and health care to their employees, and investing in community development.

II. The Shift From Political to Investor Constraints on Berle-and-Means Companies

From the high point of public company legitimacy in the middle of the twentieth century, two late-century developments reshaped U.S. political economy. First, businesses intensified their organized political engagements, with more powerful and coordinated lobbying organizations, expanding the social reach of public companies through the liquidation of the labor movement, tax cuts, the reduction of antitrust enforcement, and the spread of the deregulatory movement. Second, globalization and automation led to economic underperformance and strong shifts from managerial autonomy towards investor power, fueled by the financial technologies of hostile takeovers, hedge funds, and leveraged buyouts and by the political organization of institutional investors, especially pension funds. An unintended consequence of businesses’ political efforts amid economic headwinds was to reduce its political legitimacy. Together, these developments cleared space for the rise of index and private equity funds, and the current moment of political controversy surrounding their role in American society.

A. The Rise of Business Lobbies

At the height of public respectability in the 1950s and 1960s, leaders of Berle-and-Means companies undertook to shake off constraints that had helped create that legitimacy out of the Depression. Large businesses pushed into politics as never before, renewing and expanding their resistance to labor, taxation and regulation, while fighting the civil rights movement, environmentalism, the consumer movement, and feminism. By 1990, business had rolled back antitrust, taxes and regulations from Nixon-era peaks and triumphed over unions. These successes, ironically, have coincided with and likely been a contributing factor to the reduced legitimacy of business in the eyes of the public.

i. The Stimulus of the 1960s

That the modern business lobby got going in full sail in the late ‘60s is not an accident. The unrest of that decade, largely born out of reactions to government-backed de jure racism in the South and the government’s decision to extend covert and brief Cold War operations in the Philippines, Indonesia, Iran and Guatemala to an open and prolonged war in Vietnam, was also in part a set of responses to exercises of corporate power, past and present. The results unsettled America’s corporate leaders, helping to push them more aggressively into the politics of race, war, environmental degradation, consumer harm and women’s rights. Contributing were the inflation spike in 1969 and 1970 and President Nixon’s embrace of government control of prices, viewed as among the greatest governmental interventions in private markets in U.S. history.27

Big business had a significant role in building a foundation for Jim Crow laws and institutionalized racism. Plessy v. Ferguson, which had enshrined “separate but equal” for sixty years, concerned a railroad and its racial discrimination. The civil rights movement of the late ‘50 and early ‘60s challenged corporate racism as much as segregation in Southern schools. Title II of the Civil Rights Act of 1964 banned race discrimination in “public accommodations”—meaning privately owned hotels, bus companies, restaurants, and any other businesses serving the public generally. Title VII did the same for employment by all businesses with 15 or more employees.

It was the military-industrial complex and large defense companies intertwined with the war in Vietnam that lost the varnish of victory from World War II, which had helped hide the collateral damage and inevitably compromised morality of war. The deadly egalitarianism of the draft unified youth across class and race more broadly than any war before or since. The rising threat of the Cold War to the survival of the human species generate massive profits for Lockheed, Boeing, Raytheon, Northrop Grumman, General Dynamics, and a long list of suppliers. Peace protesters portrayed Dow Chemical as a greater enemy than the Viet Cong.

It was American chemical companies and the massive harms they had imposed on unwitting victims that were at the center of Rachel Carson’s 1962 book Silent Spring, and the environmental movement it helped stimulate. Even Richard Nixon became sufficiently alienated by chemical leaks, toxic products, and corporate smokestacks to create the EPA by executive order in 1970.

It was the Chevrolet Corvair at the center of 1965’s Unsafe at Any Speed. Ralph Nader and his followers attacked both government agencies such as the FTC but also the businesses those agencies were failing to regulate adequately. Feminism further challenged corporate hierarchies, which were in the 1960s almost entirely male. The National Organization of Women, founded in 1966 and an early endorser of the Equal Rights Amendment, was fiercely resisted by the John Birch Society, the founding members of which were business leaders, including Harry Bradley, co-founder of the Allen Bradley Co., Fred Koch, founder of Koch Industries, and Robert Stoddard, president of Wyman-Gordon.

ii. The Powell Memo as a Roadmap for Business Political Organization

The protests, successes and failed efforts of the new left stimulated many reactions, among them a new surge of political organization and action by large U.S. companies. Illustrative is the then-secret, now-infamous 1971 memo written for the U.S. Chamber of Commerce by Lewis Powell—before he went on the Supreme Court.28 After a corporate law practice representing and joining corporate boards, Powell’s memo represented a deliberate move to bring corporations, politics and his own career into rewarding alignment.

Powell’s memo was—it is hard to characterize it otherwise—a neo-fascist mix of vitriolic anti-socialism and bureaucratically banal project management. As noted by Sheldon Whitehouse in a 2021 speech, Powell peppered his memo with phrases such as “shotgun attack,” “frontal assault,” “rifle shots,” and “warfare.”29 Its goal was to end “compromise” and “appeasement” and to mobilize “the resources of American business to be marshaled against those who would destroy it.’’

As threats Powell pointed to Ralph Nader (the “single most effective antagonist of American business”) for his opposition to mass consumer torts, Charles Reich—formerly at Cravath Swaine & Moore, author of a best-selling critique of the culture of corporate America in the 1950s—and William Kunstler, then recently of Chicago Seven fame. Sourcing via an op ed by William F. Buckley, Powell attributes to Kunstler advocacy of “revolt” with “guns” against “property owners,” and blames him for arson and bombings of Bank of America branches in 1970. Quoting Milton Friedman, Powell attacked academia, the media, and the “pulpit” for critiquing capitalism and supporting socialism.

Against such threats, Power argued that corporate America should be ready to deploy “whatever degree of pressure—publicly and privately—may be necessary.” Powell advocated for business generally and the Chamber of Commerce in particular to undertake a broad, multi-channel effort at mobilizing corporations and their resources to defend the “free enterprise system” in politics and public relations. Such a movement was needed, Powell asserted, to defend corporate America against such radical ideas as “consumerism” and “environmentalism” (the “scare quotes” on those words were Powell’s). To pursue those ends, American businesses, he wrote, should spend 10% of their total advertising budgets on propaganda written by scholars and speakers in academia and elsewhere. Business schools, he argued, should be used as vehicles for business propaganda. As outlined below, business generally followed his advice, and the “counter-intellegentsia” they created remains an important part of U.S. politics and policy making today.

A most important channel for change, he argued, was the legal system, both lobbying for legislation and litigating in court. “Under our constitutional system,” he wrote, “especially with an activist-minded Supreme Court, the judiciary may be the most important instrument for social, economic and political change.” In other words, Powell’s memo advocated using the courts not simply to enforce or interpret the law, but to change it in favor of business. Federal court appointments became increasingly politicized and conservative over the next fifty years, starting with Powell himself. Two months after delivering his memo, Powell was nominated to the Supreme Court.30 On that high perch over sixteen years he created novel litigation tools—such as the weaponization of the First Amendment—with which businesses still pursue deregulatory goals.31 The harder turn towards conservative activism on today’s Supreme Court is fairly seen as the culmination of Powell’s vision and the judicial strategy he advocated.

B. The Neutering of Antitrust

An initial, obvious target for the business lobby was antitrust law and enforcement. After a decade of robust antitrust enforcement, encouraged by a Supreme Court wary of market power, antitrust authorities antagonized the business community further with a lawsuit against IBM in 1969 and the AT&T break-up, beginning in 1974.32 Businesses began a serious campaign to influence antitrust through academic advocates. U.S. companies “coopted and promoted” theorists specially but not exclusively at the University of Chicago, who drew on neoclassical economics to argue for “interpretations” of antitrust law that were more technical and laissez-faire.33 These theorists argued antitrust enforcement in the ‘60s had often worsened rather than alleviated market inefficiencies, and that markets could often self-police against potentially monopolists.34

In line with the Powell memo, companies spent significant sums on academic research and—more insidiously—on influence programs targeted at judges to disseminate Chicago School thinking.35 From 1976 through 1999, numerous federal judges—more than 40% of all judges by 1990—attended all-expenses-paid, ideologically narrow, “economic bootcamps” over several weeks at a beach in Florida, organized by a nominally independent academic center at what is now called the Antonin Scalia Law School, funded by the same companies appearing before the judge-participants in pending cases.36 (These bootcamps also advanced anti-labor economics, another business lobbying goal, discussed more below.) Companies and trade groups began to increasingly write or have ghost-written amicus briefs to advocate their policy goals even in court cases in which they were not directly involved – from 1975 onwards, the number of amici per case that opposed enforcement significantly outnumbered those who supported it, reversing the ratio from the ‘60s.37

In academia, after the heyday of Chicago School theories in the ‘70s and ‘80s, theories of imperfect competition with more complex policy payoffs and less clear legal lessons displaced the cruder models at the heart of the Chicago School.38 But before that happened, the simple and seemingly compelling Chicago School theory had been embedded by market-oriented judges in case law. At work is the peculiarly broad role of “precedent” as practiced in the U.S. legal system, in which later courts usually feel bound not only by the limited holdings but also often the underlying theoretical approaches of prior cases, even when the social science underlying those approaches has shifted. In courts, if not in the ivory tower, anti-antitrust theory has had staying power.

Under Reagan, conservative officials formally narrowed antitrust enforcement to pursue the neoclassical construct of “efficiency” from more open-ended policy goals of prior administrations.39 The increasingly conservative Supreme Court adopted stringent standing requirements on private plaintiffs, weakened “per se” rules against various conduct, and established high thresholds to prove predatory pricing.40 The antitrust agencies revised their “merger guidelines” in 1982, 1987 and 1992, progressively narrowing and setting out clearer rules limiting review of horizontal mergers, broadly eschewing review of vertical mergers, and requiring extensive study before challenging even big deals in concentrated markets.41 Agency budgets plunged; staffing was cut in half.42 As intended, enforcement actions fell. By the late ‘80s, substantive antitrust policy in practice had shrunk dramatically from the ‘60s, continuing as a threat only to the most obvious misconduct.43

C. The Extension of Lobbying into Elections

Further targets were taxes and regulation—but to attack these constraints, more than judicial influence was needed. To pursue legislative and regulatory change, corporations faced a threshold impediment: a Progressive-era ban on corporate political donations to federal election campaigns—the Tillman Act.44 This ban was never viewed as restricting lobbying per se, which is lightly and imperfectly regulated with a rarely enforced disclosure law.45 If they could make a persuasive case for a law, lobbying was all they might need. But money often speaks more loudly than words – and can assure officials will listen. To use money more directly, companies persuaded Congress to authorize corporate “political action committees” (PACs) in a series of laws in the 1970s, after which corporate PACs became an increasingly significant element of the political landscape.46

PACs still cannot simply serve as open conduits from companies to campaigns, but PAC fund-raising costs can be provided by companies to raise funds from shareholders and employees, which can then be given to candidates; with the costs of fund-raising often representing half of the costs of campaign activity, this is a significant way companies can influence political outcomes. One study in a top finance journal finds evidence that PAC activity pays off for corporations,47 with implied effects on policy.

Since the 1970s, corporations have become increasingly adept at routing “dark money” through other channels. These include “super-PACs,” “leadership” PACs, and other “527” groups authorized by a 1975 tax law change,48 which are nominally limited to funding “issue” ads, but often coordinate with non-profit trade groups under 501(c)(6) of the tax code (such as the Chamber of Commerce), as well as non-profits under 501(c)(4) of the tax code (such as Crossroads GPS, the conservative group co-founded by Karl Rove).

In 2010, the U.S. Supreme Court loosened the reins on corporate political activity further in Citizens United, permitting direct expenditures in federal elections, as long as they are “independent” of campaigns. Because these channels of influence are complements,49 Citizens United increased lobbying and corporate PAC activity.50 Because elected officials have only so much bandwidth to consider policy, the increase in business political activity has reduced the ability of individuals and other organizations to pursue their policy goals.

D. Think Tanks as a Counterweight to Academia

More broadly, trade groups became more active in following the Powell memo’s map, taking aim at the all-too-autonomous independent minds of academia. Businesses engaged in “thought leadership” directly, through trade groups, but with increasing emphasis they did so less openly, by expanding their investments in think tank activity. Some of these efforts were serious, some much less so, but all were reinforced by well-funded public relations campaigns, spreading de-regulatory and anti-tax ideology to broad segments of the public.51 Among the pro-business think tanks and influence shops that date to the 1970s are:

- Heritage Foundation (1973),

- Cato Institute (1977), and

- Manhattan Institute (1978).52

Older “conservative” think tanks quickly followed, pursuing radical reforms in the spirit of Powell’s memo.

- American Enterprise Institute’s corporate budget increased from 25% to 40% in the 1970s.53

- Hoover Institution, based in California, was closely tied to President Reagan and his administration.54

- Olin Foundation’s leadership in 1978 was taken over by William E. Simon.

Simon—an LBO professional, and Secretary of the Treasury under Presidents Nixon and Ford—committed the Olin Foundation to building a right-wing “counter-intelligentsia” to challenge egalitarianism.55 While these organizations do not always agree with each other, or with the goals of the major business lobbies, they all pushed “free market,” “cut taxes,” and “deregulatory” agendas, generally helping business lobbying campaigns.

E. Targeting Taxes

On taxes, the Powell memo had noted that the “left” had been mounting a critique of tax incentives and business deductions in 1972, even as business lobbies were pushing for more deductions. Think tanks touted tax cuts as a way to increase tax revenues, decorating policy briefs with references to “supply side economics,” a then-speculative56 and still controversial set of academic claims.57 Corporate lobbies smuggled corporate taxes into overall tax policy debates so as to allow politicians to claim they had cut taxes on middle class Americans while in fact only reducing taxes on business and capital – a rhetorical move recently repeated by President Trump.

Nominal high-bracket corporate income tax rates fell from their Eisenhower-era peak of 52% to 40% in the Reagan-era Tax Reform Act of 1986,58 while effective rates fell even faster, with shareholders of companies paying a mere 7% effective rate in 1979 on profits attributable to their ownership.59 Lower effective rates were due to a multitude of deductions, credits, and exemptions, starting under President John F. Kennedy in the 1960s and accelerating from Nixon to Carter and Reagan.60 Tax rates for the top 1% of individuals, those who own the most corporate equity, also fell from 1980 onwards.61

F. Reversing Regulation

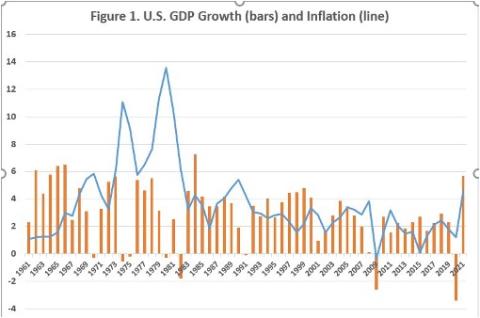

Regulation came under increasing corporate pressure as well. Deregulation, happily for business, was said to be a second implication of “supply side economics,”62 which purported to diagnose and propose a remedy for stagflation in 1974-75 and 1980-82 (inflation peaked at 11% in 1974 and 14% in 1980, see Figure 1).

Whole industries were substantially or wholly deregulated:

- Airlines (1978),

- Oil and gas (1979),

- Trucking (1980), and

- Radio (1984).63

The regulatory process was itself increasingly regulated. In 1978, President Carter ordered agencies to analyze the effects of all new regulations and minimize their burdens.64 In 1980, Congress ordered the creation of the Office of Information and Regulatory Affairs (OIRA) to (among other things) “develop and implement Federal information policies and standards including policies concerning . . . the reduction of the Government paperwork burden on the public.”65 In the same year, the Regulatory Flexibility Act (RFA) passed, requiring agencies to publish analyses of how regulatory changes will affect small entities.66 The RFA benefits small business directly, but in keeping with the way that “small business” reforms commonly benefit large companies, by slowing the regulatory process in general.67 President Reagan in 1981 empowered OIRA to require formal cost-benefit analysis requirements of all executive agencies seeking to adopt new rules,68 effectively slowing down and reducing the agencies’ capacity for regulatory change.69

G. Laying Labor Low

A final priority for the Powell memo and the business lobby in the 1970s was to crush the labor movement. To Americans under the age of 50, this may seem quixotic: why prioritize a pygmy? After all, today’s private sector unions are not a significant economic force, rarely striking (at least until very recently), and representing only 7% of private sector workers in 2022.70 Reflecting a contemporary perspective, Mark Roe premises his account of how politics shapes corporate governance on the insight that when labor power and social democracy are weak, shareholders qua shareholders face less threat from politics, which can induce large blockholders to diffuse ownership to form the U.S.-style Berle-and-Means corporation.71 But his application of that theory to explain U.S. history takes weak labor as a given in the U.S., when it was not always thus.

In fact, in 1970, private sector unions were enormously powerful in the U.S., and had been for decades. At their peak, unions represented over 35% of the U.S. private wage-or-salaried workforce.72 Unions were necessary if not sufficient for the election of Franklin Roosevelt and thus for the entire New Deal. They fought for and obtained passage of the National Labor Relations Act (NLRA) in 1935, aiding them with legal protections and a then-friendly government agency (the National Labor Relations Board (NLRB)) to help protect them and their interests in Washington, D.C. In America’s mid-20th century, as President Nixon grudgingly admitted, “No program work[ed] without Labor cooperation.”73

The struggle between business and labor of course did not end with the NRLB. Corporate lobbying weakened union rights in 1943 and 1947. Congress extended to unions the Progressive-era ban on corporate monetary donations to federal political campaigns, and then banned jurisdictional, wildcat and solidarity strikes, secondary boycotts and mass picketing, and closed shops.74 Businesses continued to resist unionization and collective bargaining, both in their operations and in Washington, D.C.

Nonetheless, World War II and the 1947 law induced in both companies and unions a more cooperative spirit, paving the way for the “corporatism” of the 1950s. In the “Treaty of Detroit,” GM and the UAW in 1950 entered into a five-year collective bargaining agreement that guaranteed pensions, health insurance, a 20% increase in the standard of living for covered workers, and cost of living adjustments (COLAs) in return for labor peace – the absence of strikes and a pacified workforce. That agreement served as a template for other agreements with other companies. Pensions also became an increasingly important component of compensation for government workers, eventually making public pensions a key investor body. At their peak, private sector unions were a strong force in the U.S. economy and in its political system.

But in the mid-1960s, business renewed its anti-union efforts. Three economic forces creating challenges for companies, but even greater headwinds for labor, were globalization, inflation, and a technology-based shift to automation and away from “Fordist” assembly lines.75 Each force contributed to corporate incentives to attack labor. But the effects of each force were mediated by changes in law, reshaped by corporate political efforts.

Globalization was enhanced by corporate lobbying aimed at preserving the U.S. commitment to free trade coming out of World War II. But free trade began to boomerang on American companies by the 1970s. Imports cut profitability and increased their sensitivity to wage demands. Globalization’s effects were heightened by business leaders’ ideological commitments, too. Amid the Cold War and the McCarthy era, they resisted social welfare programs and more generous unemployment insurance, which could have spread and reduced the burden of compensation and adjustment costs for companies and employees seeking to adapt to a globalizing world. But business lobbies feared the legitimacy and power such expansions would give to the federal government.76

Inflation became a useful talking point for business flacks as early as the 1960s. When prices first spiked in 1969 and 1970 at 5% (see Figure 1 above), businesses blamed economy-wide trends on unions, arguing higher prices were caused by union contracts. Omitted from their propaganda was the fact that COLAs had been part of the Treaty of Detroit, willingly agreed by companies in negotiations, and were no more to blame than contracts with suppliers with similar adjustment clauses, or more general price increases by wholesalers and manufacturers companies themselves rippling their way through the economy to the end consumer.77

Automation was accelerated by tax incentives pushed by both large companies and the venture capital lobby. Then as now, the “US tax code aggressively subsidizes the use of equipment (for example, via various tax credits and accelerated amortization) and taxes the employment of labor (for example, via payroll taxes).”78

Tactically, the “No-Name Committee” formed -- a small group of lawyers and industrial relations managers from major public companies. They initially included AT&T, Ford, General Electric, Macy’s, Sears, and U.S. Steel, but came to enlist lawyers at 100 large companies.79 First adopting the name “Labor Law Reform Group,” they joined other anti-labor trade groups to form the Business Roundtable in 1972. The Roundtable augmented existing trade groups such as the Chamber of Commerce,80 as well as its nominally “small business” spin-off, the National Federation of Independent Business (NFIB),81 and the National Association of Manufacturers (NAM).82

All four business groups—which remain important in today’s political landscape—increasingly fought labor. Companies hired professional PR firms to conduct media campaigns and relentless lobbying. They sought to block increases in minimum wage laws, which amid inflation was tantamount to rendering such laws economically trivial. Anti-union consulting firms coordinated thousands of companies83 to fight union campaigns through joint strike insurance funds, particularly in construction.84 Anti-union consultants relied on video surveillance and armed “SWAT” teams, and encouraged termination of workers who tried to create unions, which was and remains illegal, but effective.85 Then as now companies could pay small fines and back wages after a time-consuming dispute resolution process, knowing the tactics would slow or defeat unionization.

Companies focused on subverting the NLRA, fighting every legal battle in a war of attrition. “AFL-CIO litigation costs doubled between 1966 and 1973, and doubled again by 1979.”86 Working with successive White Houses to change the composition of NLRB, companies diluted and eventually turned the NLRA against labor on range of management-union issues. In 1971, for example, the board ruled that there was no duty for corporations to bargain on decisions that involved “fundamental managerial issues,” which effectively overruled an earlier decision and permitted the increasing use of outsourcing and plant closures.87 As the costs of global production fell, such seemingly technical legal changes helped move production to low-wage countries and to low-wage American states, where “open shop” laws and culture inhibited unionization.

Among cultural barriers to Southern unionization were racism and class-based deference, as well as entrenched anti-union business interests that promoted “right to work” laws with McCarthyite and segregationist themes.88 While exceptions existed, “There is no doubt that race mattered in the South and that racism weakened the power of the region’s working class.”89 Bryant Simon also argues that the South had larger pools of deeply impoverished potential strikebreakers, due to its agricultural past. Northern union members did themselves no favors by resisting integration and voting for Republicans who responded to companies’ anti-union lobbying. Democrats divided over tactics and overall policy, and failed to anticipate the power of the Senate filibuster in blocking pro-labor bills under President Carter in the late 1970s.

But without corporate political organization and activity, lobbies ideologically committed to “warfare,” along the lines sketched in the Powell memo, labor power would have endured longer than it did in the U.S. With corporate pressure, by 1978, the NLRA was “all but dead.”90 By 1985 the NLRB and the increasingly conservative courts—often trained at the corporate-funded “bootcamps” noted above—had turned it into an anti-union employer protection law.91

Today union “density” (union membership as a share of employment) is as low as it was in 1916.92 The exception—and an increasingly important one as private sector unions declined—was public sector unions, which became an increasingly large fraction of total union membership starting in the 1960s. But private sector union decline was at least partial cause of the decline in worker income and wealth from the 1970s to today.93 So, too, was the decline in corporate profits in the 1970s, and the means by which public companies recovered from that decade, as discussed more below.

III. Globalization and the Rise of Investor Power Through Hostile Bids and Corporate Governance

As U.S. public companies were building and flexing their political muscles to reverse many of the policies of the New Deal, they experienced increasingly heavy economic pressure in the global marketplace. Each of the forces that undermined labor – globalization, inflation, and automation – created challenges for public companies. Market-driven responses to these challenges – hostile takeovers, private equity buyouts, and a new “shareholder rights movement” – eventually returned U.S. public companies to profitability, at the expense of the autonomy of U.S. corporate managers and with further loss of political legitimacy and public confidence.

A. Worth More Dead than Alive

Lower trade barriers adopted after World War II spread of globalization in the parts of Europe and Asia that did not embrace communism. True, globalization only ever threatened a portion of U.S. business – less than a quarter of all low-skill U.S. workers were ever employed in manufacturing – most were and are in retail and service, and primarily local.94 But in the most unionized sectors, with the highest working class wages, at some of the largest U.S. companies, German and Japanese industrial resurgence and lower shipping and communication costs drove down market-clearing prices and gutted U.S. heavy industry’s ability to maintain market share. Pre-tax profitability (cash flow to assets) fell from 16% in 1966 to an average of 9% in the early 1970s.95

Despite having new flexibility from their successful political and legal campaign against unions, U.S. companies were initially slow to make major changes in how and where they produced goods. Outsourcing and relocation to lower labor cost locations ate away at union membership, but too slowly to prevent erosion of corporate value from global competition. The stagflation of the 1970s and early 1980s cut stock prices below the values of the assets those companies owned. An increasing number of public companies were worth more dead—broken up and liquidated—than alive.

B. Hostile Bids and Leveraged Buyouts as the Cure

In this economic low surged hostile takeovers. Takeovers are attempts by one or a small group of new investors to acquire enough stock of a public company to control it, over the objection of its current board and management. Bidders offer prices significantly above current market prices (“premiums”), attracting support from the target’s shareholders. Usually motivated by the bidder’s belief that it can make more money than the bid would cost by selling off assets (“bust-up” takeovers), increasing its debt and/or paying out cash (“recapitalizations”), or otherwise changing its strategy and operations (“restructurings”), hostile bids of the ‘80s typically accelerated and increased layoffs or plant closures.

While hostile takeovers have appeared throughout U.S. history, they remained marginal until the ‘80s, and then fell again in importance after the ‘80s. In that decade, a third of all major U.S. public companies became the direct subject of takeover attempts, and no U.S. public company was unaffected by them. Financing innovations (including greater market receptivity to junk bonds and higher levels of debt generally) were coupled with a more sophisticated “deal industry” – bankers and lawyers specializing in mergers and acquisitions, who helped refine techniques and defend the phenomenon against political intervention.

Private equity buyouts were stimulated by hostile bids, and vice versa. Unable to count on a quiet life, managers more frequently saw the writing on the wall, and sought themselves to buy out public investors and “go private,” a phenomenon that began in the ‘70s but accelerated in the ‘80s. Public companies engaged in their own “voluntary” bust-ups (divestitures and spin-offs), restructurings, layoffs, plant closures and recapitalizations. Initially a wave of such transactions occurred as defenses to specific hostile bids, but then they began to pursue a life of their own. Increasingly over the ‘80s, and into the ‘90s and beyond, U.S. public companies acted as if they were under the threat of hostile takeovers (or, later, an attack from a hedge fund activist), long after the takeover wave of the ‘80s had subsided.

C. The Loss of Large Company Legitimacy

One no doubt unintended effect of corporate political mobilization in the ‘70s was to contribute to the decline in public opinion of big business. One study finds that (based on Roper polls), public attitudes towards corporations were at their peak in the post-War period of American hegemony, circa 1953.96 As noted earlier, that positive attitude was at least significantly attributable to New Deal laws and institutions the Powell memo attacked companies for defending, as well as the “corporate social responsibility” ideology of the time, corporate philanthropy and union-demanded health and pension benefits that companies unwound in the ‘80s (discussed more below).

Even in the early ‘50s, only 56% of Americans had positive views of business.97 But from 1970 to 1980, public happiness with business fell sharply, even as companies began to achieve success in the political and regulatory spheres. Positive attitudes towards companies bottomed out between 30 and 35% positive, where it remained through the early ‘90s. Public attitudes towards big business are worse today. In 1980, Gallup reported 20% of Americans had a “a great deal” or “quite a lot” of confidence in “big business,” down from 35% in 1975.98

By June 2022, public confidence in big business stood at an all-time low: 14%. In a telling contrast, when asked about “small business,” the total was 68%. Big business today has political power because of its wealth, organization and informational advantages, and ideological commitments to other political actors to “markets” and “capitalism,” not because of a reservoir of trust among voters. And as noted next, the interests of “free markets” and “business” do not always align.

D. Markets vs. Corporations: Intra-Capitalist Conflicts

Another unintended (and somewhat ironic) effect of corporate political organization in the ‘70s was to pave the way for the hostile bids of the ‘80s. The reduction of labor as a force made it easier for bidders to take over companies and profit from layoffs, outsourcing and offshoring. The programmatic attack on antitrust law and enforcement increased deal activity generally, attracting dollars and talent to Wall Street and greasing the wheels of the “market for corporate control.”99

By latching onto and helping to promote free market ideology to advance its deregulatory goals, corporate trade groups such as the Business Roundtable and the Chamber of Commerce promoted the careers of political agents and boosted the budgets of think tanks and academic financial economists (particularly in business schools) committed to market solutions to every social ill. Hostile bids were viewed by many as a perfect example of a market solution. The Reagan Administration, in particular, while friendly to public companies and their political goals on many dimensions, resisted managerial efforts to regulate takeovers.

The ideology of free markets also coalesced around a more focused ideology of shareholder wealth. The measure of corporate success would not be organizational survival, market share, or contributions to society more generally, but solely whether they created profits that were distributed to shareholders. For public companies, that would translate into a dominant metric of success: the share price. In part driven by this ideological shift, shareholders themselves mobilized to support hostile bids, oppose managerial resistance to bids, and organize politically, much in the way that corporations had done in the 1970s. A shift from pensions to 401(k) plans noted below may also have reinforced the ideology of shareholder primacy.100

Shareholders aided hostile bidders in litigation, and more generally by resisting takeover “defenses” on a company-by-company basis, and in Washington, D.C. Many ways managers could make takeovers more difficult required shareholder approval under corporate law: “classifying” boards into subgroups elected every three years, for example; or adopting charter terms effectively preventing “bust-up” transactions after a hostile bid. What had been a pro forma process in which passive shareholders would rubber stamp management proposals in the past became increasingly difficult, and ultimately nearly impossible.

E. Institutional Investors as a New “Social Movement”

Most important, for the long run, including today’s political struggles over index and private equity funds, was how the political struggle over hostile takeovers helped create a permanent “social movement” among institutional investors. The movement resulted from several causes. First, ownership had to concentrate enough as a precondition for shareholders to organize. Second, regulation of institutional owners had to prompt some consideration of the possibility of organization. Third, there had to be some politically salient “trigger” for the organization effort to start.

i. Growth in Institutional Ownership as a Precondition

The preconditions for the organization of a shareholder lobby date to the ‘50s and ‘60s. In that period, as noted above, unions advocated for broader benefits, including pensions, and corporate managers saw pensions as less threatening to their overall interests than government-provided social insurance. Pension funds became increasingly important owners of public company stock, reflecting economies of scale in investment, and also helped fund the growth of the private equity industry in the 1980s.101

Table 1 shows the rise of institutional ownership in the United States since 1950, using standard data from the Federal

Reserve Board:

Table 1. Institutional Ownership of US Corporate Equity

| Year | Corp. Equity ($B) | Institutions | Pensions | Investment Companies | |||

| 1950 | 170 | 16 | 9% | 1 | 1% | 5 | 3% |

| 1960 | 420 | 60 | 14% | 2 | 0% | 20 | 5% |

| 1970 | 831 | 181 | 22% | 78 | 9% | 44 | 5% |

| 1980 | 1535 | 436 | 28% | 306 | 20% | 42 | 3% |

| 1990 | 3530 | 1433 | 41% | 947 | 27% | 233 | 7% |

| 2000 | 17627 | 8631 | 49% | 3987 | 23% | 3227 | 18% |

| 2010 | 23411 | 14674 | 63% | 4004 | 17% | 5713 | 24% |

| 2020 | 65444 | 39273 | 60% | 6636 | 10% | 17725 | 27% |

Source: Federal Reserve Board Flow of Funds Accounts

The shift was large and sustained. In 1950, “households” (i.e., individuals) directly owned 81% of corporate equity in the U.S. By 2010, their share had fallen to 37%. (What might seem to be a slight rise in household ownership from 2010 to 2020 in fact obscures a shift in ownership from what the Fed counts as “institutions” and, more importantly, what it leaves out: private equity funds (as well as hedge funds); when those institutions are considered, household ownership in fact continued to decline from 2010 to 2020.)

From 1980 to the present, pension funds have been overshadowed by mutual funds, including index funds. This shift reflected a deliberate choice by both Congress (through tax incentives) and companies to shift from “defined benefit” (DB) plans (e.g., pensions) to “defined contribution” (DC) (e.g., 401(k)s) plans in the 1980s. DC plans were and are still invested largely through mutual funds.

DC plans had the ideological virtue of giving some measure of control and responsibility to individual employees,102 versus the corporatist-style structure of trustee-overseen pensions. But for businesses, DC plans were more attractive than DB plans because they were fully “off balance sheet”—they were in effect pass-throughs of ownership interests of employees and retirees, rather than (as with pensions) a formal obligation of the companies, with the possibility that the obligations might turn out to be more expensive than anticipated, particularly in industries that were in long-term decline, due to among other things globalization or automation.

As markets gyrated wildly in the late 1970s and 1980s, the match between DB plan assets and liabilities was volatile. Some pensions were underfunded, requiring greater contributions, cutting profits. Other pensions became overfunded, attracting hostile takeovers seeking to “raid” the pension. Irwin L. Jacobs, for example, extracted $100 million from AMF Inc.’s pension just weeks after taking over AMF through a hostile bid.103

Whatever the mix between pensions and mutual funds, institutional ownership has continuously risen from the 1960s to the present—reflecting the fact that, left unaddressed, economies of scale in finance increase concentrations of wealth. Institutions had by 1980 achieved enough ownership to support the shareholder rights movement, in which they were (and remain) key players. In many ways, the problem of twelve created by index funds is just an intensification of the shareholder rights movement of the 1980s.

ii. Regulation of Institutions as a Prompt

A second cause of the political organization of shareholders was a tightening of the regulation of institutions themselves. Fiduciary duties imposed on pension funds in the Employment Retirement Income Security Act (ERISA) of 1974. Although those duties (as interpreted by the Department of Labor (DOL)) encourage pensions to not hold large blocks of any given company’s stock, to reduce risk,104 those same duties were tightened in the late 1980s to encourage more active use of the voting and other rights that pension investments in corporate stock generated.105 This push by the DOL was designed in part to try to address conflicts of interest between pension fund trustees and companies that sponsored the funds, whose managers often tried and sometimes succeeded in pressuring trustees to remain neutral in takeover battles, or simply to remain passive, and not use the voting power associated with shares they owned.

iii. Greenmail and Other Hostile Takeover Defenses as the Trigger

The growing potentially “socialist” power of pensions had been noted by Peter Drucker as early as 1976,106 but it took until the 1980s for the right trigger event for their political organization. Hostile takeovers were the trigger, especially specific managerial responses, such as “greenmail,” the first of many items on an increasingly long shareholder policy agenda. Greenmail was, effectively, a bribe paid by target managers to make a hostile bidder walk away and leave the public company as it was, with current managers in place.107 It combined apparent corruption with unequal treatment and the loss of an expected gain for target shareholders. Texaco, infamously, paid $1.3 billion to the Bass brothers of Texas simply to go away, to avoid a takeover that would have produced a 36% premium over the stock market price.

The resulting outrage was the trigger for Jesse Unruh, treasurer of California and a trustee of CalPERS (the largest public pension fund) and the California State Teachers’ Retirement Fund, to found the Council of Institutional Investors (CII) in January 1985. He recognized that takeover defenses—greenmail, but also poison pills, golden parachutes, and leveraged stock buybacks—were collectively “an issue that, in political terms, could be sold in Pasadena.”108

In a few years that followed, several other trade groups sprang up to further organize shareholders, aided by data and analysis on corporate governance from two older but still-active organizations, the Investor Responsibility Research Center (IRRC)109 and the Interfaith Center on Corporate Responsibility (ICCR). T. Boone Pickens, perhaps the most well-known “raider,” founded the United Shareholders Association, in 1986 nominally to help coordinate individual shareholders. Since the ‘60s, shareholder “gadflies” had been active, seeking to put social and political questions on corporate meeting agendas by bringing shareholder resolution proposals, and the new institutional shareholder groups began to ally with and coopt the tools of such gadflies.

Most importantly for the long-run politics of shareholder power, Robert Monks in 1985 formed Institutional Shareholders Services (ISS) to provide advice on voting and other topics to institutional investors.110 While not binding on any given institution, the ability of ISS and other proxy advisors to coordinate the votes of disparate institutions has significantly increased the ability of a consensus position on a given governance issue to result in “voluntary” change by corporate boards. Regulation of proxy advisors remains a major policy goal of the U.S. Chamber of Commerce, seemingly impervious to the hypocrisy involved, given its overall take on the vices of regulation.

Labor unions—which (as discussed above) had their clout reduced as representatives of current employees, and burned by managers in their brief alliances in fighting hostile bids in the ‘80s—also have played an important role in the shareholder rights movement, as stewards of union pension funds. All these organizations have aimed at supporting shareholder rights and interests generally, and sought a greater role for shareholders in the governance of public companies. They have effectively replaced unions (of current employees) as one of if not the most organized forms of social resistance to corporate power, at least wherever interests of dispersed shareholders are (directly or indirectly) affected by policy issues currently in play.

iv. Free Market Ideology Returns to Undermine Corporate Political Power

A final contributing cause of the shareholder rights movement was ideological—and reflected an increasingly important divide within people and organizations promoting “business” or “capitalist” goals in general. Traditional business lobbies were alarmed by, or at least neutral on hostile takeovers, because they directly threatened the jobs of individuals who were key funders of those organizations. Indeed, corporate managers briefly formed alliances with organized labor to try to pass anti-takeover laws, an alliance that died when it became apparent that managers had begun to defensively and preemptively adopt the same offshoring, outsourcing, wage-cutting and job-reducing strategies as hostile bidders.

But hostile bidders and institutional shareholders formed an equally unlikely partnership by together embracing free-market regulatory stances of the Reagan administration as applied to capital markets, which was influenced by “Chicago School” economics. Lewis Powell’s memo had celebrated Milton Friedman, who in turn celebrated free markets, including anything that maximized share prices, such as hostile bids. The Lewis Powell of 1972 would have surprised that the Lewis Powell of 1987 would have to struggle to write a complex, internally inconsistent opinion in CTS v. Dynamics Corp.111 that just barely convinced a majority of a fractured Supreme Court to uphold a weak antitakeover statute—a legal intervention in the “free market” that elevated politicians over capitalism in its purest form. Corporate interests and free market interests diverged in a remarkably short period.

Republicans divided on hostile takeovers, with many providing political support for takeovers themselves, and the shareholder-focused ideology of institutional shareholders. Reagan appointed free market enthusiasts not only to the SEC, but also to the Council of Economic Advisors, whose 1985 Economic Report of the President gushed over how takeovers could promote efficiency; to the Federal Trade Commission and Department of Justice, which reduced antitrust enforcement; to the federal courts, where they battled with more manager-friendly followers of Lewis Powell over state takeover statutes; and to the DOL, which pushed corporate pension plans to become more active in governance. Capitalist politics had turned on business.

IV. The Contemporary Setting for Investment Funds in the Political Arena

What do we learn from these reviews of corporate political and economic history from 1970 to the late ‘80s? Berle-and-Means public companies remain—and have been increasingly politically organized and active. They are no longer threatened by socialism, internationally, or labor, domestically, nor are they strongly constrained by antitrust law. They face reduced taxes (even lower after cuts under Donald Trump) and regulation, particularly industry-based price or output regulation. “Free market” ideas are far more prevalent in policy debates than they were in 1965. Nixonian wage-and-price controls were not even on the table in the post-Covid inflationary spike. The biggest constraint on business is no longer “government” (or labor), but market-aligned shareholder “governance.”

In fairness, much government regulation remains taken-for-granted and in force (if weakened). Workers’ compensation, minimum wage laws and unemployment insurance remain, if effectively reduced by inflation. Workplace and safety rules persist, even if erratically enforced. Environmental regulations from the ‘70s remain on the books, if “renegotiated” with companies, and only weakly responsive to new environmental threats (such as climate change). Corporations pay (lower) taxes, and plan around tax law. Federal securities laws—and the transparency, legitimacy and accountability they create for big business—remain largely intact as applied to listed companies, even as they have modestly rationalized and updated over the years. The federal bureaucracy continues as ballast, if nothing else, slowing regulatory change, an inertial force reinforcing Congressional dysfunction in preserving existing policy settlements as they are.

It is also true that some ‘60s-era organized political adversaries—consumer groups, human rights organizations, and left-leaning think tanks—continue to press for laws contrary to business interests. The same is true at times of both political parties, Democrats more so, but Republicans too, on issues such as diversity and immigration (where large companies are generally more open to cosmopolitanism and free movement of labor than the Republican party). The continued production of truth by members of the academy continues to threaten powers of all kind. But Democrats since Clinton have been far more openly and consistently pro-business than they were in the middle of the twentieth century, and Republicans continue to be strongly anti-tax and on most business issues anti-regulation.

In sum, the overall state of public policy for large public companies has markedly improved since 1970, and in today’s political battles, they start farther down the field than in the past. Large public companies are used to winning in the domestic political sphere. At the same time, they lack public trust and legitimacy. This forces them to find allies (such as small business, or financial firms) or work through channels (such as litigation, highly technical laws, and regulatory appointments) that much of the voting public does not track.

And public companies have been increasingly “regulated” by a new organized opposition group: shareholders generally, institutional shareholders in particular, and increasingly index funds above all others. No longer can the presumptive passivity of dispersed shareholders be taken for granted. Institutional shareholders are a political force, acting both in specific moments in struggles for control over individual companies, but also more generally, in Washington, D.C. and state political capitols. At the corporate level, the number of anti-management shareholder resolutions increased from less than 40 in 1987 to 153 in 1991, or roughly one proposal at every 42 U.S. public companies.112 In 2022, there were 797 such proposals, or roughly one proposal for every 8 companies, and among the S&P 500 (the largest public companies), each year each company receives at least one proposal, on average.113

In 1990 alone, “more shareholder proposals passed . . . than in the entire history of shareholder proposals prior to 1990.”114 Most recently, the rate at which proposals are approved by shareholders has jumped markedly, from 1% over the period from 2010 to 2019 to 12.4% in 2020 and 19.2% in 2021, before ticking down again in 2022 due to weakened constraints on which proposals have made it through the SEC staff review process.115 Since most companies who anticipate losing give in and “settle,” the impact of shareholder resolutions has been ever larger than these numbers suggest. Shareholder support for anti-poison-pill proposals increased in the average firm from 29% in 1987 to 45% in 1991; by the 2000s, shareholders had pressured most companies to drop their pills.116 Similar trends have been seen for staggered boards, which are actually more important than the more well-known poison pills.117

Reflecting the strikingly rapid success of the shareholder rights movement, the SEC Chair used a 1990 CII meeting to announce the commission’s initiation of a major review of the proxy rules, which had been critiqued by shareholder advocates as unnecessarily hampering their ability to communicate. Two years later the rules were rewritten in favor of shareholders. Davis and Thompson have argued that the fact the “shareholder rights movement” movement of the 1980s succeeded so rapidly—from creation in 1985 to significant political influence by 1990—suggests how important growth in institutional ownership was from 1960 to 1990.118 Increased ownership lowered the costs of organization and made the more conventional method for a shareholder who disliked corporate managers (“exit,” i.e., sale of stock, also known as the “Wall Street walk”) more expensive – because sales of larger blocks of stock can depress the prices at which sales take place.

Still, the rapid success of the shareholder rights movement is partly attributable to ideology and taken-for-granted but sometimes mistaken beliefs and assumptions about whether activism could be worth pursuing by investors, and over what issues.119 Not all of the mistaken beliefs were corrected over time; some were amplified by political entrepreneurs and sloppy academic research. Sentiment among institutional shareholders against “poison pills,” for example, reflected theoretically unsound research and a basic misunderstanding of how pills work.120 It would take at least another decade before dialogue among institutions, researchers and the public leveled up the discussion to approach theoretical models of “rational choice.”

In sum, a major consequence of corporate political activity in the ‘70s, and the emergence of shareholders as a political force in the ‘80s, is that index funds and private equity funds have emerged as powerful political organizations in a political landscape significantly altered—even simplified—compared to that of the mid-20th century. Without labor as a force, with business lacking public trust, and with government itself weak, the relative sway of index and private equity funds over American society is significant. More than any other types of organizations, they have power to rival big business, in a moment that is starkly different if no less dangerous for democracy, capitalism and companies alike than the ‘20s and ‘30s.

Corporatist alliances with labor of the mid-20th century are gone. Many features of the New Deal that helped legitimate capitalism and business generally have been eliminated or reduced— notably among the survivors, the transparency imposed on public companies by securities laws remains largely intact, but only for companies not owned by private equity firms. U.S. businesses as a whole survived globalization and automation, but only by becoming global themselves, adopting “asset lite” strategies, relying on contractors who lack job security and employer-based benefit, shifting to new technologies with more ambiguous social benefits, and offshoring increasing amounts of work to geographically remote polities. In so doing, they have lost much of their legitimacy in the eyes of the American public, even as they remain vulnerable to hostile takeovers and shareholder activism.

As a result, the perception at least is that corporate leaders are increasingly detached from ground level U.S. politics. Public opinion of large companies is at an all-time low. Populism helped elect Donald Trump. In this moment, public companies are under threat from index and private equity funds, for different reasons. Index funds threaten directly to build their influence over public companies, in part because broader segments of the public are channeling their money and efforts into governance via such funds. Meanwhile, private equity funds threaten to supplant public companies altogether, taking them “private” and outside of both index fund ownership and SEC disclosure rules.

In turn, both types of funds are under political pressure themselves.121 Index funds are being attacked by Republicans as socialist tools; private equity funds are being attacked by Democrats as tools of plutocracy. The growth of institutional shareholder power, and the demise of political constraints on large companies, means that political actors are increasingly focusing on investment funds as a tool for pursuing their agendas. Corporate political freedom has been more than overmatched by economic constraints, and economies of scale in finance have generated a new form of political oversight by concentrated investment agents. Perhaps the divided politics of our time will create gridlock not only in Washington, D.C., but in Philadelphia (Vanguard’s home), Boston (Bain, Fidelity and State Street) and New York (Apollo, Blackrock, Blackstone, and KKR). Even political stasis, however, is the result of politics, and a third-rail of American politics is concentrated power. The “problem of twelve”—the problem of concentration of political influence through control of large businesses—is a major new challenge to the political economy of business in the twenty-first century.122

- 1John C. Coates, The Problem of Twelve: When a Few Financial Institutions Control Everything (2023). For earlier “problems of twelve” see Bray Hammond, Banks and Politics in America, from the Revolution to the Civil War (1957) (political battles over banking in the early 19th century); Mark J. Roe, Strong Managers, Weak Owners: The Political Roots of American Corporate Finance (1994) (battles over insurance, banking and mutual funds); Morton Keller, The Life Insurance Enterprise, 1885-1910 – A Study in the Limits of Corporate Power (1963) (battles over insurance companies).

- 2Adolf A. Berle & Gardiner C. Means, The Modern Corporation and Private Property (1932).

- 3S. Rep. No. 1455 (1934).

- 4During this period, a majority of those polled supported public ownership of utilities, and nearly as many supported public ownership of banks as opposed it. See Seymour Martin Lipset & William Schneider, The Confidence Gap: Business, Labor, and Government in the Public Mind 61, 283 (1983); see also Robert S. McElvaine, The Great Depression: America 1929-1941 205 (1984) (“The Depression led many intellectuals into believing that some sort of social and ideological apocalypse was at hand . . . [and] scores of leading thinkers turned to Marx.”). Former Delaware Chief Justice Leo Strine has discussed the larger political context of the classic work by Berle and Means. Leo E. Strine Jr., Made for This Moment: The Enduring Relevance of Adolf Berle’s Belief in a Global New Deal, 42 Seattle U. L. Rev. 267 (2019); see also McElvaine, supra this note, at 207 (“Nearly 60 percent of the poor questioned in a 1935 Fortune survey said that the government should not ‘allow a man who has investments worth over a million dollars to keep them.”‘). I have noted this background in John C. Coates, Private vs. Public Choice of Securities Regulation: A Political Cost/Benefit Analysis, 41 Va. J. Int’l L. 531 (2001).

- 5Fair Labor Standards Act, Pub. L. 75–718 (1938), upheld in Jacobs v. Peavy-Wilson Lumber Co., 33 F. Supp. 206 (W.D. La. 1940).

- 674-198, 49 Stat. 449 (July 6, 1935). On labor, see Jake Rosenfeld, What Unions No Longer Do (2014); Nelson Lichtenstein, State of the Union: A Century of American Labor (2d ed. 2002).

- 7E.g., Banking Act of 1933, Pub. L. 73–66, 48 Stat. 162 (1933) (separating commercial from investment banking, creating the Federal Deposit Insurance Corporation and the Fed’s Federal Open Market Committee); Motor Carrier Act of 1935, Ch. 498, 49 Stat. 543 (bringing “motor transport,” i.e., trucking under the jurisdiction of the Interstate Commerce Commission, which had overseen railroads since its inception in 1887); Civil Aeronautics Act of 1938, Ch. 601, 52 Stat. 977 (repealed 1958) (bringing airlines under price and entry regulation under the Civil Aeronautics Board).

- 8After the “appointment of Thurman W. Arnold to the Department of Justice Antitrust Division in 1938[,] Arnold’s first step was to increase his division’s budget and legal staff, which both grew by more than 500 percent in just two years.” Laura Phillips Sawyer, US Antitrust Law and Policy in Historical Perspective, in Oxford Research Encyclopedia of American History, 10 (Jon Butler ed., Oxford Univ. Press 2019). After a series of adverse court decisions, Congress augmented the Clayton Act of 1914 in the Celler-Kefauver Act in 1950, ch. 1184, Pub.L. No. 81-899, 64 Stat. 1125 (1950), codified as amended at 15 U.S.C. §§ 18, 21, to cover asset as well as stock acquisitions and vertical and conglomerate as well as horizontal mergers. C. Paul Rogers III, A Concise History of Corporate Mergers and Antitrust Law in the United States, 24(2) Nat’l L. School of India Rev. 10 (2013).

- 9The AAA created a price and quantity control system for agriculture, Ch. 25, 48 Stat. 31 (1933), codified as amended at 7 U.S.C. §§ 601–624. Parts of the initial AAA were declared unconstitutional in United States v. Butler, 297 U.S. 1, 68–78 (1936), and it was revised to include subsidies funded by federal taxes in Ch. 30, 52 Stat. 31, codified as amended in 7 U.S.C. §§ 1281–1407, which was upheld by the Supreme Court against a challenge under the Due Process Clause in Mulford v. Smith, 307 U.S. 38 (1939) and on Commerce Clause grounds in Wickard v. Filburn, 317 U.S. 111 (1942). The CCC was a work program that ran from 1938 to 1942 to provide employment in government work projects, which included infrastructure (e.g., bridges, fire outlook towers), public amenities (wildlife trails, camps), and land surveys.

- 10Caley Horan, Insurance Era: Risk, Governance, and the Privatization of Security in Postwar America (2021).

- 11W. Elliot Brownlee, Federal Taxation in America: A Short History (2004). Marginal rates on the highest income bracket peaked at 92% in 1952 and 1953. See Tax Rate Schedules, Instructions for Form 1040, years 1944 through 1963, U.S. Dep’t of the Treasury, available at https://www.irs.gov/pub/irs-prior/i1040--1944.pdf and seq. (changing 1944 in URL to year sought). A corporate income tax was enacted in 1894 but was held unconstitutional a year later in Pollock v. Farmers’ Loan & Trust Co., 157 U.S. 429 (1895). After ratification of the Sixteenth amendment to the U.S. Constitution, which established the legality of progressive income tax generally, Congress transformed an excise tax imposed in return for the privilege of limited liability and indefinite duration associated with the corporate form, adopted in 1909, into the modern corporate income tax. For a summary of policy on corporate tax that presents “double taxation” as policy problem to be solved, see Mark P. Keightley and Molly F. Sherlock, The Corporate Income Tax System: Overview and Options for Reform, Congressional Research Service (2014).

- 12The phrase “arsenal of democracy” is commonly credited to Roosevelt, who is said to have derived it from William Knudsen. Arthur Herman, The Arsenal of Democracy: How Detroit turned industrial might into military power during World War II, The Detroit News (Jan. 3, 2013).

- 13A.J. Baime, The Arsenal of Democracy: FDR, Detroit, and an Epic Quest to Arm an America at War (2014).

- 14David Vergun, During WWII, Industries Transitioned from Peacetime to Wartime Production, Dep’t of Defense (Mar. 27, 2020), https://perma.cc/QU7A-3Y5G.

- 15Id.; A.J. Baime, How Detroit Factories Retooled During World War II to Defeat Hitler, History.com (Mar. 19, 2020), https://perma.cc/5JMY-48YH.

- 16Harry C. Thomson and Lida Mayo, The Ordnance Department: Procurement and Supply 32 (United States Army Center of Military History 1991).

- 17Paul A. C. Koistinen, Arsenal of World War II: The Political Economy of American Warfare, 1940–1945 (Lawrence: University Press of Kansas 2004). Dwight Eisenhower popularized the phrase in his farewell address. President Dwight Eisenhower, Farewell Address, (Jan. 17, 1961).

- 18Walter Scheidel, The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century (2017).

- 19Charles Higham, Trading with the Enemy 36–7 (1983).

- 20Adam LeBor, Overt and Covert, N.Y. Times (Nov. 8, 2013) (reviewing Steven Kinzer, The Brothers: John Foster Dulles, Allen Dulles, and Their Secret World War (2013)).

- 21Jane Mayer, Dark Money: The Hidden History of the Billionaires Behind the Rise of the Radical Right x-xi (2016).

- 22Higham, supra note 19, at 45–46.

- 23Id. at 99–100.

- 24Mark C. Suchman, On Advice of Counsel: Law Firms and Venture Capital Funds as Information Intermediaries in the Structuration of Silicon Valley 6 (1994) (unpublished Ph.D. dissertation, Stanford University) (“Prune Capital”); Everett M. Rogers & Judith K. Larsen, Silicon Valley Fever: Growth of High-Technology Culture 39, 269 (1984) (noting roles of the Department of Defense and NASA in birth of Silicon Valley); Annalee Saxenian , Regional Advantage 20–27, 178 n.38 (1994) (Lockheed employed 12,000 in Santa Clara County in 1964). I have noted this set of facts in John C. Coates, Explaining Variation in Takeover Defenses: Blame the Lawyers, 89 Cal. L. Rev. 1301 (2001).

- 25Rigorous time-series surveys of public trust in business only starts in the 1970s, but shows a consistent overall decline since the earliest such survey. Economists have established that trust in business (as well as government) tracks the business cycle. Betsey Stevenson and Justin Wolfers, Trust in Public Institutions over the Business Cycle, 101(3) Am. Econ. Rev. 281–87 (2011). That suggests trust in business was low in the Great Depression, consistent with the popularity of socialism at the time. It follows that trust in business was increasing over the middle part of the twentieth century to peak in the early 1970s.

- 26Peter Drucker, The New Society (1950). See also Adolf Berle, Power without Property (1959); Research and Policy Committee of the Committee on Economic Development, A Statement of National Policy: Social Responsibilities of Business Corporations (1971), reprinted in part in L. Solomon et al., Corporations: Law and Policy (1982), at 750–53.

- 27Cf. Thomas Sowell, Knowledge and Decisions 382 (1980) (“The first peacetime imposition of federal wage and price controls in American history occurred in 1971 under an administration widely regarded as ‘conservative’ – as indeed it was.”).

- 28Memorandum from Lewis F. Powell, Jr. to Eugene B. Sydnor, Jr., Ed. Comm. Chair, U.S. Chamber of Commerce (Aug. 23, 1971) [hereinafter Powell Memorandum]. This section draws on John C. Coates, Corporate Speech and the First Amendment: History, Data and Implications, 30 Constitutional Commentary 223 (2015).